What Is the Interest Earned Calculator?

This calculator shows how much interest a savings deposit or investment will earn over time using compound interest. You provide your initial deposit, the annual interest rate, how long you keep the money invested, and how often interest is compounded. The tool then separates the total interest you earn from your original principal, so you can clearly see the growth your money generates.

How to Use It

Enter your initial deposit (the principal), the annual interest rate as a percentage, and the time in years. Then choose how often interest is compounded — annually, semi-annually, quarterly, monthly, or daily. More frequent compounding produces slightly more interest because earned interest starts earning interest sooner.

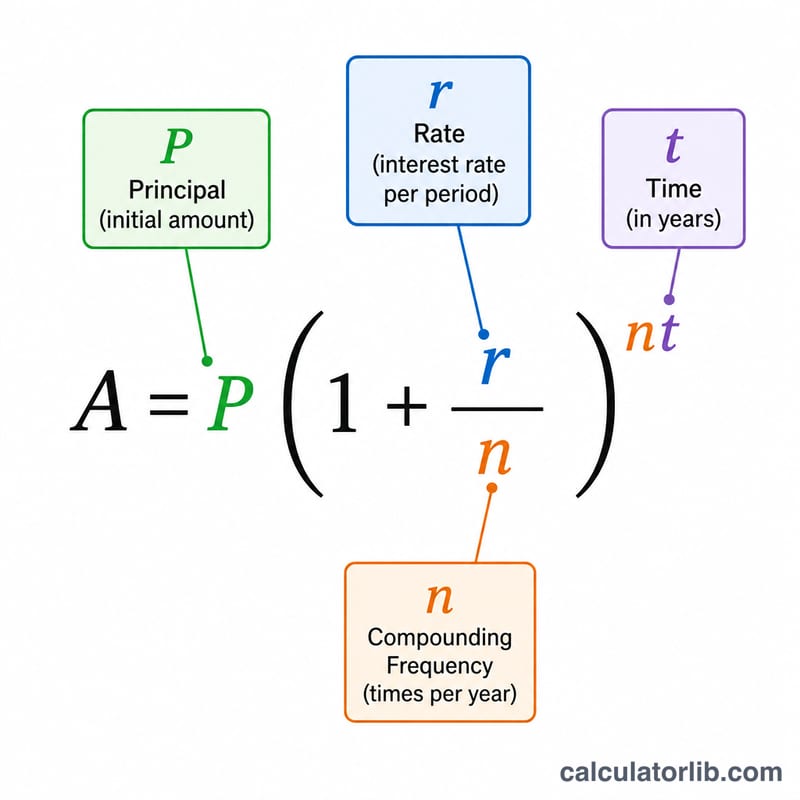

The Formula Explained

The calculator uses the standard compound interest formula: $$I = P\left(1 + \frac{r}{n}\right)^{n\,t} - P$$ Here P is the principal, r is the annual rate as a decimal (\(5\% = 0.05\)), n is the number of compounding periods per year, and t is the number of years. The term \(P\left(1 + \frac{r}{n}\right)^{n\,t}\) gives the future value (full balance), and subtracting the principal leaves the interest earned alone.

Worked Example

Suppose you deposit $10,000 at a 5% annual rate, compounded monthly, for 10 years. Then \(n = 12\) and \(t = 10\), so the balance is $$10{,}000 \times \left(1 + \frac{0.05}{12}\right)^{120} \approx \$16{,}470.09$$ Subtracting the $10,000 principal leaves about $6,470.09 in interest earned.

FAQ

Does this include taxes? No. The result is gross interest before any taxes that may apply in your country.

What if I add money regularly? This calculator assumes a single lump-sum deposit with no further contributions or withdrawals.

Why does compounding frequency matter? The more often interest compounds, the sooner it begins earning its own interest, slightly increasing the total — daily compounding earns a bit more than annual at the same rate.