What Is a Line of Credit Payment Calculator?

A line of credit (LOC) or home equity line of credit (HELOC) lets you borrow against an approved limit and pay interest only on what you use. This calculator estimates your monthly payment two ways: an interest-only payment (common during a HELOC's draw period) and a fully amortizing principal-and-interest payment that pays the balance to zero over a set term.

How to Use It

Enter your current outstanding balance, the annual interest rate (APR), the repayment term in months, and choose a payment type. The tool returns the monthly payment, the total interest you'll pay over the term, and the total amount repaid.

The Formula Explained

First convert the APR to a monthly rate: \(i = \text{APR} \div 100 \div 12\). For an interest-only payment, you simply pay the interest that accrues each month:

$$\text{PMT} = \text{Balance} \times i$$

— the principal never shrinks. For an amortizing payment, the standard annuity formula applies:

$$\text{PMT} = \frac{\text{Balance} \times i}{1 - (1 + i)^{-n}}$$

where \(n\) is the number of months. If the rate is 0%, the amortizing payment is simply \(\text{Balance} \div n\).

Worked Example

Suppose you owe $25,000 at 8.5% APR. The monthly rate is \(0.085 \div 12 = 0.00708333\). Interest-only:

$$25{,}000 \times 0.00708333 \approx \$177.08/\text{month}$$

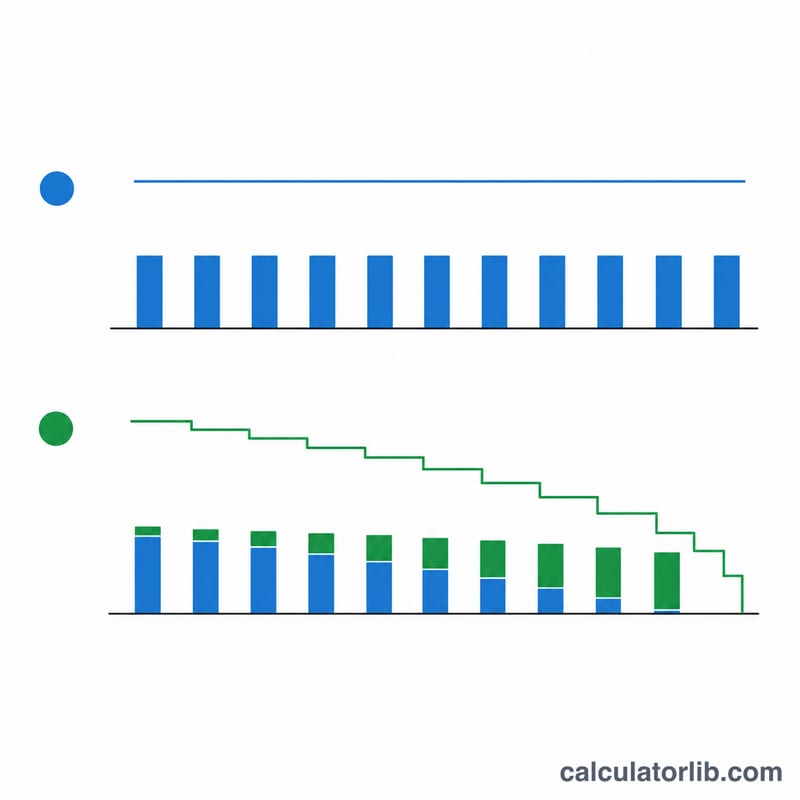

Over 120 months that's $21,250 in interest while the $25,000 principal still remains. Switching to a 120-month amortizing payment raises the monthly amount to about $309.96 but clears the debt entirely.

FAQ

Why is interest-only cheaper monthly? Because you aren't repaying any principal — the balance (and your future interest) stays the same.

What happens after a HELOC draw period? Many HELOCs switch from interest-only to amortizing payments, causing a "payment shock." Run both scenarios to plan ahead.

Does the rate change? Most HELOCs use a variable rate tied to the prime rate, so your real payment can rise or fall. This calculator assumes a fixed rate for estimation.