What Is Yield to Call?

Yield to call (YTC) estimates the annualized return an investor earns on a callable bond if the issuer redeems (calls) it on the earliest possible call date rather than holding it to maturity. Because issuers often call bonds when interest rates fall, YTC is a key downside-yield measure for callable bonds, frequently compared against yield to maturity to find the lower "yield to worst."

How to Use This Calculator

Enter the bond's face (par) value, its current market price, the call price (what the issuer pays to redeem it), the annual coupon rate as a percentage, and the number of years until the call date. The calculator derives the annual coupon payment and returns the approximate YTC as an annualized percentage.

The Formula Explained

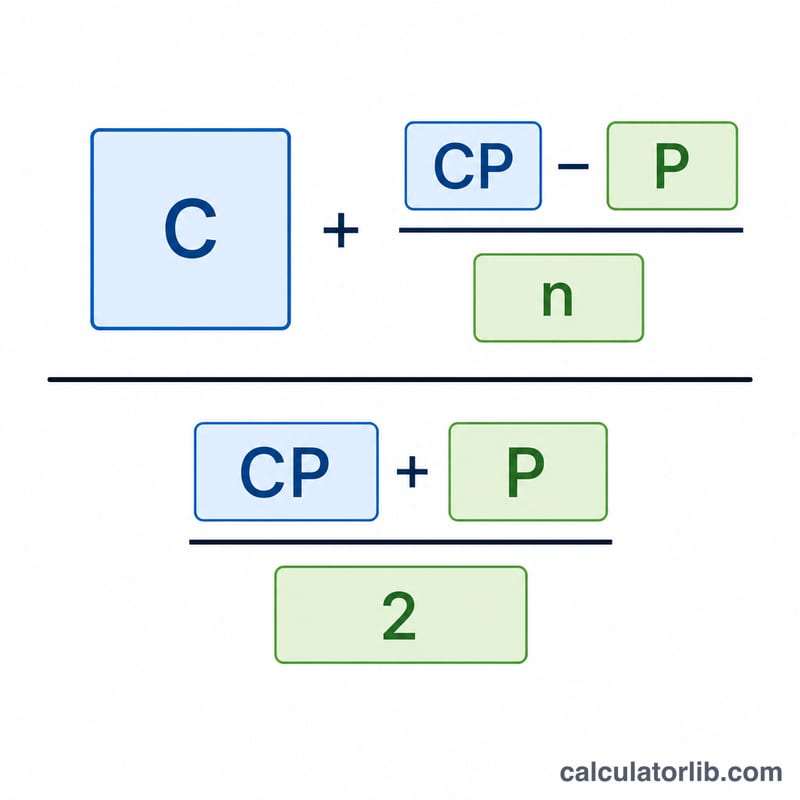

The approximation is $$\text{YTC} \approx \frac{C + \dfrac{\text{CP} - \text{P}}{n}}{\dfrac{\text{CP} + \text{P}}{2}}$$, where \(C\) is the annual coupon dollar amount, \(\text{CP}\) is the call price, \(\text{P}\) is the current price, and \(n\) is the years to call. The numerator adds the coupon income to the per-year price gain or loss toward the call price; the denominator is the average of the call price and current price, approximating the average invested capital.

Worked Example

A bond with $1,000 face value pays an 8% coupon ($80/year). It trades at $1,050, is callable at $1,100 in 5 years. Numerator: \(80 + (1100 - 1050)/5 = 80 + 10 = 90\). Denominator: \((1100 + 1050)/2 = 1075\). $$\text{YTC} \approx 90 / 1075 = 0.08372 \approx 8.37\%$$

FAQ

Is this exact? No — it is the standard approximation. A precise YTC requires solving for the rate that sets discounted cash flows equal to price, but this estimate is close for most bonds.

YTC vs YTM? YTM assumes you hold to maturity; YTC assumes the bond is called on the call date. Investors use the lower of the two as "yield to worst."

Why include a call premium? Many bonds are called above par (e.g., $1,100 on a $1,000 bond) to compensate holders for early redemption — that premium boosts YTC.