What is available home equity?

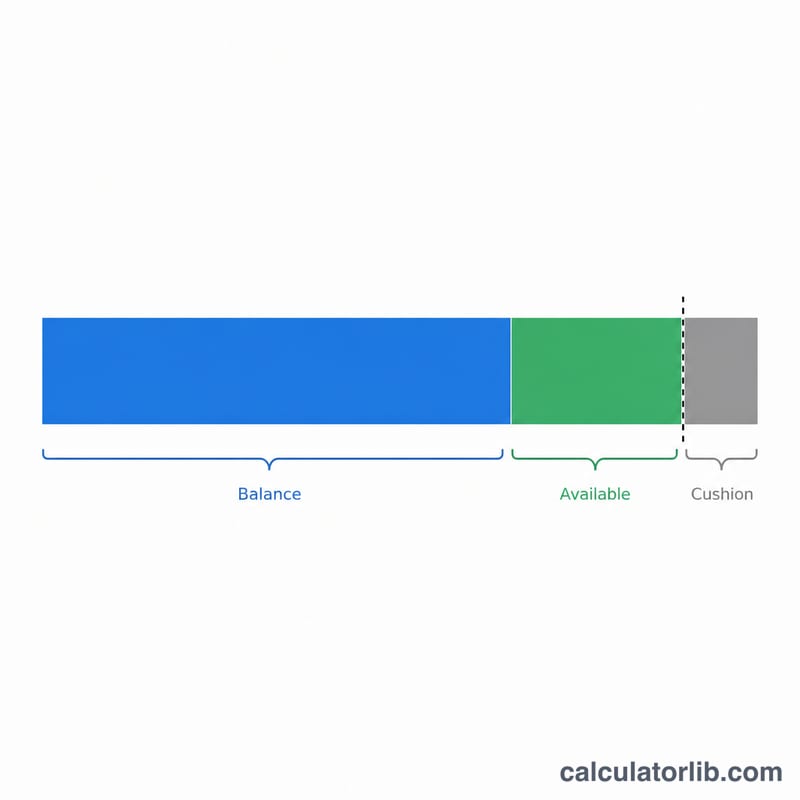

Available home equity is the portion of your property's value that a lender will let you borrow against, after accounting for your existing mortgage. Lenders cap total borrowing at a maximum combined loan-to-value (CLTV) ratio — commonly 80% to 90% — which limits how much you can tap with a home equity loan or HELOC.

How to use this calculator

Enter your current home value (use a recent appraisal or estimate), your outstanding mortgage balance, and the maximum CLTV your lender allows. The calculator multiplies the value by the CLTV to find your maximum allowed borrowing, then subtracts what you still owe to show the equity you could actually access.

The formula explained

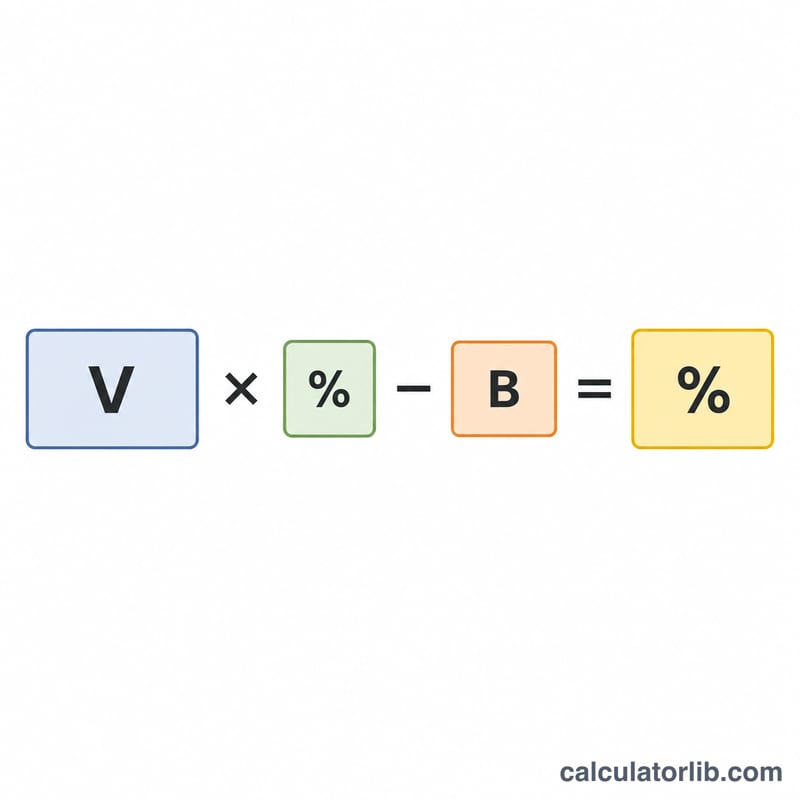

The core equation is $$\text{Available} = \text{Value} \times \text{maxCLTV} - \text{Mortgage Balance}$$ For example, an 80% CLTV on a home means a lender will permit total secured debt up to 80% of the home's worth. Whatever remains after your first mortgage is your borrowing room. The tool also reports your current loan-to-value (LTV) so you can see how leveraged you already are.

Worked example

Suppose your home is worth $400,000, you owe $250,000, and your lender allows an 80% CLTV. Maximum borrowing $$= \$400{,}000 \times 0.80 = \$320{,}000.$$ Subtract the $250,000 balance and you have $70,000 of available equity to borrow. Your current LTV is \(\$250{,}000 \div \$400{,}000 = 62.5\%\).

FAQ

Why does the result show $0? If your mortgage balance already exceeds the maximum borrowing at your CLTV, there is no room left to borrow, so the result is floored at zero.

What CLTV should I use? Many lenders cap home equity products at 80–85% CLTV, though some go up to 90% or more. Check your lender's specific limit.

Is this a loan approval? No. This is an estimate. Actual borrowing also depends on your income, credit score, and the lender's underwriting rules.