What this calculator does

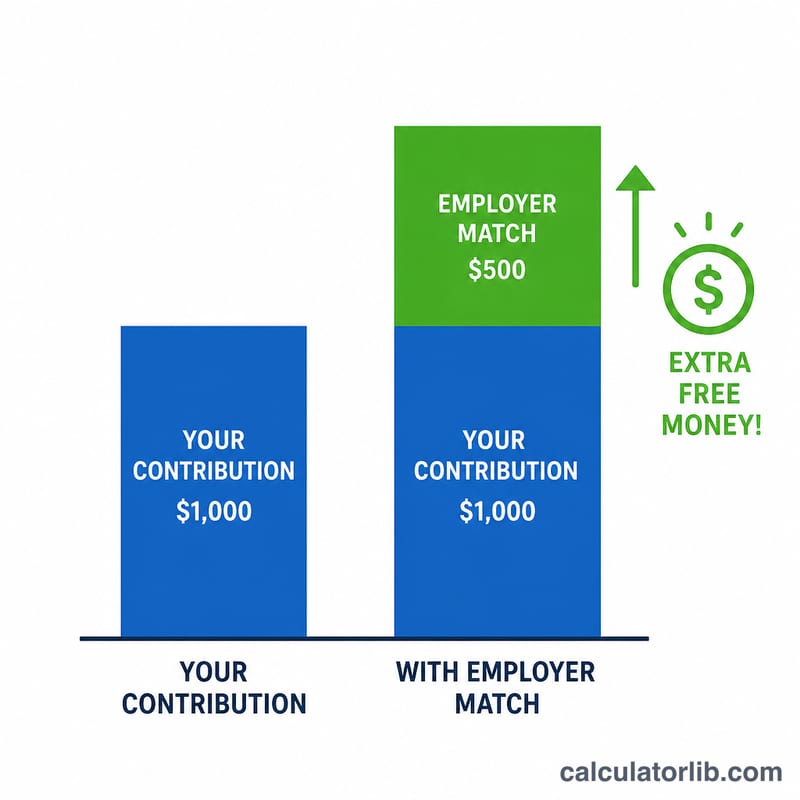

This tool applies to United States 401(k) retirement plans. Many US employers match part of what you put into your 401(k) — effectively free money toward your retirement. This calculator shows how much employer match you earn each year based on your salary, how much you contribute, your employer's match rate, and the cap on how much salary the match applies to.

How to use it

Enter your gross annual salary, the percentage of salary you contribute, your employer's match rate (e.g. 50% means 50 cents per dollar), and the match cap (the maximum percent of salary the employer will match). The calculator returns your annual employer match, your own contribution, the combined total, and the percent of salary that actually got matched.

The formula explained

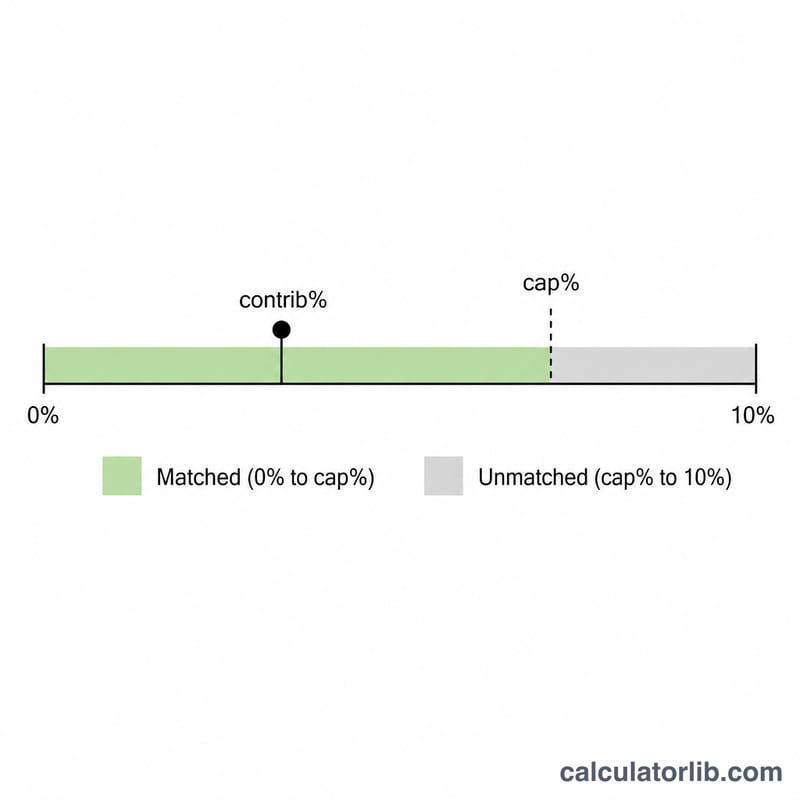

The match only applies up to the cap, so we first take min(your contribution %, cap %). We multiply that matched percent by the match rate and by your salary:

$$\text{Annual Match} = \frac{\min\!\left(\text{contrib \%},\ \text{cap \%}\right)}{100} \times \frac{\text{match Rate \%}}{100} \times \text{salary}$$

Contributing more than the cap does not increase the match — you simply max out the free money at the cap.

Worked example

Salary $60,000, you contribute 6%, employer matches 50% up to a 6% cap. Matched percent = \(\min(6\%,\ 6\%) = 6\%\). Match = $$0.06 \times 0.50 \times 60{,}000 = \$1{,}800$$ Your own contribution = \(0.06 \times 60{,}000 = \$3{,}600\), so $5,400 total goes into your 401(k).

FAQ

Should I always contribute at least up to the cap? Generally yes — contributing below the cap leaves free employer money on the table.

What is a typical match? A common formula is 50% of contributions up to 6% of salary, but 100% up to 3–5% is also common. Check your plan documents.

Does the employer match count toward my contribution limit? No. Employer contributions do not count against your personal IRS elective-deferral limit, though combined limits apply.