What is present value?

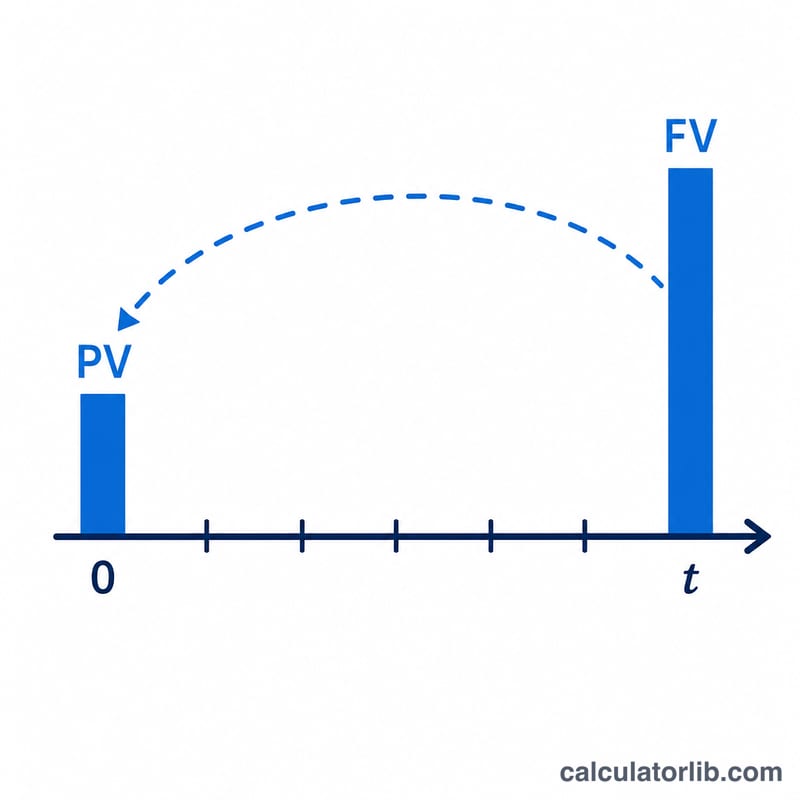

Present value (PV) is what a future amount of money is worth today, once you discount it at a given interest or required rate of return. A dollar received in the future is worth less than a dollar today, because today's dollar can be invested and grow. This calculator finds the PV of a single future lump sum (FV) and, optionally, the PV of a recurring payment stream — an ordinary annuity, an annuity due, a growing annuity, or a perpetuity. It is universal time-value-of-money math with no regional or tax rules.

How to use it

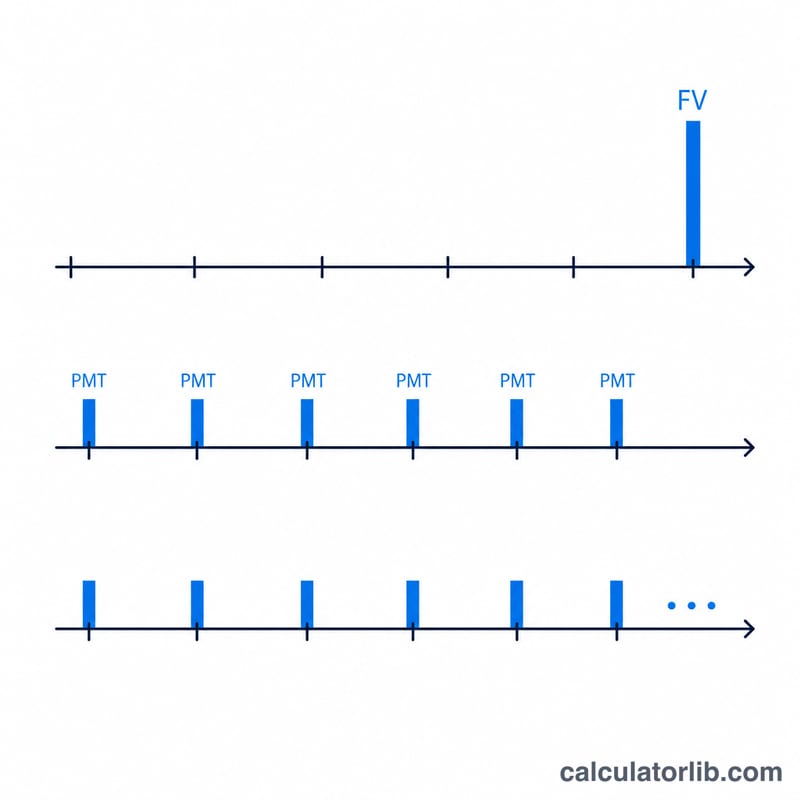

Enter the Future Value, the Number of Periods (t), the Rate per period, and the Compounding intervals per period (m). Leave the payment fields blank to value only the lump sum. To value a payment stream, enter the Amount (PMT), optional growth, payments per period (q), and whether payments occur at the end (ordinary) or start (due). For a perpetuity, type p in the Number of Periods box; for continuous compounding, type C in the Compounding box.

The formula explained

The lump sum is discounted as $$\text{PV} = \dfrac{\text{FV}}{\left(1+\frac{R}{m}\right)^{m t}}.$$ The periodic effective rate is \(i = (1 + R/m)^m - 1\), and the per-payment rate is \(i_{pay} = (1 + i)^{1/q} - 1\) over \(N = q\cdot t\) payments. An ordinary annuity is $$\text{PV} = \text{PMT}\cdot\dfrac{1-(1+i_{pay})^{-N}}{i_{pay}};$$ an annuity due multiplies that by \((1 + i_{pay})\). Deposits subtract the stream's PV (reducing the amount you must set aside), while withdrawals add it.

Worked example

FV = 15,000, t = 10, R = 5.25%, m = 12, no payments. $$\text{PV} = \frac{15{,}000}{(1 + 0.0525/12)^{120}} = \frac{15{,}000}{1.68856} = \textbf{\$8{,}883.50}.$$

FAQ

Why is the rate "per period"? The rate you enter applies to one period; compounding m sets how often interest is applied within that period.

What does typing "p" do? It models a perpetuity — payments forever — so the lump-sum term vanishes and \(\text{PV} = \text{PMT} / i_{pay}\) (or \(\text{PMT} / (i_{pay} - g)\) for a growing perpetuity).

Deposits vs withdrawals? Withdrawals add the stream's PV to the lump-sum PV; deposits subtract it, since regular contributions reduce the amount you need today.