What Is Depreciation Recapture Tax?

This calculator applies to United States federal taxes. When you sell US real estate (rental property, commercial buildings) on which you previously claimed depreciation deductions, the IRS "recaptures" some of that benefit at sale. Under Section 1250, the portion of gain attributable to depreciation — known as unrecaptured Section 1250 gain — is taxed at a maximum federal rate of 25%, higher than the ordinary long-term capital gains rate. This estimate uses 2024-era rules and does not include state taxes or the 3.8% Net Investment Income Tax.

How to Use This Calculator

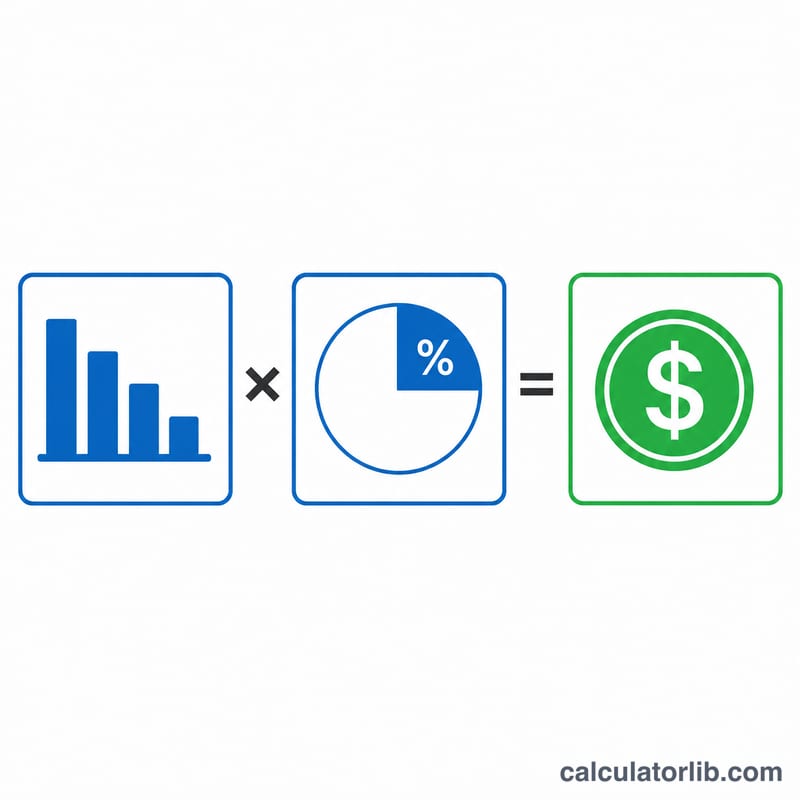

Enter the total accumulated depreciation you have claimed over the years you owned the property, then enter the recapture tax rate (the default 25% is the federal maximum for Section 1250 property). The calculator multiplies the two to estimate your recapture tax and shows what remains after the tax is applied.

The Formula Explained

The core math is simple:

$$\text{Recapture Tax} = \text{Accumulated Depreciation} \times \text{Rate}$$

Accumulated depreciation is the sum of all depreciation deductions taken. The 25% ceiling applies only to depreciation amounts; any gain above your original basis is taxed at regular capital gains rates and is not included here.

Worked Example

Suppose you owned a rental property and claimed $100,000 in total depreciation. At the 25% recapture rate: $$\$100{,}000 \times 0.25 = \$25{,}000$$ in depreciation recapture tax. After paying this tax on the recaptured amount, $75,000 remains.

FAQ

Is the rate always 25%? 25% is the federal maximum for unrecaptured Section 1250 gain. Your effective rate could be lower depending on your tax bracket.

Does this include state tax? No. Many states also tax recaptured depreciation; add your state rate separately.

What about the 3.8% NIIT? High earners may owe an additional 3.8% Net Investment Income Tax, which this calculator does not include.