What is the annuity future value factor?

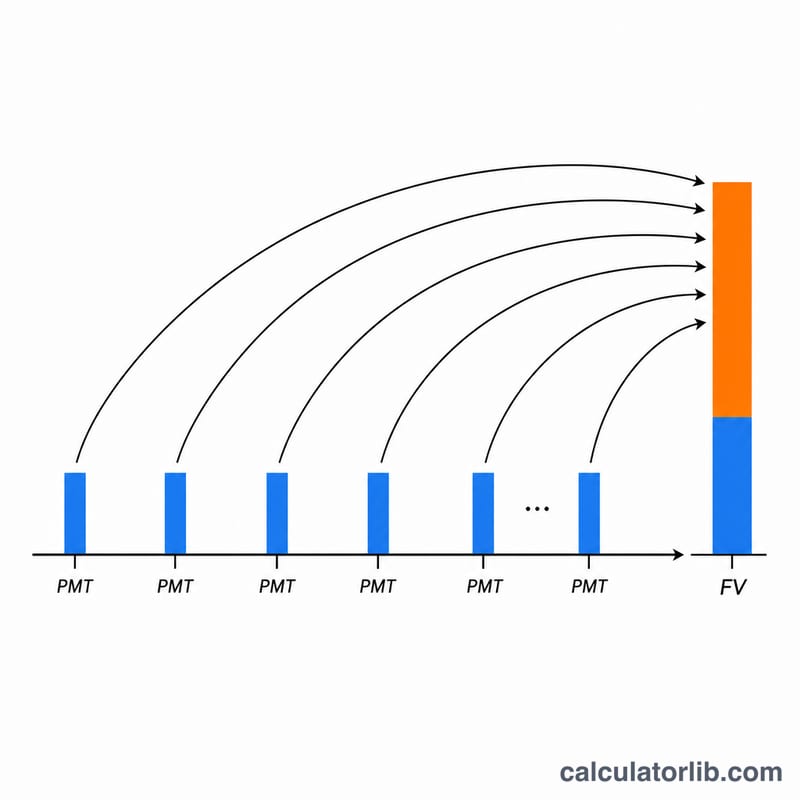

The annuity future value factor (sometimes called the savings accumulation factor) tells you how much a series of equal, regular contributions will grow to when each contribution earns compound interest. Multiply the factor by your fixed yearly contribution and you get the total accumulated value at the end of the saving period — original contributions plus all the interest they have earned. This is universal finance math; it works with any currency and any unit.

How to use this calculator

Enter four things: the fixed amount you contribute each year, the annual interest rate as a percent, the number of saving years, and how you want the result rounded (decimal places and rounding mode). The calculator assumes an ordinary annuity, meaning each contribution is made at the end of the year. It returns both the unitless factor and the future value in the same unit as your contribution.

The formula explained

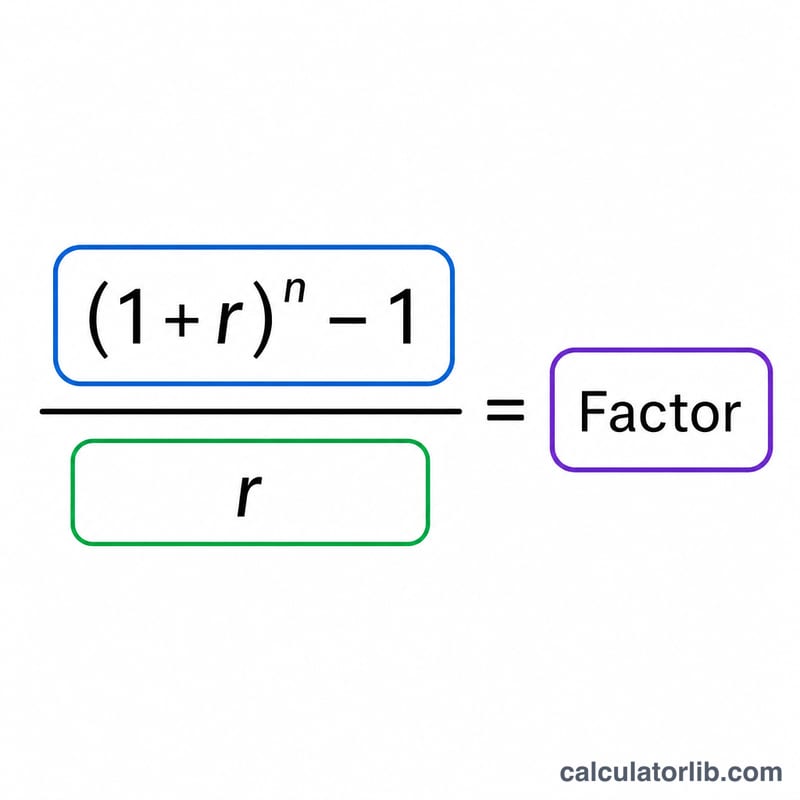

The factor is $$\frac{(1 + r)^{n} - 1}{r}$$ where \(r\) is the rate as a decimal (3% becomes 0.03) and \(n\) is the number of years. The future value is simply $$FV = \text{PMT} \times \text{factor}$$ If the rate is exactly 0%, dividing by \(r\) is undefined, so the calculator uses the correct limit: with no interest the factor equals \(n\) (you just sum the contributions).

Worked example

Suppose you save 1 unit per year for 20 years at 3%. Then \(r = 0.03\) and \((1.03)^{20} = 1.806111\). The factor is $$\frac{1.806111 - 1}{0.03} = 26.870 \text{ (3 decimals)}$$ Future value $$= 1 \times 26.870 = 26.870$$ If each unit were 10,000 of currency, that is roughly 268,703 accumulated from contributing 10,000 per year for 20 years.

FAQ

Is this an ordinary annuity or annuity-due? Ordinary — contributions occur at the end of each period. For an annuity-due (start-of-period), multiply the result by \((1 + r)\).

What if the rate is 0%? The factor becomes equal to the number of years and the future value is just contribution × years.

What unit is the future value in? The same unit as the contribution you entered — the factor itself is unitless, so no conversion is applied.