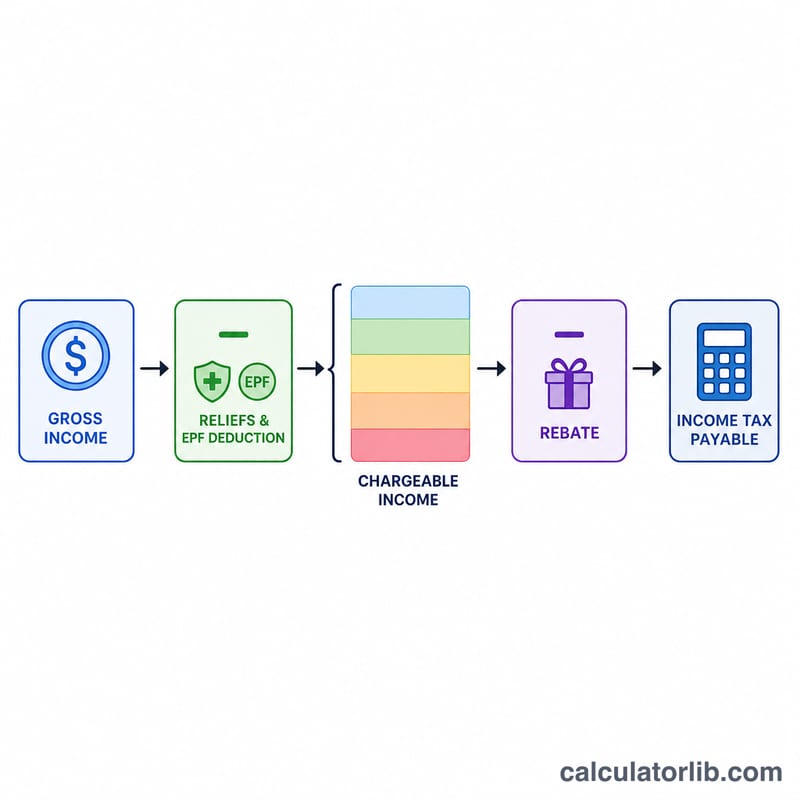

What This Calculator Does

This tool estimates personal income tax for Malaysian tax residents for the Year of Assessment 2024 (YA2024), administered by LHDN (Inland Revenue Board). It applies the resident progressive tax bands, subtracts your personal reliefs, and applies the RM400 rebate available when chargeable income does not exceed RM35,000. It assumes you are a tax resident; non-residents are taxed at a flat 30% and are out of scope.

How to Use It

Enter your total annual income, your EPF or approved-fund contributions (relief capped at RM4,000), any other reliefs you qualify for (lifestyle, medical, education, etc.), and your marital status. The default RM9,000 individual relief is applied automatically, plus RM4,000 if you support a spouse with no income.

The Formula Explained

First, chargeable income = annual income − total reliefs. Then the YA2024 resident bands are applied progressively: 0% up to RM5,000; 1% on the next RM15,000; 3% next RM15,000; 6% next RM15,000; 11% next RM20,000; 19% next RM30,000; 25% next RM300,000; 26%, 28% and 30% on higher bands. Finally a RM400 rebate (RM800 if married) is deducted when chargeable income ≤ RM35,000.

$$\text{Tax Payable} = \operatorname{Progressive}(C) - \text{Rebate}$$

$$\text{where}\quad \left\{ \begin{aligned} C &= \text{Income} - 9000 - \min\!\left(\text{EPF},\,4000\right) - \text{Reliefs} \\ \text{Rebate} &= 400 \;\text{ if } C \le 35000 \end{aligned} \right.$$

Worked Example

A single taxpayer earns RM60,000 with RM4,000 EPF. Reliefs = RM9,000 + RM4,000 = RM13,000, so chargeable income = RM47,000. Tax = 0 + (15,000×1%) + (15,000×3%) + (12,000×6%) = 150 + 450 + 720 = RM1,320. Chargeable income exceeds RM35,000, so no rebate applies — tax payable is RM1,320.

$$\text{Reliefs} = 9000 + 4000 = 13000$$

$$\text{Chargeable income} = 60000 - 13000 = 47000$$

$$\text{Tax} = 0 + (15000 \times 1\%) + (15000 \times 3\%) + (12000 \times 6\%) = 150 + 450 + 720 = 1320$$

FAQ

Is the EPF relief really capped? Yes — EPF plus life insurance relief is capped at RM4,000 for YA2024.

Who gets the RM400 rebate? Residents whose chargeable income is RM35,000 or less; a spouse with no income adds another RM400.

Is this an official figure? No. It is an estimate to plan with — always confirm with LHDN or a tax professional.