What is the Home Office Deduction?

Applies to the United States (IRS rules). If you use part of your home regularly and exclusively for business, you may deduct related costs. The IRS offers two ways to figure this: the simplified method and the actual expense (regular) method. This calculator computes both and tells you which yields the larger deduction. It is an estimate for tax-year planning, not tax advice — limits and eligibility rules can change.

How to use this calculator

Enter the square footage of your home office, the total square footage of your home, and your total annual home expenses (rent or mortgage interest, utilities, insurance, repairs, depreciation, etc.). The tool returns the simplified deduction, the actual-expense deduction, your business-use percentage, and the larger of the two.

The formulas explained

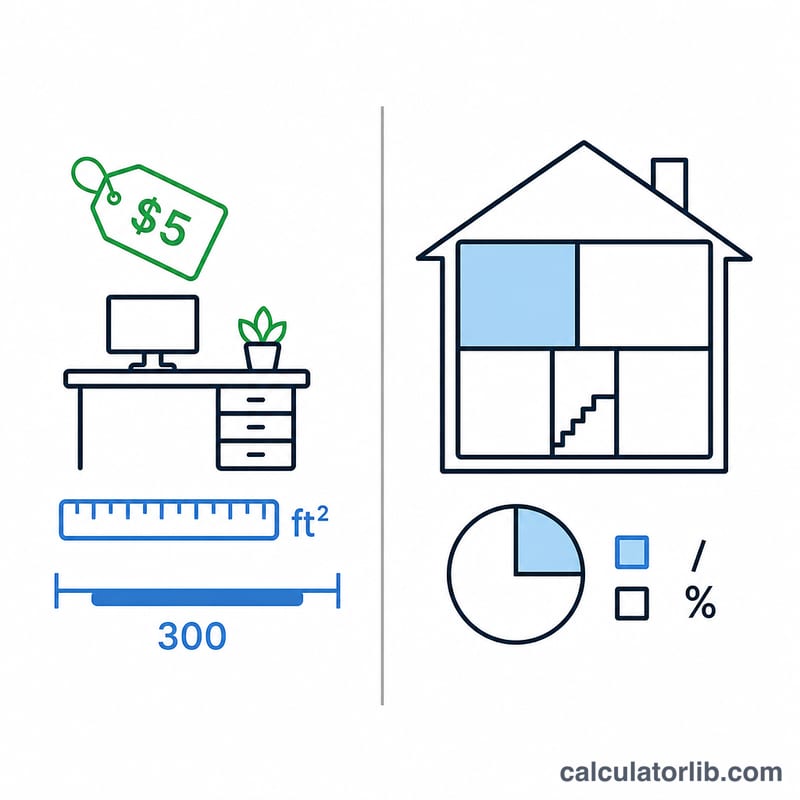

The simplified method is fixed at $5 per square foot, but only the first 300 square feet count — so the maximum is $1,500. The actual method allocates your real home expenses by the fraction of your home used for business: office area divided by total area. Choosing the bigger result generally maximizes your write-off.

$$\text{Deduction} = \max\left(\,\underbrace{5 \times \min\!\left(\text{Office (sq ft)},\,300\right)}_{\text{Simplified}},\ \underbrace{\text{Home Expenses} \times \frac{\text{Office (sq ft)}}{\text{Total (sq ft)}}}_{\text{Actual}}\,\right)$$

$$\text{Business \%} = \frac{\text{Office (sq ft)}}{\text{Total (sq ft)}} \times 100$$

Worked example

Suppose your office is 150 sq ft, your home is 1,500 sq ft, and annual home expenses total $20,000. Simplified: \(\min(150, 300) \times \$5\) = $750. Business-use percentage: \(150 / 1{,}500 = 10\%\). Actual: \(\$20{,}000 \times 10\%\) = $2,000. The actual method wins here, giving a $2,000 deduction.

FAQ

What is the maximum simplified deduction? $1,500 (\(300 \text{ sq ft} \times \$5\)).

Must the space be used exclusively for business? Generally yes — regular and exclusive business use is required, with limited exceptions like daycare or inventory storage.

Can employees claim this? Under current federal rules, the deduction is generally available to self-employed taxpayers, not W-2 employees. Check current IRS guidance or a tax professional.