What Is Present Value?

Present value (PV) answers a simple but powerful question: how much money do you need to deposit today, in a single lump sum, so that it grows into a specific target amount in the future? Because money earns interest over time, a dollar today is worth more than a dollar tomorrow. This calculator "discounts" your future goal back to its equivalent value right now.

How to Use It

Enter your Future Value Goal (the amount you want to have), the annual interest rate you expect to earn, the number of years until you need the money, and how often interest compounds (monthly, quarterly, annually, etc.). The result is the deposit you must make today, plus the interest that deposit will earn along the way.

The Formula Explained

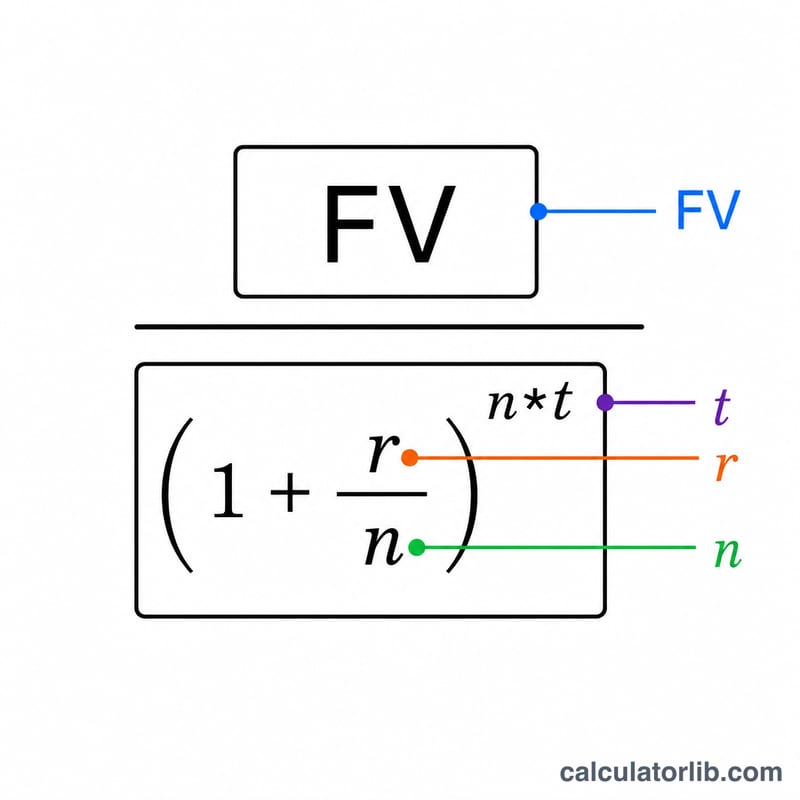

The present value formula is $$PV = \dfrac{FV}{\left(1 + r/n\right)^{n \cdot t}}$$ where FV is the future value, r is the annual rate as a decimal, n is the number of compounding periods per year, and t is the number of years. The denominator is the compound growth factor; dividing the goal by it reverses the growth to find today's value.

Worked Example

Suppose you want $10,000 in 10 years and expect 5% interest compounded monthly. Here \(r = 0.05\), \(n = 12\), \(t = 10\). The growth factor is $$\left(1 + 0.05/12\right)^{120} \approx 1.6470$$ So $$PV = 10{,}000 / 1.6470 \approx \$6{,}071.63$$ Deposit that today and it grows to your $10,000 goal, earning about $3,928 in interest.

FAQ

Does compounding frequency matter? Yes. More frequent compounding means a slightly higher growth factor, so you need a slightly smaller deposit today to reach the same goal.

What rate should I use? Use the realistic annual yield (APY's underlying nominal rate) of the account or investment you plan to use. Conservative estimates avoid disappointment.

Is this the same as discounting cash flows? This computes the present value of a single future lump sum. Streams of regular payments use an annuity present value formula instead.