What Is the Payday Loan APR Calculator?

Payday loans advertise their cost as a small flat fee — for example, "$15 per $100 borrowed." That sounds cheap, but because the loan is repaid in just a couple of weeks, the annualized cost is enormous. This calculator converts the flat fee into a true Annual Percentage Rate (APR) so you can compare a payday loan against credit cards, personal loans, or any other form of credit on an equal footing.

How to Use It

Enter three numbers: the principal (the amount you actually receive), the total fee charged for the loan, and the term in days until repayment is due. The calculator returns the effective APR, the fee as a percentage of the principal, and the total amount you will repay.

The Formula Explained

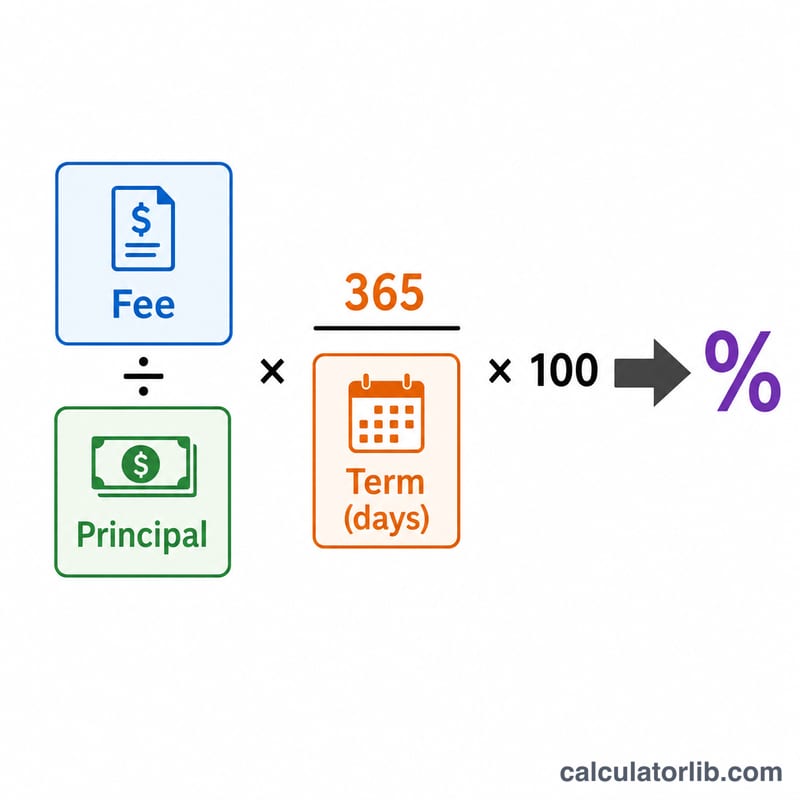

The APR is calculated as:

$$\text{APR} = \frac{\text{Fee}}{\text{Principal}} \times \frac{365}{\text{Term (days)}} \times 100\%$$

The first term, \(\text{Fee} \div \text{Principal}\), is the cost of the loan for its term. Multiplying by \(365 \div \text{Term}\) annualizes that cost — scaling a 14-day charge up to a full year. Multiplying by 100 expresses it as a percentage. This is a simple (non-compounding) APR, which is the standard disclosure method for short-term credit.

Worked Example

You borrow $500 and agree to repay $575 in 14 days. The fee is $75. The fee is 15% of the principal (\(\$75 \div \$500\)). Annualized: $$0.15 \times \left(\frac{365}{14}\right) \times 100 = 391.07\% \text{ APR}$$ A loan that felt like a modest $75 charge is actually borrowing money at nearly 391% a year.

FAQ

Why is the APR so high? Because the fee is charged over a very short period. Annualizing assumes you renew the loan repeatedly for a year, which reveals the true cost of relying on payday credit.

Does this include compounding? No. This uses the simple-interest APR method used in standard loan cost disclosures. Rolling a loan over multiple times would push the effective cost even higher.

What term should I use? Use the number of days between when you receive the money and when full repayment is due — typically until your next payday.