What is an Annuity Payment Calculator?

An annuity payment calculator finds the fixed, recurring payment (PMT) required to fully pay off a present value — such as a loan principal or an investment lump sum — over a set number of periods at a given interest rate. It is the standard math behind mortgage payments, car loans, and structured payouts. This tool is universal and currency-agnostic; enter amounts in any currency you like.

How to use it

Enter the present value (the amount borrowed or invested today), the annual interest rate as a percent, the term in years, and how many payments occur each year (monthly, quarterly, semi-annual, or annual). The calculator returns the payment per period plus the total amount paid and total interest over the life of the annuity.

The formula explained

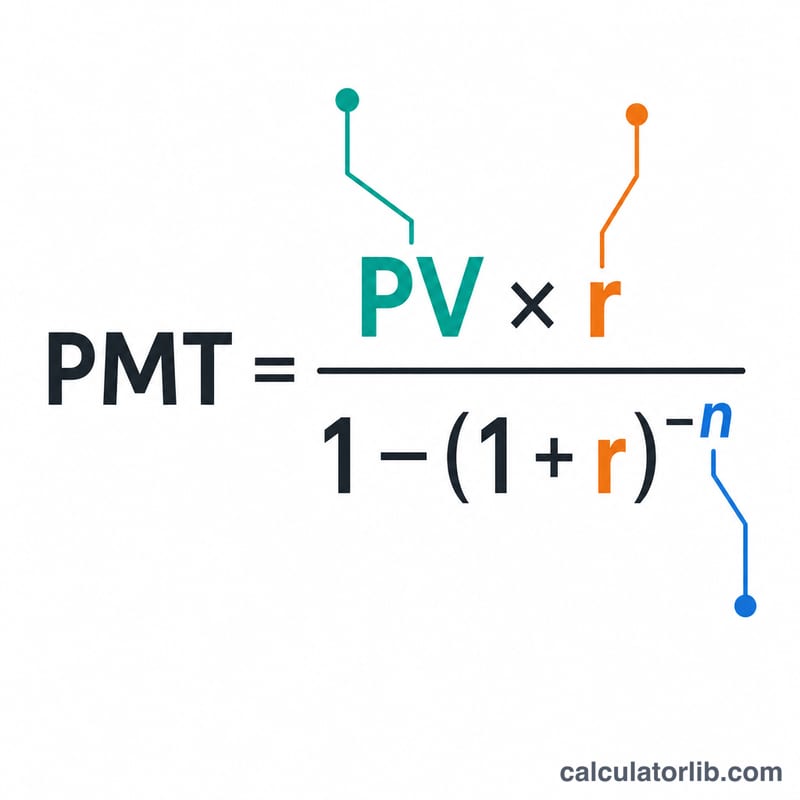

The core equation is $$\text{PMT} = \frac{PV \cdot r}{1 - (1 + r)^{-n}}$$ where PV is the present value, r is the periodic interest rate, and n is the total number of payments. The periodic rate is the annual rate divided by payments per year (\(r = \text{annual} \div f\)), and \(n\) equals \(\text{years} \times f\). When the rate is zero, the payment is simply \(PV \div n\).

Worked example

Borrow 100,000 at 6% annual interest, repaid monthly over 30 years. Here \(r = 0.06 \div 12 = 0.005\) and \(n = 30 \times 12 = 360\). Then $$\text{PMT} = \frac{100{,}000 \times 0.005}{1 - 1.005^{-360}} \approx 599.55 \text{ per month}.$$ Over 360 payments you pay about 215,838, of which roughly 115,838 is interest.

Payment Across Different Scenarios

The fixed periodic payment is found with \(\text{PMT} = \dfrac{PV \cdot r}{1 - (1 + r)^{-n}}\), where \(r\) is the periodic rate and \(n\) is the total number of payments. The tables below show how the payment, total amount paid, and total interest change as the present value, annual rate, term, and payment frequency vary.

$100,000 borrowed, monthly payments (freq = 12)

| Annual rate | Term | Monthly PMT | Total paid | Total interest |

|---|---|---|---|---|

| 4% | 15 yr (n=180) | $739.69 | $133,144 | $33,144 |

| 4% | 30 yr (n=360) | $477.42 | $171,870 | $71,870 |

| 6% | 15 yr (n=180) | $843.86 | $151,894 | $51,894 |

| 6% | 30 yr (n=360) | $599.55 | $215,838 | $115,838 |

| 8% | 15 yr (n=180) | $955.65 | $172,017 | $72,017 |

| 8% | 30 yr (n=360) | $733.76 | $264,155 | $164,155 |

Effect of payment frequency ($100,000 at 6% over 15 years)

| Frequency | Periodic rate \(r\) | Periods \(n\) | PMT | Total paid |

|---|---|---|---|---|

| Monthly (12) | 0.5000% | 180 | $843.86 | $151,894 |

| Quarterly (4) | 1.5000% | 60 | $2,539.34 | $152,361 |

| Semi-annual (2) | 3.0000% | 30 | $5,101.926 | $153,058 |

| Annual (1) | 6.0000% | 15 | $10,296.28 | $154,444 |

Each payment covers the interest accrued that period plus a portion of principal; total paid is \(\text{PMT} \times n\) and total interest is total paid minus \(PV\).

Interpreting Your Result

PMT is the constant amount you pay each period so that, after \(n\) payments, the present value is reduced to exactly zero. Early payments are mostly interest; as the balance shrinks, a larger share of each payment goes to principal.

Total paid is the sum of all payments, \(\text{PMT} \times n\). Total interest is the extra cost of financing — the difference between total paid and the original present value:

$$\text{Total Interest} = (\text{PMT} \times n) - PV$$Two levers drive total interest sharply higher:

- Higher interest rate — a larger \(r\) raises every payment and the cumulative interest. In the example above, moving $100,000 over 30 years from 4% to 8% nearly triples the interest paid.

- Longer term — a larger \(n\) lowers each individual payment but stretches the balance over more periods, so more interest accrues overall. The 30-year option costs far more in interest than the 15-year option at the same rate, even though the monthly payment is smaller.

Ordinary annuity vs. annuity-due: this calculator assumes an ordinary annuity, where payments are made at the end of each period (standard for most loans and mortgages). For an annuity-due (payments at the beginning of each period, common in leases and rent), each payment is smaller by a factor of \((1+r)\): \(\text{PMT}_{due} = \text{PMT}_{ordinary} / (1+r)\).

This is general educational information, not financial advice. Actual loan costs may include fees, insurance, or compounding conventions not captured here — confirm figures with your lender or a qualified professional.

Key Terms & Variables

- Present Value (PV)

- The amount owed or financed today — the loan principal or the lump sum the stream of payments is worth at the start.

- Payments per year (f)

- How often payments are made: 12 (monthly), 4 (quarterly), 2 (semi-annual), or 1 (annual). It converts the annual rate and term into per-period values.

- Periodic rate (r)

- The interest rate applied each period, \(r = \dfrac{\text{annual rate \%}}{100 \cdot f}\). For a 6% annual rate paid monthly, \(r = 0.06/12 = 0.005\) (0.5% per month).

- Number of periods (n)

- The total count of payments, \(n = \text{years} \cdot f\). A 15-year monthly loan has \(n = 15 \times 12 = 180\) payments.

- PMT

- The fixed payment per period that fully amortizes the present value over \(n\) periods at rate \(r\).

- Ordinary annuity

- A series of equal payments made at the end of each period — the convention used by this calculator and by most installment loans.

- Principal

- The portion of each payment that reduces the outstanding balance (as opposed to the portion that pays interest). Summed over the loan, total principal equals the original PV.

- Total interest

- The total financing cost over the life of the schedule: \((\text{PMT} \times n) - PV\).

FAQ

Is this an ordinary annuity? Yes — payments are assumed at the end of each period (ordinary annuity), which matches most loans.

What if the interest rate is 0%? The calculator divides the present value evenly across all periods (\(PV \div n\)).

Can I use it for savings withdrawals? Yes. The same formula tells you the sustainable periodic withdrawal from a lump sum earning a fixed return.