What Is Tax-Equivalent Yield?

Tax-equivalent yield (TEY) tells you how much a fully taxable investment would have to yield to match the after-tax return of a tax-free investment, such as a municipal bond. Because the interest on many municipal bonds escapes income tax, a seemingly modest tax-free yield can be worth far more than its headline rate to a high-bracket investor. This calculator converts a tax-free yield into its taxable equivalent so you can compare apples to apples.

How to Use It

Enter the tax-free yield of the investment you are considering, then enter your marginal tax rate — the rate applied to your next dollar of income. Click calculate and you'll see the taxable yield you would need to earn the same after-tax return, plus the yield advantage the tax-free option provides.

The Formula Explained

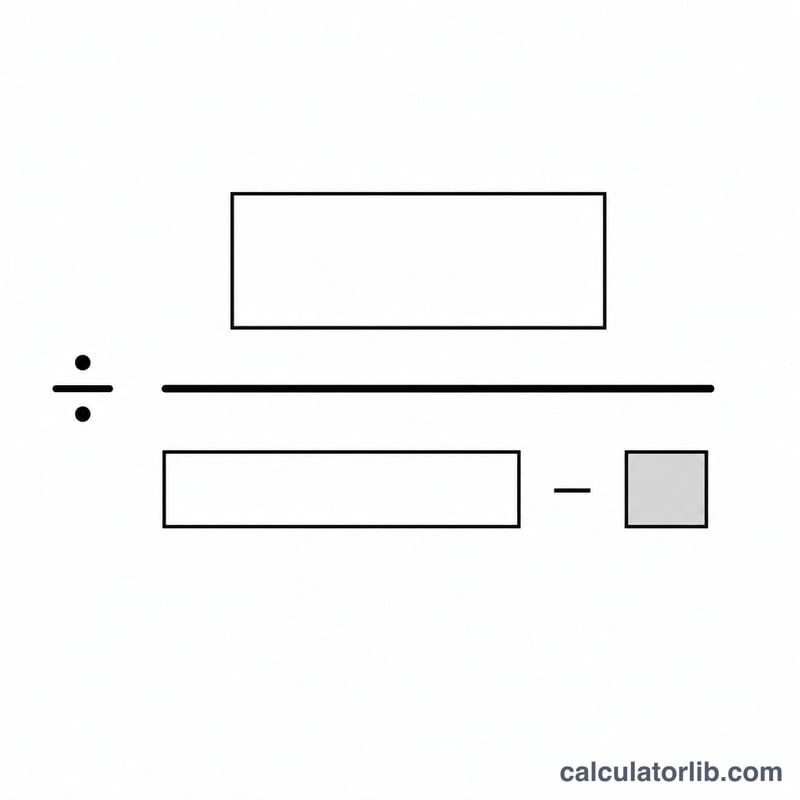

The relationship is simple: $$\text{TEY} = \frac{\text{Tax-Free Yield (\%)}}{1 - \dfrac{\text{Tax Rate (\%)}}{100}}$$. Dividing by one minus your tax rate "grosses up" the tax-free yield to account for the taxes you would otherwise pay. The higher your tax bracket, the larger the gross-up and the more attractive tax-free investments become.

Worked Example

Suppose a municipal bond yields 3.5% tax-free and your marginal tax rate is 24%. The taxable equivalent is $$3.5 \div (1 - 0.24) = 3.5 \div 0.76 \approx 4.605\%$$ So a taxable bond would need to yield about \(4.61\%\) to leave you with the same money after taxes — a yield advantage of roughly 1.1 percentage points.

FAQ

Which tax rate should I use? Use your combined marginal rate. For US investors comparing in-state municipal bonds, you can include federal plus state (and local) rates if the bond is exempt from all of them.

Does this account for the AMT or de minimis rules? No. This is a simplified comparison and ignores the alternative minimum tax, capital-gains treatment, and other special situations. Consult a tax professional for decisions.

Why does my answer get huge near 100%? As the tax rate approaches 100%, the divisor approaches zero and the equivalent yield grows without bound, which is why the model caps the rate below 100%.