What is the Annuity Payment on a $1 Loan Table?

This tool builds a printable factor table showing the periodic payment required to fully amortize a loan of exactly $1, across a grid of interest rates (the columns) and numbers of periods (the rows). Each cell is a dimensionless payment factor: the dollars of payment, per dollar borrowed, per period. Because it is built on a $1 present value, the table is universal and applies to any currency or loan size — simply multiply a cell by your actual principal to get your actual periodic payment.

How to use it

Choose how many rate columns and period rows you want. Set the Starting Rate and the rate Increment to control the column headers (each column adds the increment to the previous rate). Set the Starting Period and period Increment to control the row headers. The generated table then lists the payment factor for every rate/period combination. To find your payment, locate the cell at your per-period interest rate and your number of payments, then compute: actual payment = principal × factor.

The formula explained

For a present value PV = $1, periodic interest rate i (in decimal) and n periods, the ordinary-annuity (end-of-period) amortizing payment is:

$$\text{PMT} = i \cdot \dfrac{(1+i)^n}{(1+i)^n - 1}$$

The interest rate per period is converted from percent with \(i = \text{rate\%} / 100\). The denominator equals zero only when \(i = 0\) or \(n = 0\), so both are excluded — all six inputs must be strictly positive. A period count of \(n = 1\) is valid and simply gives a factor of \(1 + i\).

Worked example

Take a rate of 2% per period (\(i = 0.02\)) over \(n = 10\) periods. Then \((1.02)^{10} = 1.21899442\), so the factor is $$0.02 \times \frac{1.21899442}{0.21899442} = 0.11132653.$$ Each $1 borrowed therefore requires about $0.1113 per period; for a $1,000 loan that is \(1000 \times 0.11132653 \approx \$111.33\) per period.

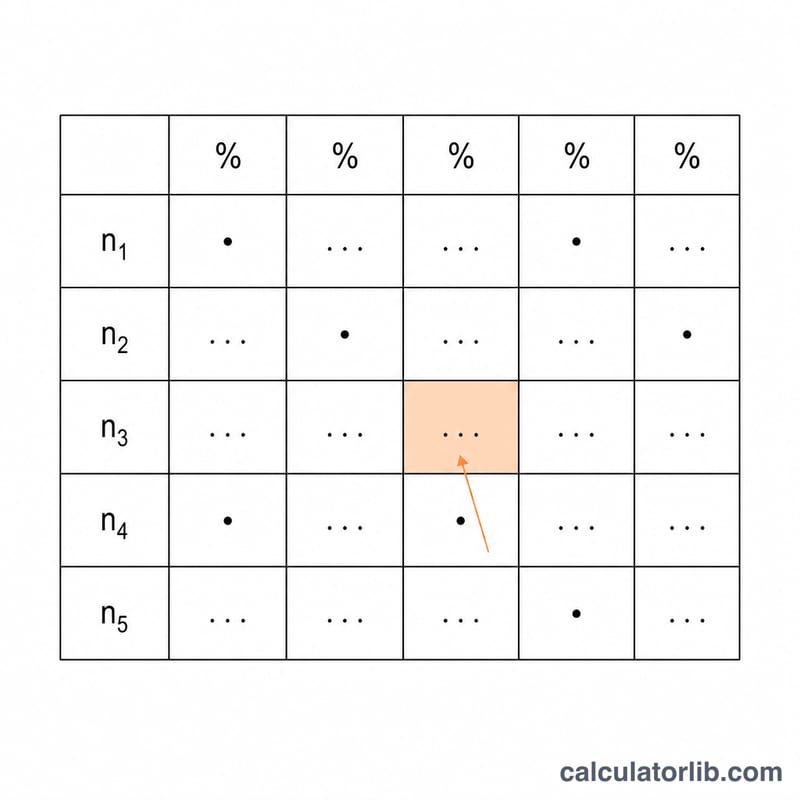

Sample Annuity Payment Factor Table

Each cell is the per-period payment required to fully amortize a $1 loan over \(n\) periods at a per-period interest rate \(i\), using the annuity payment formula:

$$\text{PMT} = i \cdot \frac{(1+i)^n}{(1+i)^n - 1}$$To find a real payment, multiply the factor by your principal. For example, a $20,000 loan over 60 periods at 0.5% per period is \(20000 \times 0.01933280 = \$386.66\) per period.

| Periods (n) | 0.25% | 0.50% | 1.00% | 1.50% | 2.00% |

|---|---|---|---|---|---|

| 12 | 0.08469370 | 0.08606643 | 0.08884879 | 0.09167999 | 0.09455960 |

| 24 | 0.04298121 | 0.04432061 | 0.04707347 | 0.04992410 | 0.05287110 |

| 36 | 0.02907515 | 0.03042194 | 0.03321431 | 0.03615240 | 0.03923285 |

| 60 | 0.01797498 | 0.01933280 | 0.02224445 | 0.02538932 | 0.02876797 |

| 120 | 0.00967604 | 0.01110205 | 0.01434709 | 0.01801852 | 0.02204993 |

| 180 | 0.00691558 | 0.00843857 | 0.01200172 | 0.01615215 | 0.02076485 |

| 360 | 0.00421604 | 0.00599551 | 0.01028613 | 0.01520176 | 0.02016531 |

Values shown to 8 decimal places. The factor falls as \(n\) grows (payments spread over more periods) and rises as \(i\) grows (more interest per period). As \(n\to\infty\) the factor approaches \(i\), since an infinitely long loan is effectively interest-only.

Key Terms & Variables

- Payment factor

- The level periodic payment that fully repays a $1 loan over \(n\) periods at rate \(i\). Multiply it by any principal to get that loan's payment. It is the reciprocal of the present-value annuity factor (PVIFA).

- Present value (PV)

- The amount borrowed today — the principal. In a $1 table, PV = 1, so each cell is a payment per dollar of present value.

- Periodic interest rate (i)

- The interest rate applied each period, expressed as a decimal. It equals the annual nominal rate divided by the number of compounding periods per year (e.g. 6% annual / 12 = 0.005 monthly).

- Number of periods (n)

- The total count of payment periods over the life of the loan — for a 30-year monthly mortgage, \(n = 30 \times 12 = 360\).

- PMT

- The constant payment made each period. For a general principal: \(\text{PMT} = \text{PV} \cdot i \cdot \dfrac{(1+i)^n}{(1+i)^n-1}\).

- Amortization

- The process of paying off a loan with equal periodic payments, each split between interest on the outstanding balance and principal reduction. Early payments are mostly interest; later payments are mostly principal.

- Ordinary annuity vs annuity-due

- An ordinary annuity has payments at the end of each period (the standard for loans, and the basis of this table). An annuity-due has payments at the beginning of each period; its payment factor is the ordinary factor divided by \((1+i)\), giving slightly smaller payments.

FAQ

Is this an annuity-due or ordinary-annuity table? The visible formula computes the ordinary-annuity (end-of-period payment) factor, which is the standard amortizing loan/mortgage payment.

What does each cell mean? It is the payment per $1 of principal per period. Multiply it by your loan amount to get the real payment.

Why are zero rates or zero periods not allowed? They make the denominator zero and the formula undefined; only strictly positive rates and periods are accepted.