What This Calculator Does

This tool applies to United States self-employed taxpayers who receive 1099 income (freelancers, contractors, gig workers, sole proprietors). It estimates your self-employment (SE) tax, your federal income tax, and the quarterly estimated payment you should send to the IRS. Figures use the standard SE tax structure (15.3% combined Social Security and Medicare on 92.35% of net profit). It is a planning estimate only and does not model the Social Security wage cap, the additional Medicare tax, state taxes, credits, or the QBI deduction.

How to Use It

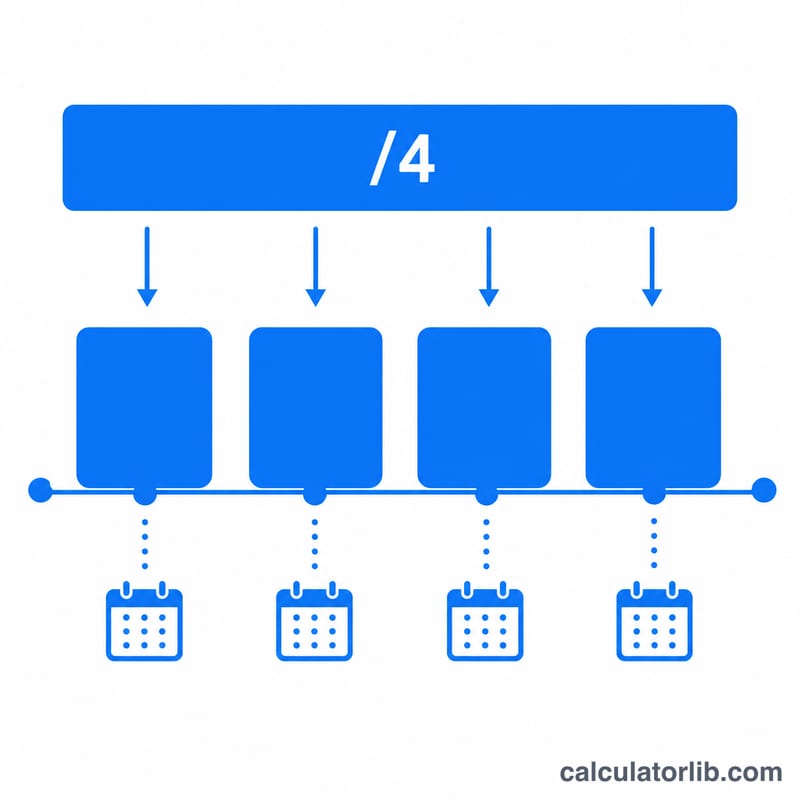

Enter your expected annual net self-employment profit (revenue minus business expenses). Enter an estimated income tax rate — your effective federal rate, often 10–24% depending on bracket and filing status. Optionally add other deductions (such as the standard deduction or retirement contributions) that reduce income-taxable amounts. The calculator returns your total tax and divides it into four equal quarterly payments.

The Formula Explained

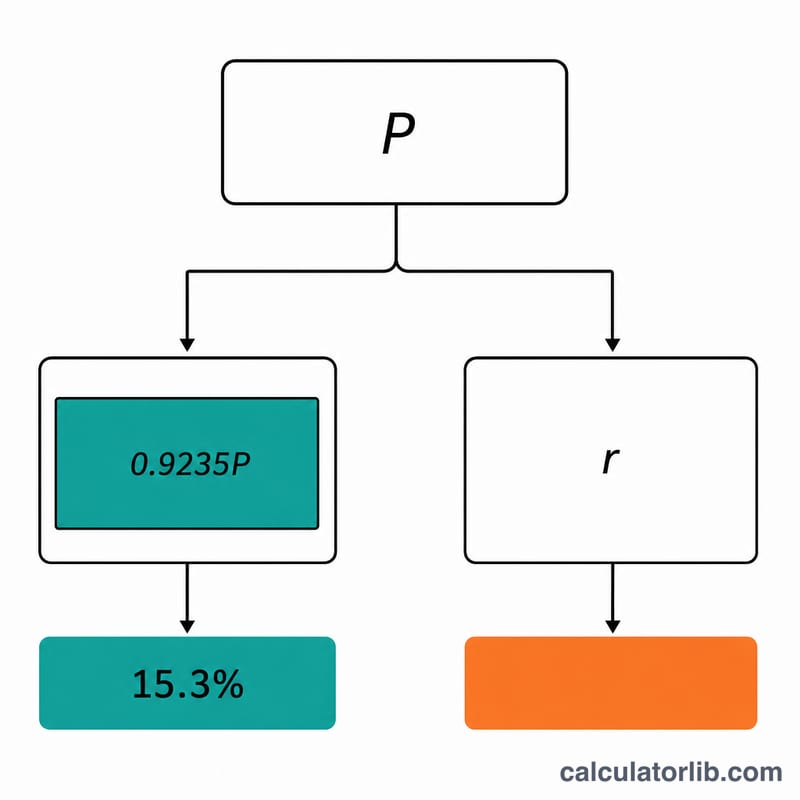

The IRS taxes only 92.35% of net profit for SE purposes, so SE tax = \(0.9235 \times \text{profit} \times 0.153\). You can deduct half of that SE tax before computing income tax. Income tax then applies to (net profit − half SE tax − other deductions) at your chosen rate. Total tax = SE tax + income tax, and the quarterly amount is that total ÷ 4.

$$\begin{gathered} Q = \dfrac{T_{SE} + T_{inc}}{4} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} T_{SE} &= 0.153 \times 0.9235 \times \text{Net Profit} \\ T_{inc} &= \left(\text{Net Profit} - \tfrac{T_{SE}}{2} - \text{Other Deductions}\right) \times \dfrac{\text{Income Tax Rate}}{100} \end{aligned} \right. \end{gathered}$$

Worked Example

Suppose net profit is $60,000 with a 12% income tax rate and no extra deductions. SE base = \(0.9235 \times 60{,}000 = \$55{,}410\). SE tax = \(55{,}410 \times 0.153 = \$8{,}477.73\). Half of SE tax = $4,238.865. Income-taxable = \(60{,}000 - 4{,}238.865 = \$55{,}761.135\), taxed at 12% = $6,691.34. Total tax ≈ $15,169.07, so each quarterly payment is about $3,792.27.

FAQ

When are quarterly taxes due? Generally April 15, June 15, September 15, and January 15 of the following year.

Why is the SE tax 15.3%? It combines the 12.4% Social Security and 2.9% Medicare taxes that an employer and employee normally split — as a self-employed person you pay both halves.

Is this exact? No. It is a fast estimate. Consult a tax professional and IRS Form 1040-ES for filing.