什么是第179条(Section 179)抵扣?

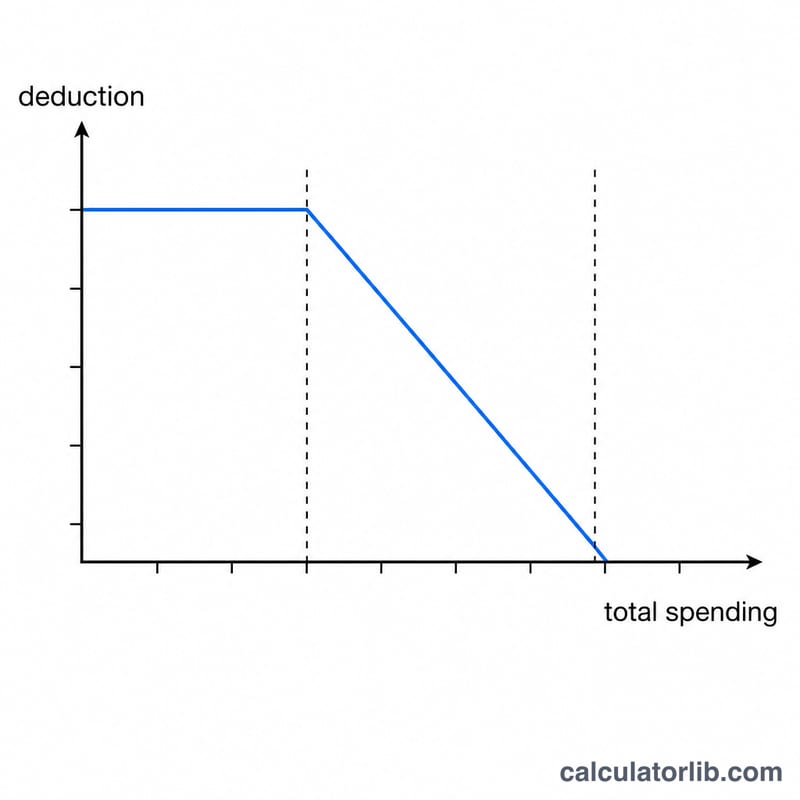

本计算器适用于美国,采用美国国税局(IRS)针对2023纳税年度的第179条限额:最高抵扣额为116万美元($1,160,000),支出逐额递减的起征点为289万美元($2,890,000)。第179条允许企业在符合条件的设备和软件投入使用的当年,一次性全额扣除其购置成本,而无需在多年内分期折旧。请注意:这是美国的税收制度,中国及其他国家的固定资产折旧与税前扣除规则与此不同。具体年度数字及适用资格,请务必咨询专业税务顾问或查阅IRS第946号刊物(Publication 946)。

如何使用

输入您想抵扣的某项资产的购置成本、本年度设备采购总额,以及可选的奖金折旧率(2024年投入使用的资产为60%,更早年份往往为100%——请按对应年度核对)。计算器会先算出经逐额递减后可享受的第179条抵扣额,再对剩余计税基础适用奖金折旧。

计算公式说明

当您的设备采购总额超过289万美元时,每超出1美元,年度116万美元的上限就相应减少1美元。举例来说,若您购入价值295万美元的设备,上限将减少6万美元,降至110万美元。第179条抵扣额取「资产成本」与「调整后上限」二者中的较小值。扣除后剩余的计税基础,可继续适用奖金折旧。

$$\begin{gathered} D = S_{179} + \left(\text{Cost} - S_{179}\right)\times \dfrac{\text{Bonus Rate}}{100} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} S_{179} &= \min\!\left(\text{Cost},\ L\right) \\ L &= \max\!\left(0,\ 1{,}160{,}000 - \max\!\left(0,\ \text{Total Purchases} - 2{,}890{,}000\right)\right) \end{aligned} \right. \end{gathered}$$

实例演算

假设您购入一台价值10万美元的机器,且本年度采购总额为10万美元(低于起征点,故无需逐额递减)。在奖金折旧率为60%的情况下:第179条抵扣额 = min($100,000,$1,160,000)= $100,000。由于成本已被全额扣除,剩余计税基础为$0,奖金折旧也为$0。第一年抵扣总额 = $100,000。

$$S_{179} = \min\left(100{,}000,\ 1{,}160{,}000\right) = 100{,}000$$

$$D = 100{,}000 + \left(100{,}000 - 100{,}000\right)\times \dfrac{60}{100} = 100{,}000$$

常见问题

抵扣额会超过我的购置成本吗?不会——抵扣额以您输入的资产成本为上限。

如果我的采购总额超过405万美元($4,050,000)会怎样?第179条限额会完全递减归零,抵扣额降至$0(但奖金折旧可能仍然适用)。

有收入限制吗?有。第179条抵扣额不得超过您企业的应税所得;本计算器未纳入该项限制。