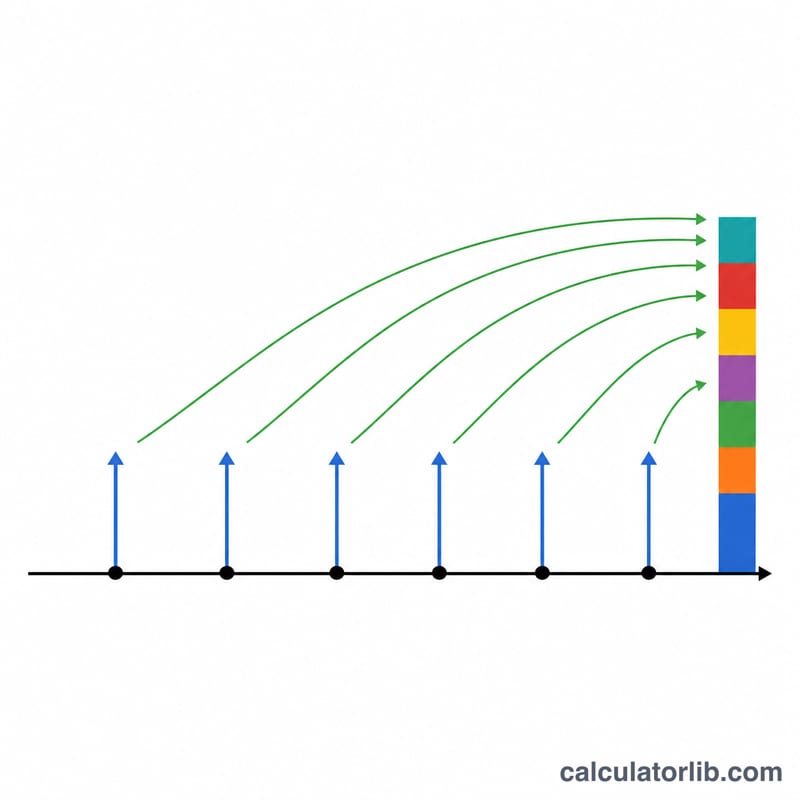

What Is the Future Value of an Annuity?

An annuity is a series of equal payments made at regular intervals — such as monthly savings deposits, retirement contributions, or loan installments. The future value of an annuity tells you how much that stream of payments will be worth at a chosen point in the future, after each payment has had a chance to earn compound interest. This calculator works for any currency since it is pure mathematics.

How to Use This Calculator

Enter your payment per period (PMT), the interest rate earned each period, and the total number of periods. Choose whether the annuity is ordinary (payments at the end of each period, the most common case) or an annuity due (payments at the start of each period). The calculator returns the accumulated future value, your total contributions, and the interest earned.

Make sure your rate and number of periods use the same time unit. For monthly deposits, use the monthly rate (annual rate ÷ 12) and the total number of months.

The Formula Explained

The standard formula is:

$$FV = PMT \times \frac{(1 + r)^n - 1}{r}$$

Here \(r\) is the periodic interest rate as a decimal (e.g. 5% = 0.05) and \(n\) is the number of payments. For an annuity due, the entire result is multiplied by \((1 + r)\) because every payment compounds for one additional period.

Worked Example

Suppose you deposit $1,000 at the end of each year for 10 years into an account earning 5% annually. With \(r = 0.05\) and \(n = 10\):

$$FV = 1000 \times \frac{(1.05)^{10} - 1}{0.05} = 1000 \times \frac{1.628894627 - 1}{0.05} \approx \$12{,}577.89$$ You contributed $10,000, so the interest earned is about $2,577.89.

FAQ

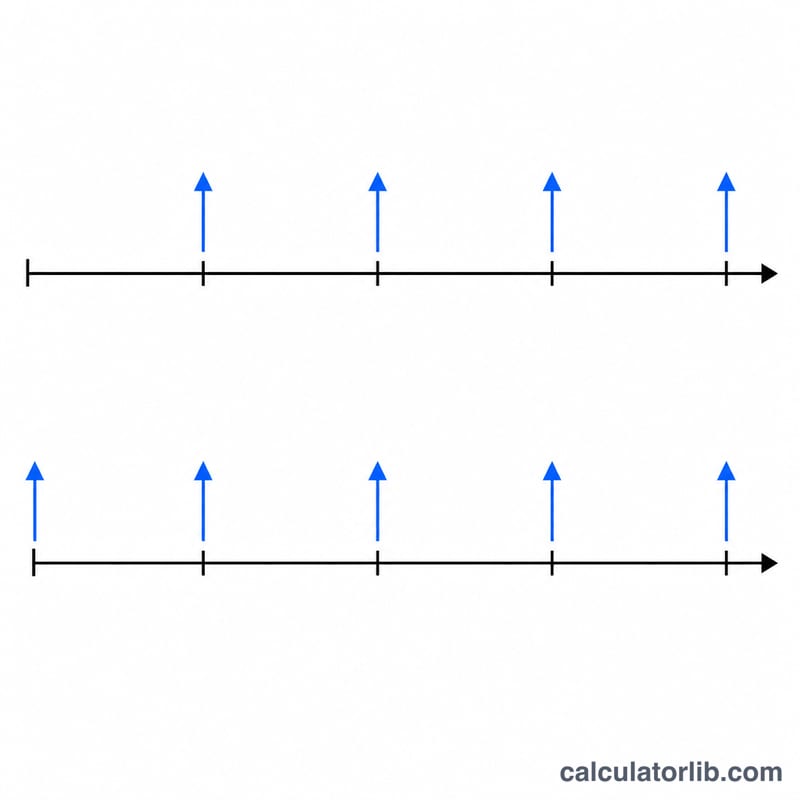

What is the difference between an ordinary annuity and an annuity due? In an ordinary annuity, payments occur at the end of each period; in an annuity due, they occur at the beginning, giving each payment an extra compounding period and a higher future value.

What if the interest rate is 0%? With no interest, the future value is simply the payment multiplied by the number of periods (\(PMT \times n\)).

How do I model monthly contributions? Convert the annual rate to a monthly rate (divide by 12) and set n to the total number of months.