What Is Home Equity?

Home equity is the share of your property that you truly own. It is the difference between your home's current market value and the amount you still owe on your mortgage and any other loans secured against the property. As you pay down your loan and as your home's value rises, your equity grows. Equity is a key measure of household wealth and determines how much you can borrow through a home equity loan or line of credit (HELOC).

How to Use This Calculator

Enter your home's current estimated market value and the total balance remaining on your mortgage. The calculator instantly returns your dollar equity, your equity as a percentage of the home's value, and your loan-to-value (LTV) ratio. Lenders typically allow you to borrow against equity until your combined LTV reaches about 80–85%.

The Formula Explained

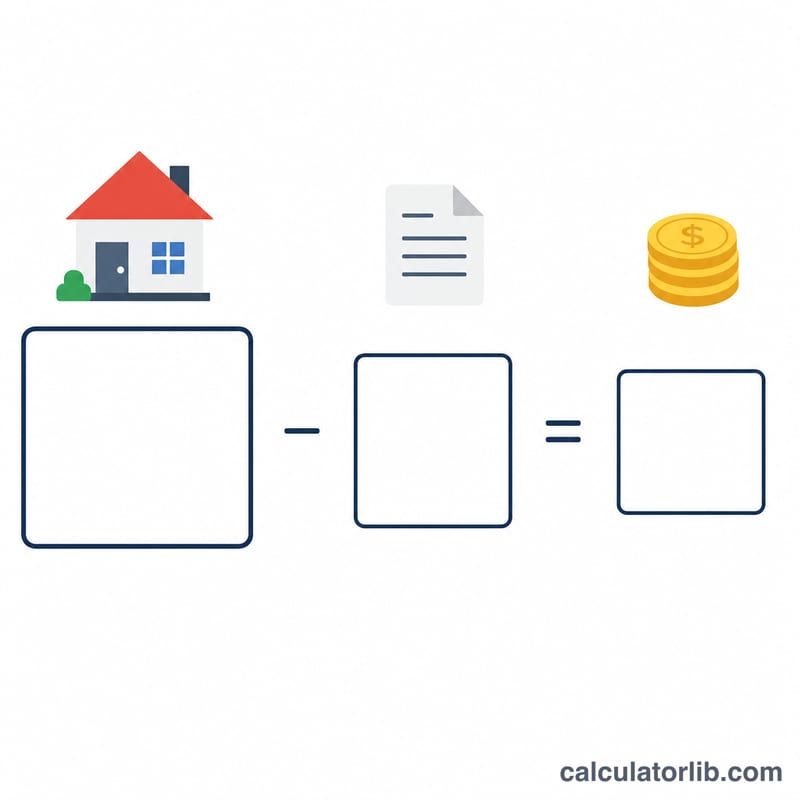

The math is simple: $$\text{Equity} = \text{Home Value} - \text{Mortgage Balance}$$. To express this as a percentage, divide equity by the home value and multiply by 100. The LTV ratio is the inverse view — the mortgage balance divided by the home value, times 100. A lower LTV (higher equity) means less risk to lenders and better borrowing options for you.

$$\text{Equity \%} = \frac{\text{Home Value} - \text{Mortgage Balance}}{\text{Home Value}} \times 100$$

$$\text{LTV} = \frac{\text{Mortgage Balance}}{\text{Home Value}} \times 100$$

Worked Example

Suppose your home is worth $400,000 and you still owe $250,000 on your mortgage. Your equity is $$\$400{,}000 - \$250{,}000 = \$150{,}000$$ As a percentage, that is $$\$150{,}000 \div \$400{,}000 \times 100 = 37.5\%$$ Your LTV is $$\$250{,}000 \div \$400{,}000 \times 100 = 62.5\%$$

FAQ

How can I increase my home equity? Pay down your mortgage faster, make extra principal payments, or make improvements that raise your home's market value.

What is a good equity percentage? Many lenders want you to keep at least 15–20% equity, meaning an LTV of 80–85% or lower, before approving additional borrowing.

Does home value mean the price I paid? No — use the current market value (from a recent appraisal or comparable sales), not the original purchase price, for an accurate result.