What Is a Home Loan Eligibility Calculator?

This calculator estimates the maximum home loan you could qualify for based on your repayment capacity. Lenders rarely lend purely on the property value — they look at how much of your monthly income can comfortably service debt. The key ratio used is FOIR (Fixed Obligation to Income Ratio), the share of your monthly income that may go toward all loan EMIs combined. This tool is generic and works for any currency; FOIR norms and interest rates vary by lender and country.

How to Use It

Enter your net monthly income, the total of any EMIs you already pay, the FOIR your lender applies (commonly 40–55%), the annual interest rate, and the loan tenure in years. The calculator first finds your maximum affordable EMI, then converts that into the largest loan principal that EMI can support over the chosen tenure.

The Formula Explained

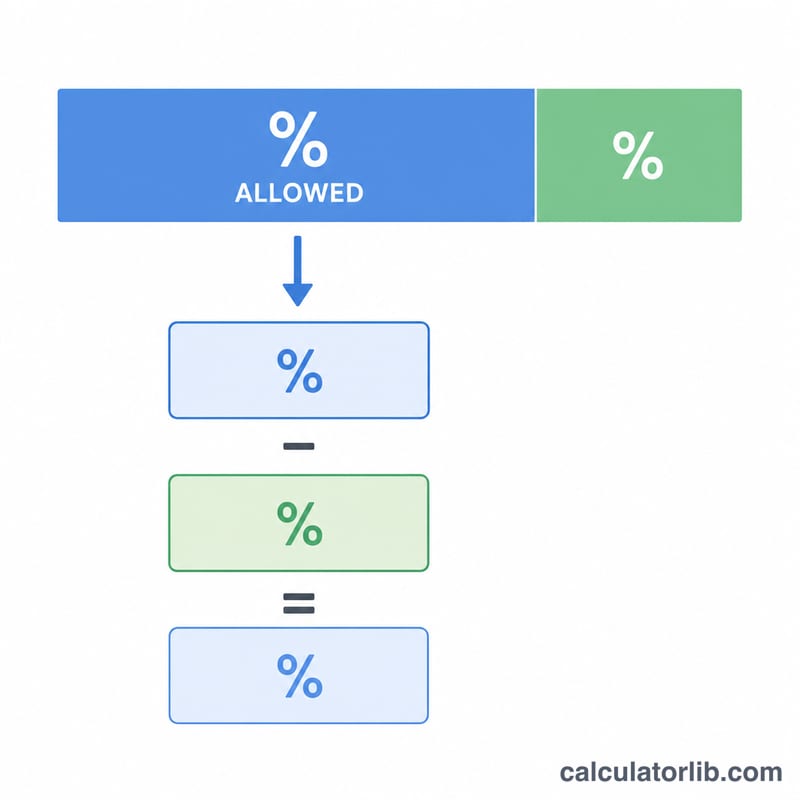

First, \( \text{MaxEMI} = \text{Income} \times (\text{FOIR}/100) - \text{ExistingEMI} \). This is the monthly amount left for a new loan. Then the maximum principal is the present value of that EMI stream:

$$ \text{MaxLoan} = \text{MaxEMI} \times \frac{1 - (1+i)^{-n}}{i} $$where \(i\) is the monthly interest rate (annual rate ÷ 12 ÷ 100) and \(n\) is the total number of monthly payments (years × 12).

Worked Example

Suppose your income is 60,000, existing EMIs are 5,000, FOIR is 50%, the rate is 9% per year, and the tenure is 20 years. \( \text{MaxEMI} = 60{,}000 \times 0.50 - 5{,}000 = 25{,}000 \). With \( i = 0.0075 \) and \( n = 240 \), the factor $$ \frac{1 - 1.0075^{-240}}{0.0075} \approx 111.145 $$ giving a maximum loan of about 2,778,627.

FAQ

What is a good FOIR? Many lenders cap FOIR at 40–55% of net income; lower FOIR usually means easier approval.

Does this guarantee approval? No. It is an estimate. Actual eligibility also depends on credit score, age, employment, and lender policy.

Can I increase my eligibility? Yes — reduce existing EMIs, choose a longer tenure, add a co-applicant, or find a lower interest rate.