What Is a Balloon Payment Calculator?

A balloon loan has small regular payments during the term and a single large lump sum—the balloon payment—due at the end. This calculator works out exactly how big that final payment will be, given your loan amount, interest rate, term, and the periodic payment you actually make.

How to Use It

Enter the original loan amount, the annual interest rate, the loan term in years, and your fixed monthly payment. The calculator compounds the balance monthly, subtracts the value of all payments made, and shows the remaining balloon due at maturity, along with the total of regular payments and the grand total paid.

The Formula Explained

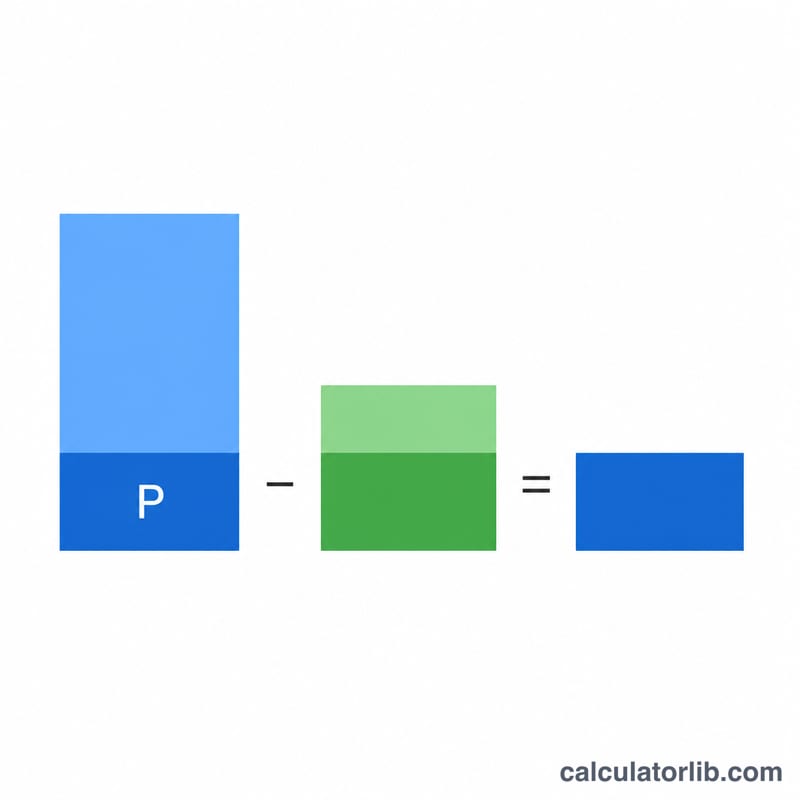

The remaining balance after n payments is:

$$\text{Balloon} = P\cdot(1+r)^{n} - \text{PMT}\cdot\frac{(1+r)^{n} - 1}{r}$$

where \(P\) is the principal, \(r\) is the periodic (monthly) interest rate = annual rate \(\div 12 \div 100\), \(n\) is the number of payments = years \(\times 12\), and \(\text{PMT}\) is the periodic payment. The first term grows the principal with compound interest; the second term is the future value of an ordinary annuity of payments, which reduces the balance.

Worked Example

Borrow $200,000 at 5% annual interest over 5 years, paying $1,073.64 per month. Monthly rate \(r = 0.05/12 \approx 0.0041667\), \(n = 60\). \((1+r)^{60} \approx 1.283359\). $$\text{Balloon} = 200000 \times 1.283359 - 1073.64 \times \frac{1.283359 - 1}{0.0041667} \approx 256671.7 - 73014.0 \approx 183{,}657.68$$ still owed at the end.

Key Terms Explained

A balloon loan is a loan whose scheduled monthly payments do not fully repay the borrowed amount over the loan term, leaving a large final lump sum — the balloon payment — due at the end. The terms below define every quantity that feeds the balloon formula \(B = A\,(1+r)^{n} - M\,\dfrac{(1+r)^{n}-1}{r}\).

- Principal (\(A\))

- The original amount of money borrowed, before any interest accrues. This is the loan amount on which the balance and balloon are calculated.

- Periodic interest rate (\(r\))

- The interest rate applied to each payment period. For a monthly loan it equals the annual nominal rate divided by 12 (and by 100 to convert from a percentage), i.e. \(r = \dfrac{\text{annual rate \%}}{1200}\). For example, a 6% annual rate gives a monthly rate of \(0.06/12 = 0.005\).

- Term / number of payments (\(n\))

- The total count of payment periods over the loan's life. For a monthly loan, \(n = 12 \times \text{years}\). On a balloon loan this is the schedule the payment is based on or the period until the balloon comes due.

- Periodic payment (PMT, \(M\))

- The fixed amount paid each period (typically monthly). On a balloon loan this payment is deliberately smaller than the amount needed to fully amortize the principal by maturity, which is what leaves a balance behind.

- Balloon payment (\(B\))

- The single large lump-sum amount still owed at maturity after all the regular periodic payments have been made. It equals the future value of the principal minus the future value of the payments made.

- Amortization

- The gradual reduction of a loan's principal balance through scheduled payments, where each payment covers accrued interest first and applies the remainder to principal. A fully amortizing loan ends at a zero balance; a balloon loan only partially amortizes.

- Future value of an annuity

- The accumulated value of a stream of equal periodic payments grown at the periodic interest rate, given by \(M\,\dfrac{(1+r)^{n}-1}{r}\). In the balloon formula this term represents how much the borrower's payments have effectively offset the compounding principal.

- Maturity

- The date the loan term ends and any remaining balance — the balloon payment — becomes due in full. At maturity the borrower must pay off, refinance, or otherwise settle the balloon.

FAQ

Why is the balloon so large? Because the monthly payment is set low (often interest-mostly), little principal is repaid, leaving a big lump sum.

Can the balloon be zero? Yes—if the payment is high enough to fully amortize the loan, the balance reaches zero and no balloon is due.

Is this currency or country specific? No. The math is universal; just enter amounts in your own currency.