What Is a 1031 Exchange?

This calculator applies to United States federal tax law under IRC Section 1031. A 1031 (or "like-kind") exchange lets real estate investors defer capital gains tax by reinvesting the proceeds from selling an investment property into another qualifying property. The tax is not eliminated — it is postponed until you eventually sell without exchanging. Rules reflect current US law; consult a qualified intermediary and tax professional, as IRS rules and rates can change.

How to Use It

Enter the sale price of the property you are giving up (the relinquished property), your adjusted basis (original cost plus improvements minus depreciation), and any selling/closing costs. Then enter any boot you receive — cash taken out plus net debt relief (mortgage boot) — and your applicable capital gains tax rate. The tool computes your realized gain, how much is taxable now, and how much tax you defer.

The Formula Explained

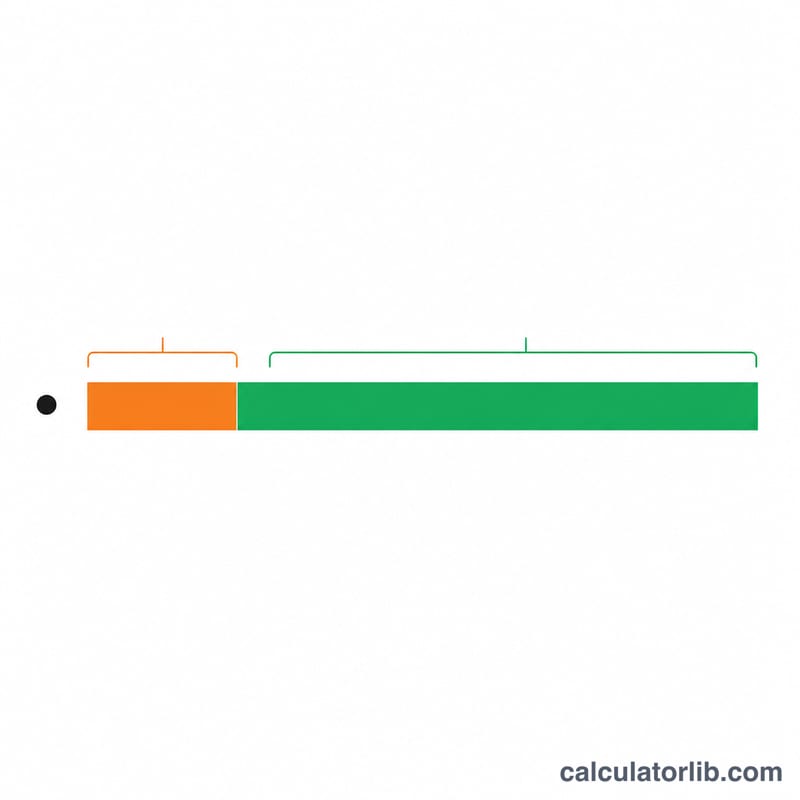

First, realized gain = (sale price − selling costs) − adjusted basis. In a fully like-kind reinvestment you would defer all of it. But any boot received is taxable: recognized gain = min(boot, realized gain). The leftover, deferred gain = realized gain − recognized gain, rolls forward into the replacement property's basis. Tax due now equals recognized gain × tax rate; tax deferred equals deferred gain × tax rate.

$$\text{Realized Gain} = (\text{Sale Price} - \text{Selling Costs}) - \text{Adjusted Basis}$$

$$\text{Recognized Gain} = \min(\text{Boot},\ \text{Realized Gain})$$

$$\text{Deferred Gain} = \text{Realized Gain} - \text{Recognized Gain}$$

Worked Example

You sell a rental for $500,000 with $30,000 in selling costs and an adjusted basis of $300,000. Realized gain = (500,000 − 30,000) − 300,000 = $170,000.

$$\text{Realized Gain} = (500{,}000 - 30{,}000) - 300{,}000 = 170{,}000$$

You take $20,000 cash boot. Recognized gain = min(20,000, 170,000) = $20,000, so deferred gain = $150,000.

$$\text{Recognized Gain} = \min(20{,}000,\ 170{,}000) = 20{,}000$$

$$\text{Deferred Gain} = 170{,}000 - 20{,}000 = 150{,}000$$

At a 20% rate, you owe $4,000 now and defer $30,000 of tax.

2024 Federal Long-Term Capital Gains Tax Rates

A fully deferred 1031 exchange postpones the federal tax that would otherwise apply to your gain. To understand the size of that benefit, it helps to know which rates would apply if you simply sold the property and recognized the gain. For assets held longer than one year, the federal long-term capital gains rate is 0%, 15%, or 20%, depending on taxable income and filing status.

| Rate | Single | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | Up to $47,025 | Up to $94,050 | Up to $63,000 |

| 15% | $47,026 – $518,900 | $94,051 – $583,750 | $63,001 – $551,350 |

| 20% | Over $518,900 | Over $583,750 | Over $551,350 |

Two additional charges commonly stack on top of these base rates for investment real estate:

| Surcharge | Rate | Applies to |

|---|---|---|

| Unrecaptured Section 1250 gain (depreciation recapture) | Up to 25% | The portion of gain attributable to prior depreciation deductions on the property |

| Net Investment Income Tax (NIIT) | 3.8% | Net investment income for filers above MAGI thresholds ($200,000 single, $250,000 MFJ) |

Because these can combine, the effective rate on a recognized real-estate gain can meaningfully exceed the headline 15% or 20% figure. For example, a high-income investor recognizing gain might face a 20% long-term rate plus the 3.8% NIIT, for a combined $3,800 NIIT charge on $100,000 of investment income — all of which a fully qualifying exchange can defer.

2024 figures shown are federal only and do not include state income tax. Always confirm current thresholds and your own marginal situation with a tax professional.

Key 1031 Exchange Terms

- Relinquished property

- The property you currently own and are selling (giving up) in the exchange.

- Replacement property

- The like-kind property you acquire to complete the exchange and into which the gain is rolled.

- Adjusted basis

- Your original cost plus capital improvements, minus accumulated depreciation. It is subtracted from net sale proceeds to determine realized gain.

- Cash boot

- Non-like-kind value you receive, such as cash retained at closing or sale proceeds not reinvested. Boot is taxable up to the amount of realized gain.

- Mortgage (debt) boot

- A net reduction in liabilities — when the debt on the replacement property is less than the debt paid off on the relinquished property. The shortfall is treated like cash boot and may be taxed.

- Realized gain

- The total economic gain on the sale: net sale price minus adjusted basis, regardless of how much is taxed currently.

- Recognized gain

- The portion of realized gain that is currently taxable. In a proper 1031 exchange this is limited to the boot received.

- Deferred gain

- Realized gain that is not recognized now because it is rolled into the replacement property; it is postponed, not forgiven.

- Qualified intermediary (QI)

- An independent third party who holds the sale proceeds and facilitates the exchange so the taxpayer never takes constructive receipt of the funds.

- Like-kind property

- Real property held for productive use in a trade or business or for investment. Since 2018, Section 1031 applies only to real property, not personal property.

Understanding Your Results

The calculator estimates how much capital gains tax a like-kind exchange lets you postpone. A few important points help put the numbers in context.

Deferred, not eliminated. A 1031 exchange does not erase your tax bill — it postpones it. The gain you defer remains attached to the replacement property and is generally recognized when that property is later sold in a taxable transaction. Some investors continue exchanging across multiple properties and ultimately rely on a stepped-up basis at death, but absent that, the deferred tax eventually comes due.

Lower replacement basis. Because the gain carries over, your replacement property takes a reduced (carryover) basis: roughly its purchase price minus the deferred gain. This lower basis means smaller future depreciation deductions and a larger taxable gain when you eventually sell.

Strict deadlines. To qualify, you must identify potential replacement property within 45 days of selling the relinquished property, and you must close on the replacement within 180 days (or the due date of your tax return, if earlier). Both clocks start at the closing of the relinquished property and are not extendable except in narrow disaster-relief situations.

Equal or greater value and debt. To defer the entire gain, the replacement property must be of equal or greater value, you must reinvest all net proceeds, and you must replace at least as much debt as you paid off (or add equivalent cash). Any shortfall — cash kept or a net reduction in debt — is treated as boot and is taxed up to the amount of realized gain.

Depreciation recapture still applies. Even in a fully qualifying exchange, recognized boot can trigger unrecaptured Section 1250 gain taxed at up to 25%, and a later taxable sale will bring the recaptured depreciation back into income. The exchange defers this along with the rest of the gain, but it does not change its character.

This is general educational information, not tax or legal advice. 1031 exchanges have strict technical requirements, and an error can disqualify the entire transaction. Consult a qualified intermediary and a tax professional before proceeding.

FAQ

What is boot? Boot is any non-like-kind value you receive — cash withdrawn or a reduction in mortgage debt that isn't replaced. It triggers immediate taxation.

Can I defer 100% of my gain? Yes, if you reinvest all proceeds, take no cash, and acquire equal or greater debt — leaving zero boot.

Does this include depreciation recapture? This is a simplified estimate using a single blended rate; depreciation recapture (taxed up to 25%) may apply to part of your gain. See a tax advisor.