What is the Self-Employment Tax?

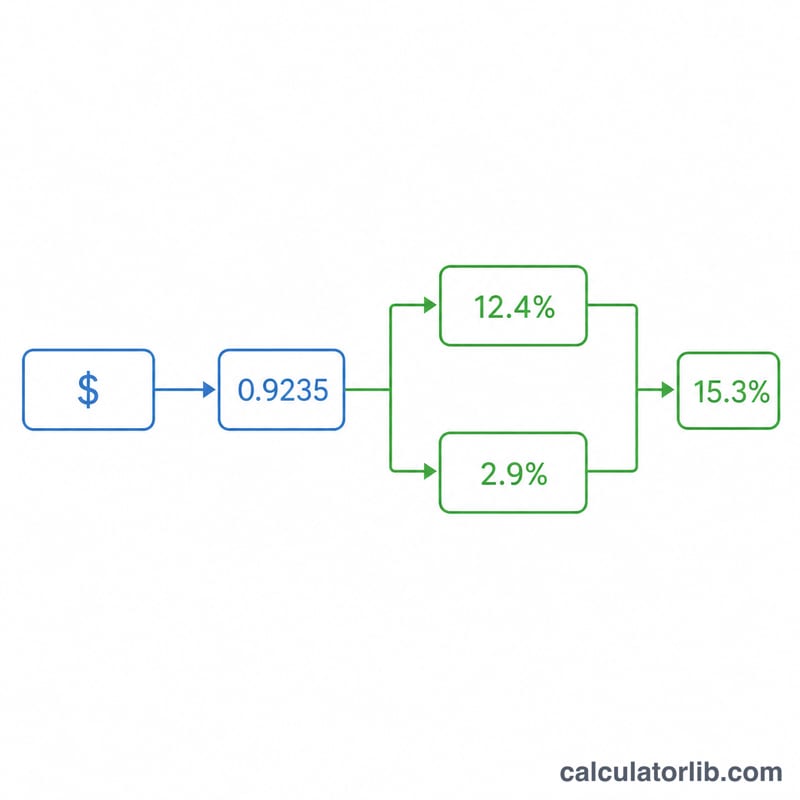

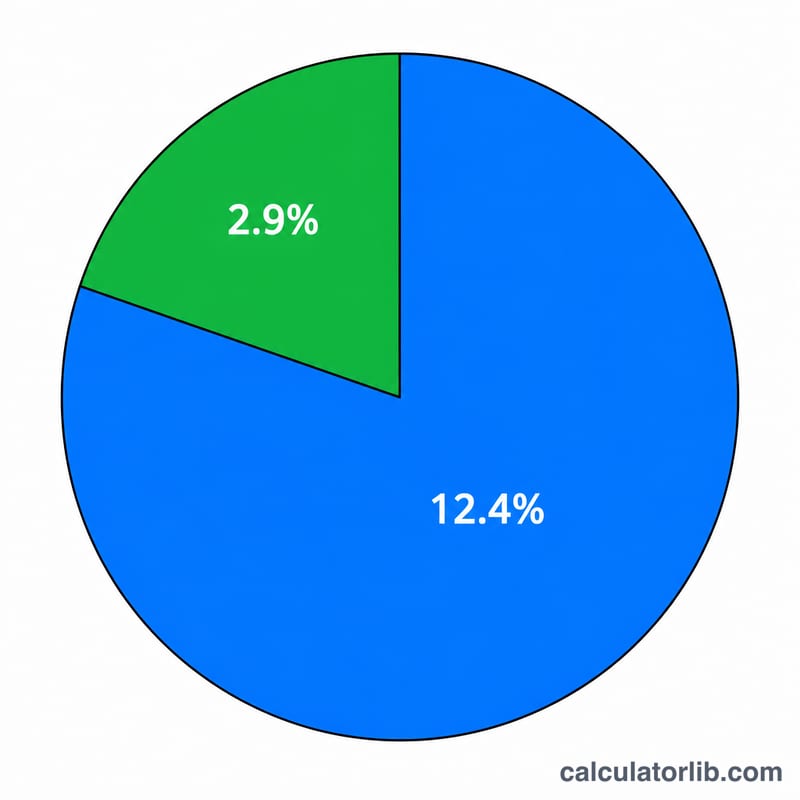

This calculator applies to the United States and uses 2026 tax-year rules. Self-employment (SE) tax is how independent contractors, freelancers, and sole proprietors pay Social Security and Medicare taxes — the equivalent of the FICA taxes a W-2 employer and employee split. Because you are both employer and employee, you pay both halves: a combined 15.3% rate, made up of 12.4% for Social Security and 2.9% for Medicare.

How to Use It

Enter your net self-employment profit (business income minus deductible business expenses, from Schedule C). If you also earned W-2 wages this year, enter the amount that was subject to Social Security tax — this reduces the remaining Social Security wage base available for your SE income. The calculator returns your total SE tax, the Social Security and Medicare portions, and the deductible one-half of SE tax you can subtract when figuring adjusted gross income.

The Formula Explained

First, only 92.35% of your net profit counts as taxable net earnings: \(\text{Net Earnings} = \text{Net Profit} \times 0.9235\). The Social Security portion (12.4%) applies only up to the annual wage base — $184,500 for 2026 — minus any W-2 wages already taxed. The Medicare portion (2.9%) has no cap. Adding them gives your total SE tax.

$$\begin{gathered} \text{SE Tax} = 0.124 \times \min(NE,\; B) + 0.029 \times NE \\[1.5em] \text{where}\quad \left\{ \begin{aligned} NE &= \max\!\left(0,\; 0.9235 \times \text{Net Profit}\right) \\ B &= \max\!\left(0,\; 184500 - \text{W-2 Wages}\right) \end{aligned} \right. \end{gathered}$$

Worked Example

Suppose your net profit is $50,000. Net earnings = \(50{,}000 \times 0.9235 = \$46{,}175\). This is below the SS cap, so Social Security = \(46{,}175 \times 0.124 = \$5{,}725.70\) and Medicare = \(46{,}175 \times 0.029 = \$1{,}339.08\). Total SE tax = $7,064.78, and you can deduct half ($3,532.39) on your return.

FAQ

Do I pay SE tax if I have a small loss? No — if net earnings are zero or negative, there is no SE tax.

Why 92.35%? It approximates the employer-side deduction, so the self-employed are not taxed on the portion an employer would not be taxed on.

Is this my full tax bill? No. SE tax is in addition to federal and state income tax. This tool estimates only the SECA (Social Security + Medicare) component.