What is the FVIFA Table Creator?

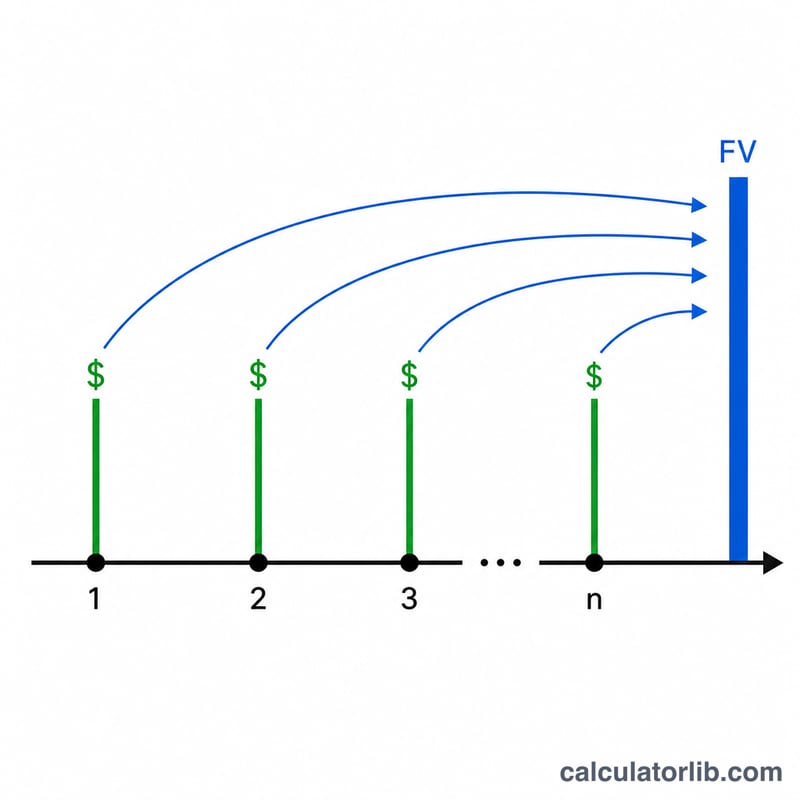

This tool builds a Future Value Interest Factor of an Annuity (FVIFA) table. Each factor tells you the future value of a stream of $1 payments made every period, accumulated at a given periodic interest rate. Multiply any factor by your actual payment amount to get the future value of that annuity. The table is indexed by the number of periods (\(n\), the rows) and the periodic interest rate (\(i\), the columns).

How to use it

Choose the annuity type, then set how many interest-rate columns you want, the starting rate and the increment between columns. Set how many period rows you want, the starting period, and the increment between rows. The tool generates a labeled grid of factors rounded to five decimal places, ready to read or print.

The formula explained

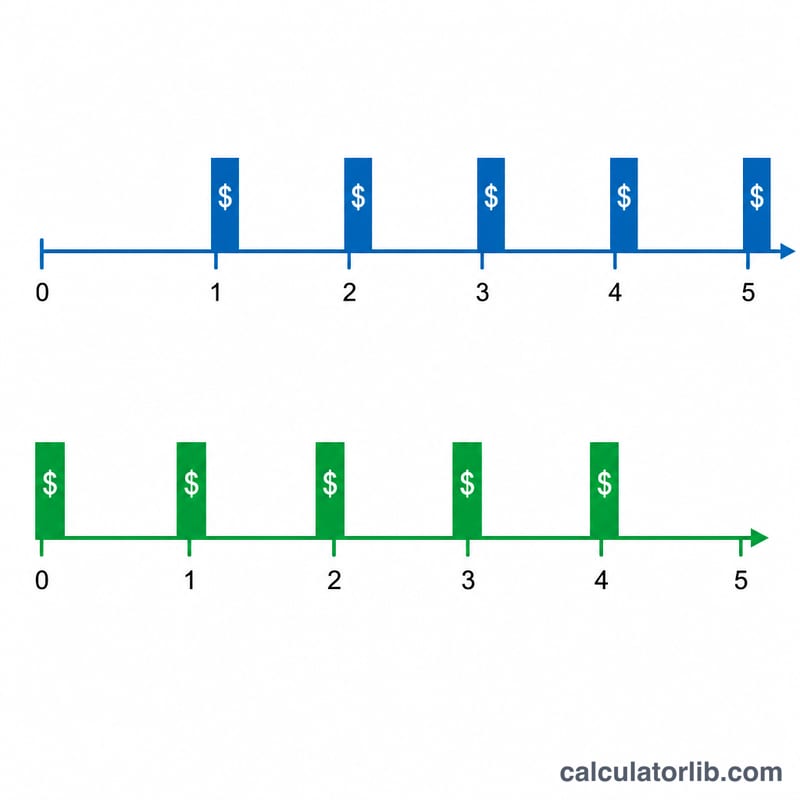

For an ordinary annuity (payments at the end of each period) the factor is $$\text{FVIFA} = \frac{(1+i)^n - 1}{i}$$ For an annuity due (payments at the beginning of each period) each payment earns one extra period of interest, so the factor is multiplied by \((1+i)\): $$\text{FVIFA} = \frac{(1+i)^n - 1}{i}\,(1+i)$$ When the rate \(i\) is exactly 0, the formula would divide by zero; the mathematical limit is simply \(n\), so a 0% column shows the factor \(n\).

Worked example

Ordinary annuity, \(i = 1\%\) (0.01), \(n = 3\): $$\frac{(1.01)^3 - 1}{0.01} = \frac{1.030301 - 1}{0.01} = 3.03010$$ At \(i = 3\%\), \(n = 4\): $$\frac{(1.03)^4 - 1}{0.03} = \frac{0.12550881}{0.03} = 4.18363$$ For an annuity due with \(i = 1\%\), \(n = 2\): $$2.01000 \times 1.01 = 2.03010$$

FAQ

What does a single factor mean? It is the future value of $1 paid each period. Multiply by your payment size to get the total.

Ordinary vs. due? Ordinary pays at period end; due pays at the start, so it accumulates slightly more (by a factor of \(1 + i\)).

Why five decimals? Classic finance tables use five-decimal factors so they can be multiplied by large payments with minimal rounding error.