What is the 401(k) Contribution Calculator?

This calculator is for US employees participating in an employer-sponsored 401(k) retirement plan. It estimates how much you and your employer will contribute each year and each paycheck based on your salary, the percentage you elect to defer, and your company's matching formula. Figures here are pre-tax estimates and use the 2024 IRS employee deferral limit of $23,000 ($30,500 if age 50+) as a reference cap.

How to use it

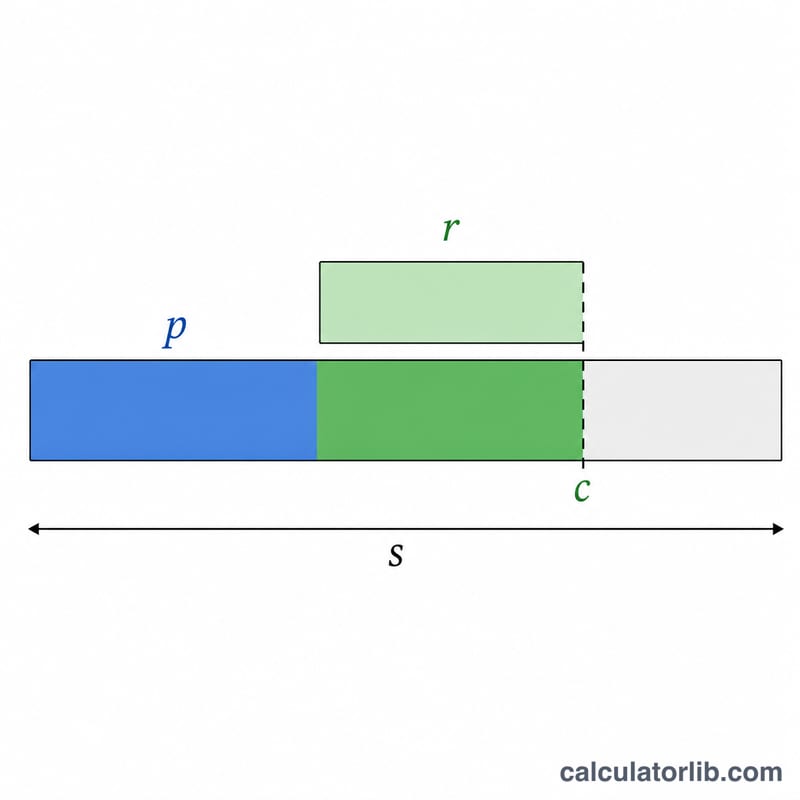

Enter your annual gross salary, the percentage of pay you want to contribute, your employer's match rate (e.g. 50% or 100% of your contribution), and the match cap (the maximum percent of salary your employer will match). Choose your pay frequency, then read off your annual and per-paycheck contribution amounts plus the "free money" from your employer.

The formula explained

Your annual employee contribution is simply Salary × ContribPct. The employer match only applies up to the cap, so the matched portion of your rate is min(ContribPct, MatchCap). Multiply that by the match rate and your salary: $$\text{EmployerMatch} = \min(\text{ContribPct}, \text{MatchCap})\times \text{MatchRate} \times \text{Salary}$$ The total annual contribution is the sum of the two, and per-paycheck values divide each by the number of pay periods.

Worked example

Salary $100,000, you contribute 10%, employer matches 50% up to 6% of salary, paid bi-weekly (26 periods). Employee contribution = \(\$100{,}000 \times 10\% = \$10{,}000\). Matched percent = \(\min(10\%, 6\%) = 6\%\), so employer match = \(6\% \times 50\% \times \$100{,}000 = \$3{,}000\). Total = $13,000/year. Per paycheck: you contribute $384.62 and your employer adds $115.38.

2024 & 2023 IRS 401(k) Contribution Limits

The IRS sets annual limits on how much you and your employer can contribute to a 401(k) plan. The two key figures are the employee elective deferral limit (what you can defer from your own paychecks) and the annual additions limit (the combined total of your deferrals plus all employer contributions). Employees age 50 and older can add a catch-up contribution on top of the standard limits.

| Limit | 2024 | 2023 |

|---|---|---|

| Employee elective deferral limit (under age 50) | $23,000 | $22,500 |

| Catch-up contribution (age 50+) | $7,500 | $7,500 |

| Employee deferral limit including catch-up (age 50+) | $30,500 | $30,000 |

| Combined employee + employer annual additions limit (under age 50) | $69,000 | $66,000 |

| Annual additions limit including catch-up (age 50+) | $76,500 | $73,500 |

Notes: The annual additions limit also caps out at 100% of your compensation if that is lower than the dollar figure. The employee deferral limit applies across all 401(k) and 403(b) plans you participate in during the year, not per employer. Employer matching and profit-sharing contributions count toward the combined annual additions limit but not toward your personal deferral limit.

Key Terms Explained

- Elective deferral

- The portion of your salary you voluntarily choose to redirect into your 401(k) instead of receiving it as current take-home pay. Deferrals are subject to the annual IRS employee contribution limit ($23,000 in 2024).

- Contribution percentage

- The share of your gross pay you elect to contribute each pay period, entered in this calculator as contribPct. For a $80,000 salary, a 6% contribution equals $4,800 of employee deferrals per year.

- Employer match rate

- How much your employer adds for every dollar you contribute, expressed as a percentage (matchRate). A common arrangement is a 50% match (the employer adds $0.50 per $1.00 you defer); a 100% match is a full dollar-for-dollar match.

- Match cap

- The maximum percentage of your salary that the employer will match (matchCap). If the cap is 6%, contributing more than 6% does not earn additional matching dollars — though your own deferrals still grow your balance. In this calculator the match is based on the lesser of your contribution % and the match cap.

- Pay frequency / pay periods

- How often you are paid in a year (payPeriods): 52 (weekly), 26 (biweekly), 24 (semi-monthly), or 12 (monthly). Annual contributions are divided across these periods to show the per-paycheck amount.

- Traditional vs. Roth 401(k)

- Traditional 401(k) contributions are made pre-tax, lowering your taxable income now, with withdrawals taxed in retirement. Roth 401(k) contributions are made after tax, so qualified withdrawals (including growth) are tax-free later. Both share the same combined elective deferral limit.

- Vesting

- The schedule that determines how much of the employer's matching contributions you actually own if you leave the company. Your own deferrals are always 100% vested immediately; employer contributions may vest gradually (graded) or all at once after a set period (cliff).

FAQ

Does this include the IRS contribution limit? The calculator flags the 2024 limit but does not hard-cap your input — verify your elected amount stays within the legal maximum.

Is the match really free money? Yes. Contributing at least up to the match cap captures your full employer match, which is an immediate return on your savings.

Are these amounts pre-tax? For a traditional 401(k), yes — contributions reduce taxable income. Roth 401(k) contributions are after-tax instead.