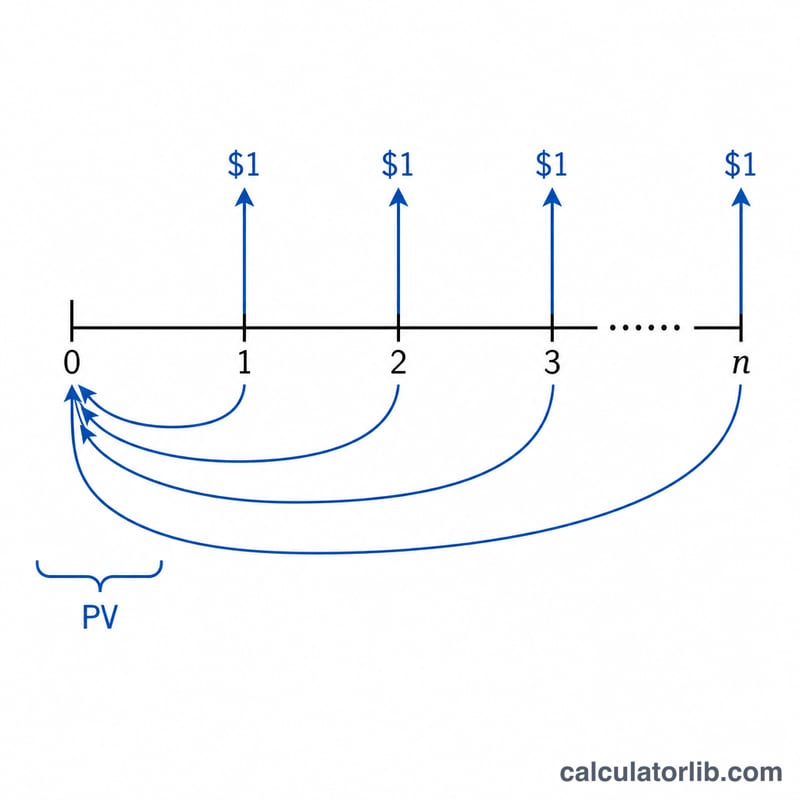

What is a PVIFA Table?

A PVIFA (Present Value Interest Factor for an Annuity) table shows the present value today of receiving $1 at the end — or beginning — of each period for n periods, discounted at a periodic interest rate i. Multiply any annuity payment by the matching factor and you instantly get its present value. This creator lets you build a custom grid: rows are the number of periods, columns are interest rates, and you control the starting values and increments for each.

How to Use It

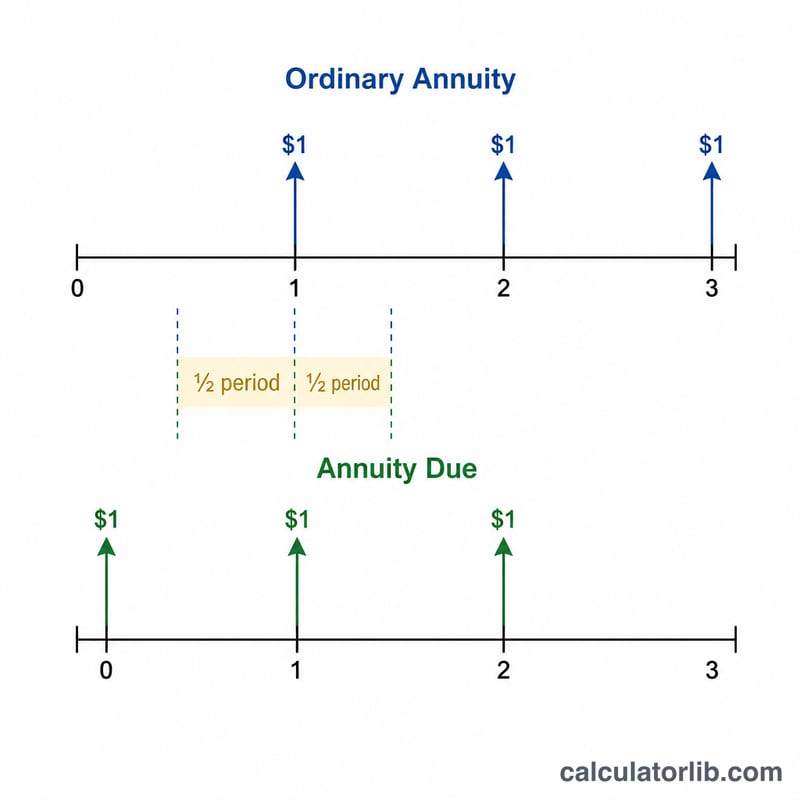

Pick the annuity type (ordinary = payment at period end, or annuity due = payment at the start). Set how many rate columns you want, the starting rate, and the rate increment added to each successive column. Then set how many period rows you want, the starting period count, and the period increment. The tool computes a factor for every cell and rounds it to 5 decimal places. Use the Print Table button for a clean printable copy.

The Formula Explained

For an ordinary annuity the factor is $$\text{PVIFA} = \frac{1}{i}\left[1 - (1+i)^{-n}\right]$$ where i is the per-period rate as a decimal (a 1% column means \(i = 0.01\)) and n is the number of periods. For an annuity due the payments arrive one period earlier, so each factor is multiplied by \((1+i)\). When the rate is exactly 0% the formula's limit is simply n, which the calculator handles automatically.

Worked Example

For n = 1 and i = 0.01 (1%): $$\frac{1}{0.01} \times \left(1 - \frac{1}{1.01}\right) = 100 \times (1 - 0.990099) = 0.99010$$ For n = 2 at 1%: $$100 \times \left(1 - \frac{1}{1.0201}\right) = 1.97040$$ For n = 3 at 3%: $$33.3333 \times \left(1 - \frac{1}{1.03^3}\right) = 2.82861$$ A one-period annuity due at 1% equals \(0.99010 \times 1.01 = 1.00000\) — exactly $1, because the single payment is received immediately.

FAQ

How do I use a factor? Multiply your level payment by the factor: a $500 payment for 10 periods at 5% with a factor of 7.72173 has a present value of $3,860.87.

Why divide the percent by 100? The formula needs i as a decimal, so 5% becomes 0.05. The table headers display the percent for readability.

Ordinary vs annuity due? Ordinary annuities pay at the end of each period (typical for loans and bonds); annuity due pays at the start (typical for rent or leases), making each factor slightly larger by a factor of \((1+i)\).