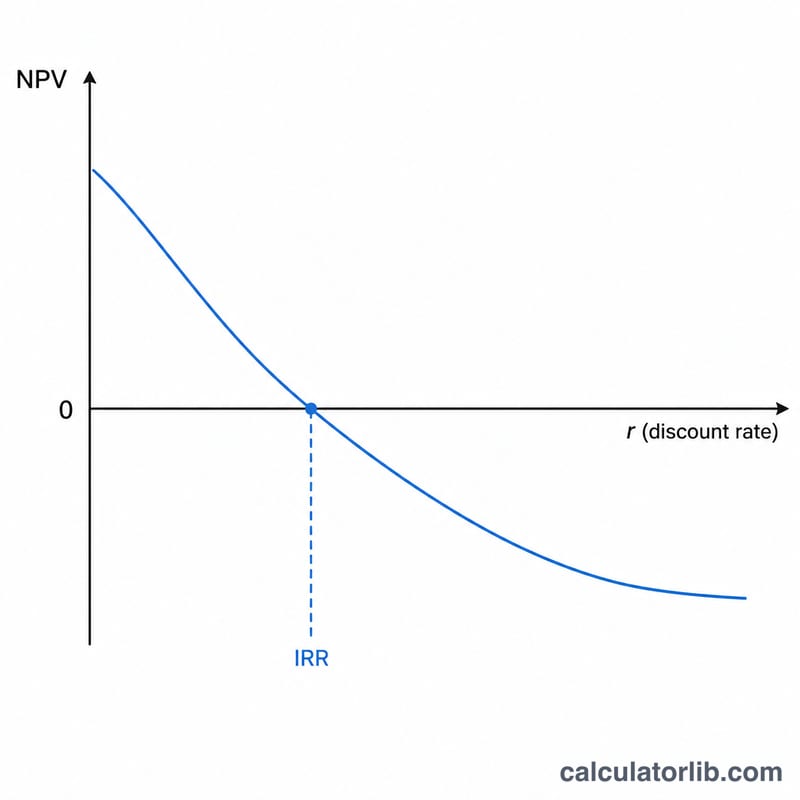

What is the NPV & IRR Calculator?

This tool evaluates the profitability of an investment or project. Net Present Value (NPV) discounts every future cash flow back to today's value using a chosen discount rate, then subtracts the initial investment. Internal Rate of Return (IRR) is the single discount rate at which the NPV becomes exactly zero — effectively the project's break-even annual yield.

How to use it

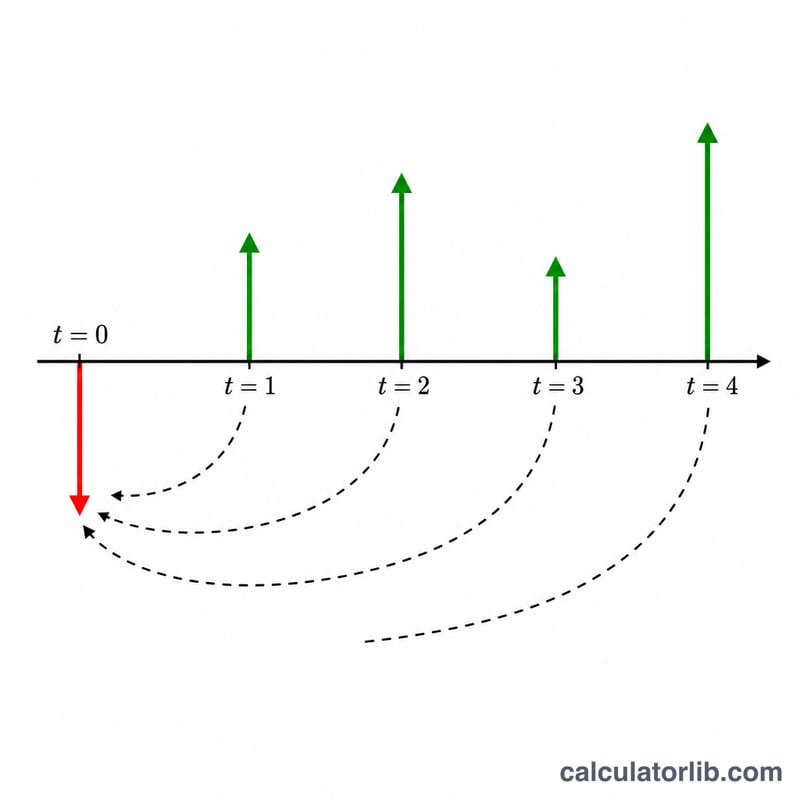

Enter the initial investment (the outflow at year 0), then list the cash inflows for each subsequent year separated by commas. Provide a discount rate to compute NPV. A positive NPV means the project adds value; an IRR above your required return (hurdle rate) means it is worth pursuing.

The formula explained

NPV sums each cash flow divided by (1 + r) raised to the power of the year. Year 0 is the negative initial investment. IRR has no closed-form solution, so the calculator uses bisection to find the rate that drives NPV to zero.

$$\text{NPV} = -\,\text{Initial} + \sum_{t=1}^{n} \frac{\text{CF}_t}{\left(1 + \dfrac{\text{Rate}}{100}\right)^{t}}$$$$0 = -\,\text{Initial} + \sum_{t=1}^{n} \frac{\text{CF}_t}{\left(1 + \text{IRR}\right)^{t}}$$

Worked example

Initial investment = 10,000; cash flows = 3,000, 4,200, 6,800; discount rate = 10%.

$$\text{NPV} = -10{,}000 + \frac{3{,}000}{1.1} + \frac{4{,}200}{1.1^2} + \frac{6{,}800}{1.1^3} = -10{,}000 + 2{,}727.27 + 3{,}471.07 + 5{,}109.69 \approx \mathbf{1{,}308.04}$$ Solving for IRR gives roughly 15.2%, comfortably above the 10% discount rate, so the project is financially attractive.

FAQ

What does a negative NPV mean? The project returns less than your discount rate — it destroys value at that required return.

Why might IRR be misleading? Projects with alternating positive and negative cash flows can have multiple IRRs, and IRR ignores the scale of investment, so always check NPV too.

What discount rate should I use? Typically your weighted average cost of capital (WACC) or required rate of return.