What Is a FIRE Number?

Your FIRE (Financial Independence, Retire Early) number is the size of investment portfolio you need so that its returns — withdrawn at a sustainable rate — can cover your living expenses indefinitely. Reaching it means work becomes optional. The concept is rooted in the popular "4% rule," derived from the Trinity Study, which suggests that withdrawing about 4% of a portfolio in the first year (then adjusting for inflation) has historically lasted 30+ years.

How to Use This Calculator

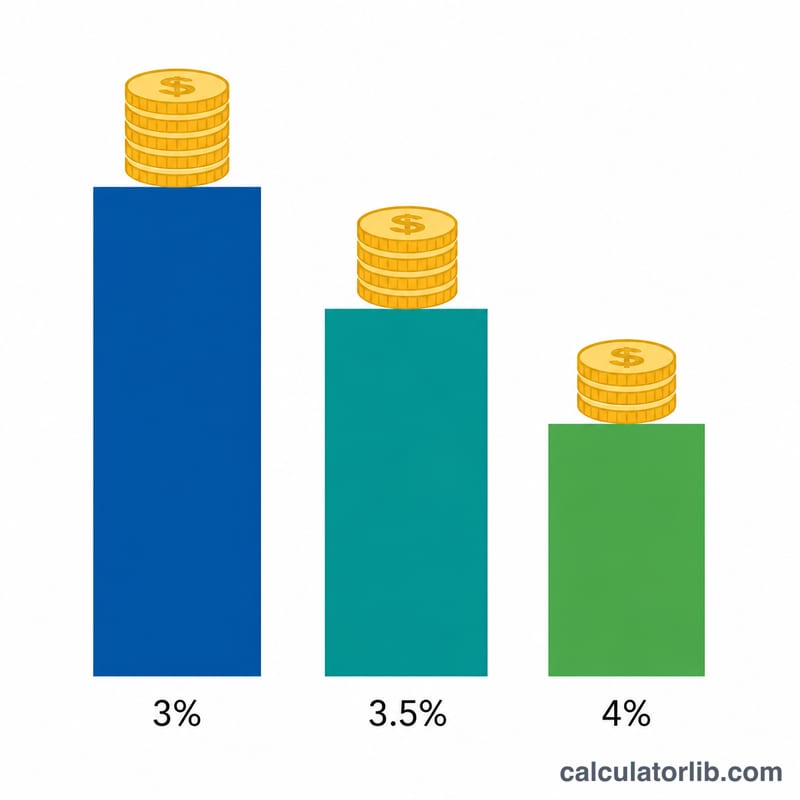

Enter your expected annual expenses in retirement, the safe withdrawal rate you plan to use (4% is the classic default; more conservative savers use 3–3.5%), and optionally your current savings. The calculator returns your target portfolio, how much you still need, and your progress percentage.

The Formula Explained

The math is simple: divide your annual spending by your withdrawal rate expressed as a decimal.

$$\text{FIRE Number} = \dfrac{\text{Annual Expenses}}{\text{Withdrawal Rate} / 100}$$At a 4% withdrawal rate this is the same as multiplying expenses by 25 (because \(1 \div 0.04 = 25\)). A lower withdrawal rate means a larger, safer target; a higher rate means a smaller target but more sequence-of-returns risk.

Worked Example

Suppose you spend $40,000 per year and use a 4% withdrawal rate. Your FIRE number is

$$40{,}000 \div 0.04 = \$1{,}000{,}000$$If you've already saved $250,000, you still need $750,000 and are 25% of the way there.

FAQ

Is the 4% rule guaranteed? No. It's a historical guideline based on US market data. Market conditions, longer retirements, and fees can change outcomes — many in the FIRE community prefer 3.25–3.5% for extra safety.

Should I include taxes? Yes. Your annual expenses figure should reflect what you actually need to spend, including estimated taxes on withdrawals and healthcare costs.

What about inflation? The withdrawal-rate approach already assumes inflation-adjusted withdrawals, so use today's expense figures and the rule accounts for rising costs over time.