What this calculator does

This Mortgage Payment Calculator works out your fixed monthly principal and interest (P&I) payment on a home loan. It uses the standard US convention of monthly compounding, where the annual interest rate is divided by 12. It does not include property taxes, homeowners insurance, PMI, or HOA dues — those are separate line items in a full PITI estimate.

How to use it

Enter the mortgage amount (the loan principal or current balance), the term and whether the term is in years or months, and the annual interest rate as a percent. Press calculate to see your level monthly payment, the total number of payments, the total amount paid over the life of the loan, and the total interest.

The formula explained

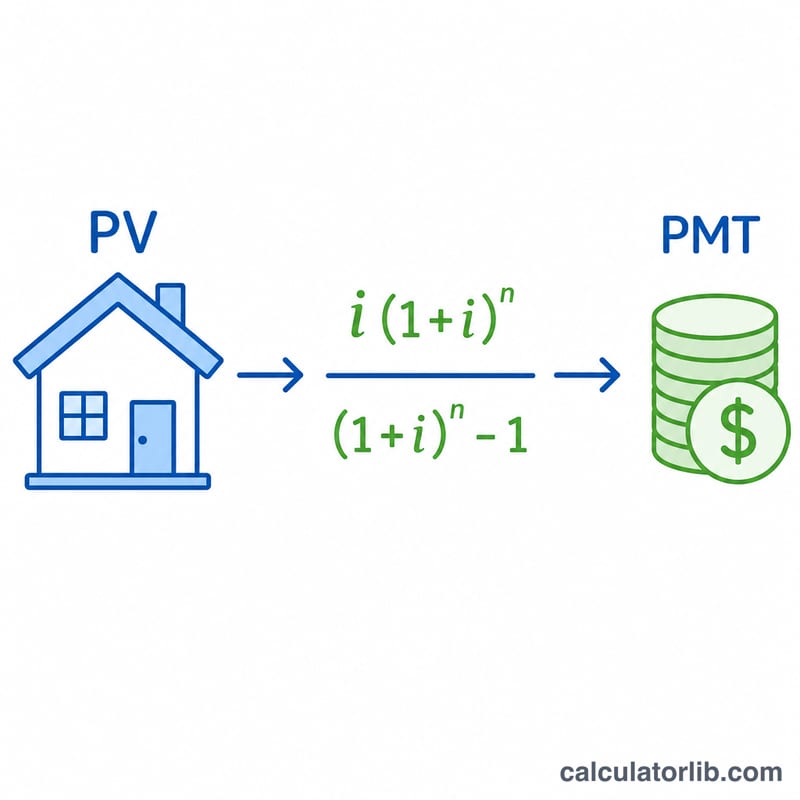

The level payment of an amortizing loan is an annuity payment:

$$\text{PMT} = \text{PV} \cdot \frac{i\,(1+i)^n}{(1+i)^n - 1}$$

Here \(\text{PV}\) is the loan amount, \(i = \text{annualRate} / 100 / 12\) is the monthly interest rate, and \(n\) is the total number of monthly payments (years × 12, or months as entered). If the rate is 0, the denominator becomes zero, so the calculator falls back to \(\text{PMT} = \text{PV} / n\) — spreading the principal evenly.

Worked example

Loan of $175,000 over 30 years at 4.125%: \(i = 0.0034375\), \(n = 360\), and \((1+i)^n \approx 3.4397\). The payment is $$175000 \times 0.0034375 \times \frac{3.4397}{3.4397 - 1} \approx \$848.14$$ per month. Over 360 payments that totals about $305,331, of which roughly $130,331 is interest.

FAQ

Does this include taxes and insurance? No. It is principal and interest only. Add escrowed taxes and insurance separately for a full housing cost.

What rate should I enter? Enter the nominal annual interest rate (APR-style nominal rate), not a monthly rate. The tool converts it to monthly.

Why does total interest seem high? Long terms mean interest accumulates for decades. Shortening the term or making extra payments dramatically reduces total interest.