What is the US Gift Tax Calculator?

This tool applies to United States federal gift tax only. It estimates how much (if any) federal gift tax a donor may owe after applying the annual gift exclusion and the unified lifetime exemption. Default values reflect the 2025 figures (annual exclusion $19,000 per recipient, lifetime exemption $13.99 million, top rate 40%); you can override them for other tax years or for prior-gift situations. This is an estimate, not tax advice — consult a CPA or the IRS for filing (Form 709).

How to use it

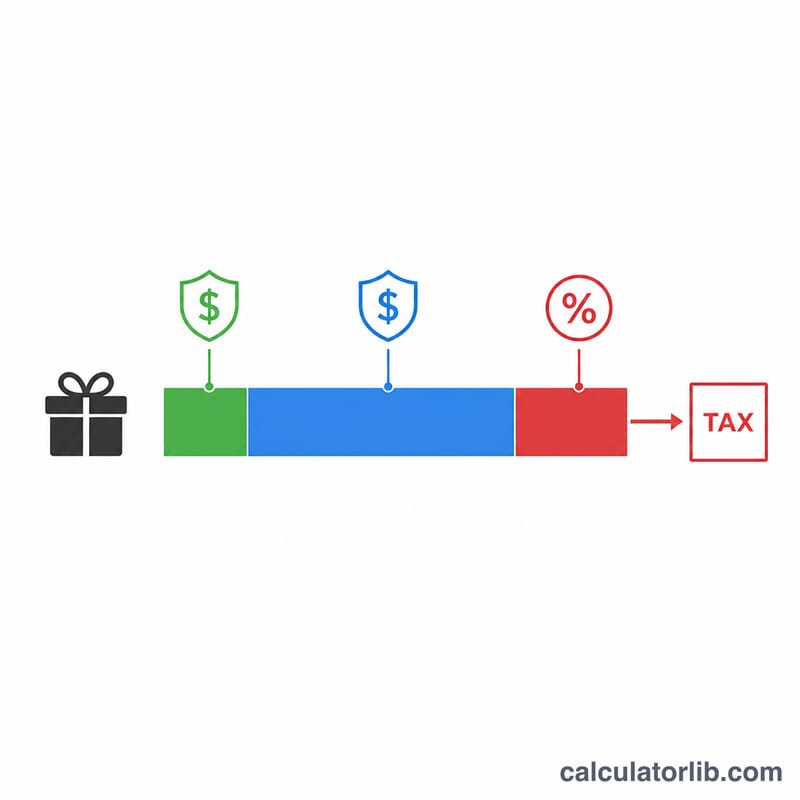

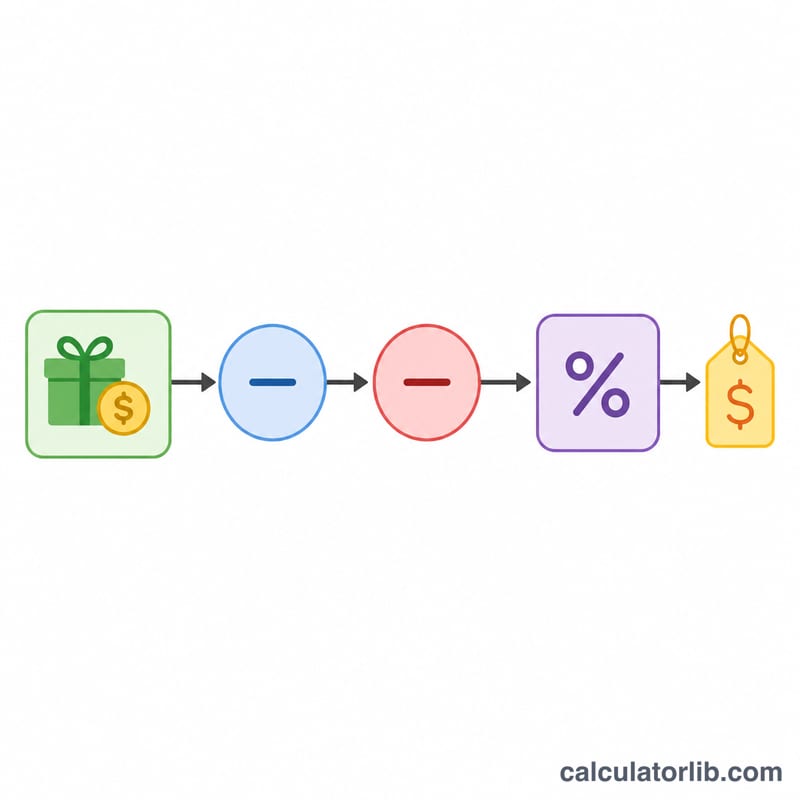

Enter the gift amount, the annual exclusion that applies to that recipient, any lifetime taxable gifts you have already made (which reduce your remaining exemption), the lifetime exemption amount, and the top tax rate. The calculator first subtracts the annual exclusion, then applies whatever lifetime exemption you have left, and only taxes anything beyond that.

The formula explained

First, the taxable gift equals the gift minus the annual exclusion (never below zero). Next, your remaining lifetime exemption equals the total exemption minus prior gifts already used. The smaller of the taxable gift and the remaining exemption is "applied" and shields that portion from tax. Whatever taxable gift is left is multiplied by the tax rate.

$$\begin{gathered} \text{Tax} = \max\!\left(T - E,\ 0\right) \times \dfrac{\text{Rate \%}}{100} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} T &= \max\!\left(\text{Gift} - \text{Annual Exclusion},\ 0\right) \\ E &= \min\!\left(T,\ \max\!\left(\text{Lifetime Exemption} - \text{Prior Gifts},\ 0\right)\right) \end{aligned} \right. \end{gathered}$$

Worked example

Suppose you give $50,000 to one person, the annual exclusion is $19,000, you have used $0 of a $13,990,000 lifetime exemption, and the rate is 40%. Taxable gift = \(\$50{,}000 - \$19{,}000 = \$31{,}000\). Because $31,000 is fully covered by the available exemption, the exemption applied is $31,000, the amount actually taxed is $0, and the tax due is $0 — though Form 709 is still typically required to report it.

$$\text{Tax} = \max\!\left(31{,}000 - 31{,}000,\ 0\right) \times \dfrac{40}{100} = 0$$

FAQ

Does the recipient pay the tax? No. US gift tax is generally the responsibility of the donor.

What is the annual exclusion? An amount you can give each recipient each year with no gift tax consequences and usually no need to report.

When is tax actually owed? Only after your cumulative taxable gifts exhaust your lifetime exemption; then gifts above it are taxed up to 40%.