What is Net Present Value?

Net Present Value (NPV) measures how much a stream of future cash flows is worth today, after discounting each amount back to time 0 at a required rate of return. A positive NPV means the investment is expected to add value; a negative NPV means it destroys value at the chosen discount rate. This calculator supports uneven cash flows, intra-period compounding, and both beginning- and end-of-period timing.

How to use it

Enter the periodic discount rate as a percent (for example 4 for 4%). Set the compounding frequency per period (1 = compound once per period). Choose whether cash flows occur at the end (ordinary annuity) or beginning (annuity due) of each period. Set the time-0 outlay (usually negative). Then add one line per distinct cash-flow group: a "Periods" count and the "Cash Flows" amount that repeats in each of those consecutive periods. Lines expand into a flat per-period stream, so 5 periods at 50,000 fills periods 1-5.

The formula explained

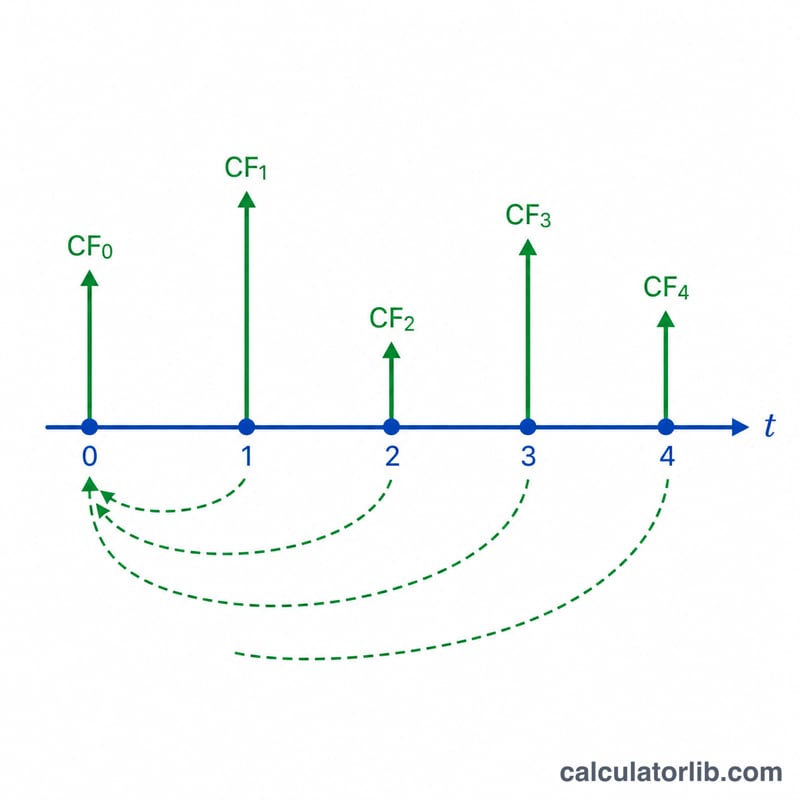

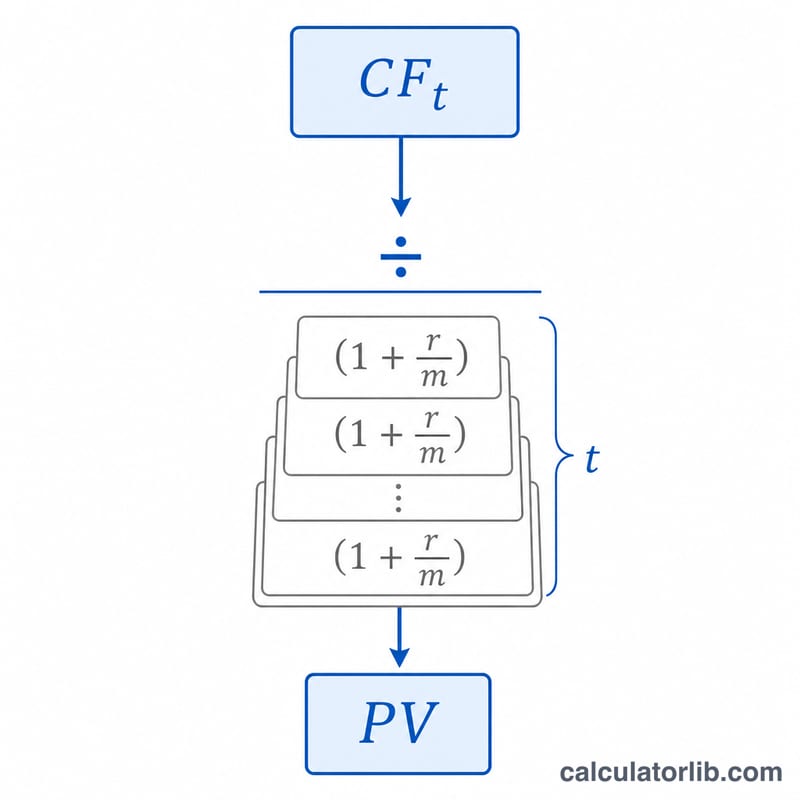

With periodic rate \(r\) (decimal) and \(m\) compounding sub-intervals, the end-of-period discount factor for period \(t\) is \(1 / \left(1 + r/m\right)^{m \cdot t}\). Multiply each period's cash flow by its factor and sum them, then add the undiscounted time-0 amount. If \(r = 0\), every factor is 1 and NPV is simply the sum of all cash flows. For beginning timing the exponent becomes \(m \cdot (t-1)\).

$$\text{NPV} = CF_0 + \sum_{t=1}^{N} \frac{CF_t}{\left(1 + \frac{r}{m}\right)^{m \cdot t}}$$

Worked example

Rate 4%, \(m = 1\), end timing. Time 0 = -200,000. Periods 1-5 = 50,000 each; periods 6-10 = 45,000 each. Each flow is divided by \(1.04^t\). Period 1 = $$50{,}000 / 1.04 = 48{,}076.92$$ period 6 = $$45{,}000 / 1.04^6 = 35{,}564.15$$ Summing all ten present values plus the -200,000 gives an NPV of about $187,249.42 over 10 periods.

FAQ

How is this different from Excel's NPV? Excel's NPV() discounts the first argument as period 1. Here, the time-0 line is never discounted (like adding it outside NPV), and you can group repeated amounts by a period count.

What discount rate should I use? Use your required rate of return or cost of capital per period. For annual periods, that is your annual rate.

Can cash flows be negative? Yes. Use negative values for outflows such as the initial investment or later capital expenditures.