What Is Adjusted Gross Income (AGI)?

This calculator applies to the United States federal income tax system. Adjusted Gross Income (AGI) is your total gross income from all sources, reduced by specific "above-the-line" deductions allowed by the IRS. AGI is one of the most important numbers on your tax return because it determines your eligibility for many credits, deductions, and contribution limits. Figures here are general estimates and not tax advice; consult the current IRS instructions or a tax professional for your specific situation.

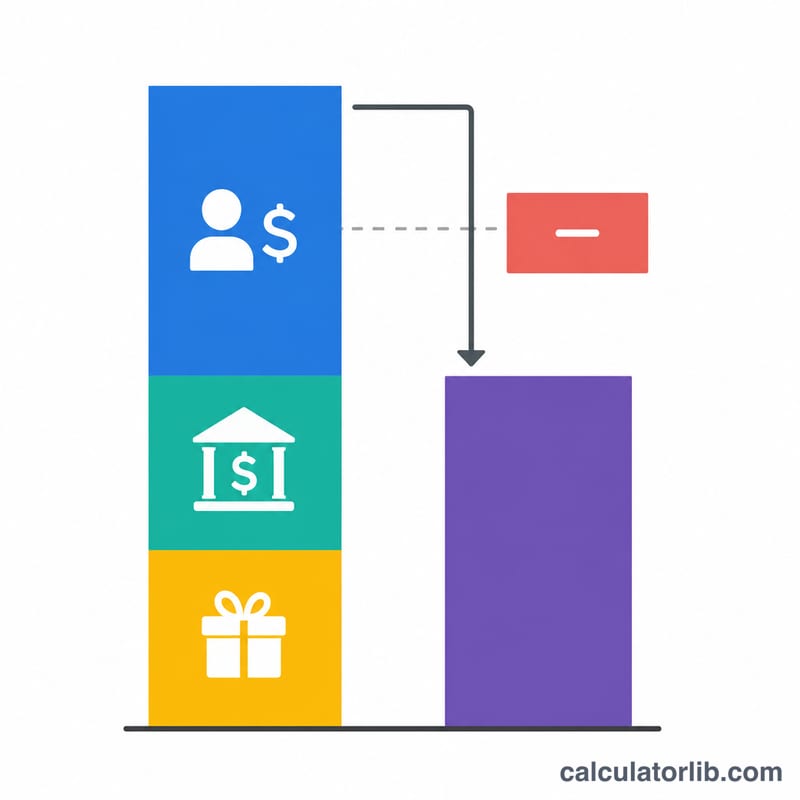

How to Use This Calculator

Enter every source of income — wages and salary, interest and dividends, self-employment or business income, and any other taxable income. Then enter your above-the-line adjustments such as deductible IRA or SEP retirement contributions, Health Savings Account (HSA) contributions, student loan interest, and any other eligible adjustments. The tool adds your income, subtracts your adjustments, and shows your AGI instantly.

The Formula Explained

The calculation is straightforward: $$\text{AGI} = \text{Total Gross Income} - \text{Above-the-Line Adjustments}$$ Gross income is the sum of all taxable money you received during the year. Above-the-line adjustments are subtracted before you choose the standard or itemized deduction, which is why they are valuable — everyone who qualifies can claim them.

Worked Example

Suppose you earned $60,000 in wages and $500 in interest, giving $60,500 of gross income. You contributed $6,000 to a traditional IRA. Your AGI is $$\$60{,}500 - \$6{,}000 = \$54{,}500$$ That lower number could improve your eligibility for income-based tax breaks.

Above-the-Line Adjustment Limits

Above-the-line adjustments (officially "adjustments to income" on Schedule 1 of Form 1040) reduce your gross income to arrive at your Adjusted Gross Income (AGI). The figures below are general IRS amounts for the 2024 tax year; verify against current IRS instructions, since limits are adjusted annually for inflation and phase-outs depend on your filing status.

| Adjustment | 2024 Annual Limit | Key Eligibility / Phase-out Notes |

|---|---|---|

| Traditional IRA contribution | $7,000 (under 50); $8,000 (50+) | Full deduction phases out for active workplace-plan participants (e.g. MFJ $123,000–$143,000; single $77,000–$87,000 MAGI). |

| HSA — self-only coverage | $4,150 (+$1,000 if 55+) | Requires an HSA-qualified high-deductible health plan; no other disqualifying coverage. |

| HSA — family coverage | $8,300 (+$1,000 if 55+) | Same HDHP eligibility rules; the $1,000 catch-up is per spouse and must go in each spouse's own HSA. |

| Student loan interest | Up to $2,500 | Phases out (single $80,000–$95,000; MFJ $165,000–$195,000 MAGI). Cannot be married filing separately. |

| Educator expenses | Up to $300 ($600 if both spouses are eligible educators) | For K–12 teachers, instructors, counselors, principals or aides working 900+ hours. |

| SEP-IRA / Solo 401(k) | Up to $69,000 (employer side) | Limited to 25% of compensation (SEP) or the combined employee/employer limit (Solo 401(k)); for the self-employed. |

| Deductible self-employment tax | ~50% of SE tax paid | The employer-equivalent half of Social Security and Medicare self-employment tax. |

This table is general information, not tax advice. Confirm amounts and phase-out thresholds with IRS Publication 17 and the Form 1040 / Schedule 1 instructions for your tax year.

Key Terms Defined

- Gross Income

- All income you receive that is subject to tax before any adjustments — wages, interest and dividends, business income, capital gains, taxable retirement distributions, and other income.

- Above-the-Line Adjustment

- A deduction subtracted directly from gross income to compute AGI (reported on Schedule 1). Examples include IRA and HSA contributions, student loan interest, and the deductible portion of self-employment tax. They are available whether or not you itemize.

- Adjusted Gross Income (AGI)

- Gross income minus above-the-line adjustments. Reported on Form 1040 line 11, it is the baseline for many income-based limits.

- Modified Adjusted Gross Income (MAGI)

- AGI with certain deductions and exclusions added back (e.g. student loan interest, tax-exempt interest, foreign earned income). Used to determine eligibility for many credits and contribution limits; its exact definition varies by provision.

- Taxable Income

- AGI minus your standard deduction or itemized deductions (and any qualified business income deduction). This is the amount to which tax rates are actually applied.

- Standard Deduction

- A fixed dollar amount, based on filing status, that reduces AGI to taxable income without itemizing.

- Itemized Deduction

- Specific allowable expenses (such as mortgage interest, state and local taxes up to the cap, and charitable gifts) claimed on Schedule A instead of the standard deduction when they total more.

- Phase-out

- The gradual reduction or elimination of a tax benefit as income (AGI or MAGI) rises through a defined range, until the benefit reaches zero at the top of the range.

FAQ

Is AGI the same as taxable income? No. Taxable income is AGI minus your standard or itemized deduction (and any qualified business income deduction). AGI comes first.

What counts as an above-the-line adjustment? Common ones include deductible IRA/SEP contributions, HSA contributions, the deductible portion of self-employment tax, student loan interest, and educator expenses.

Why does AGI matter? Many credits and deductions phase out based on AGI (or modified AGI), so lowering it can unlock additional tax savings.