What Is a Deferred Annuity?

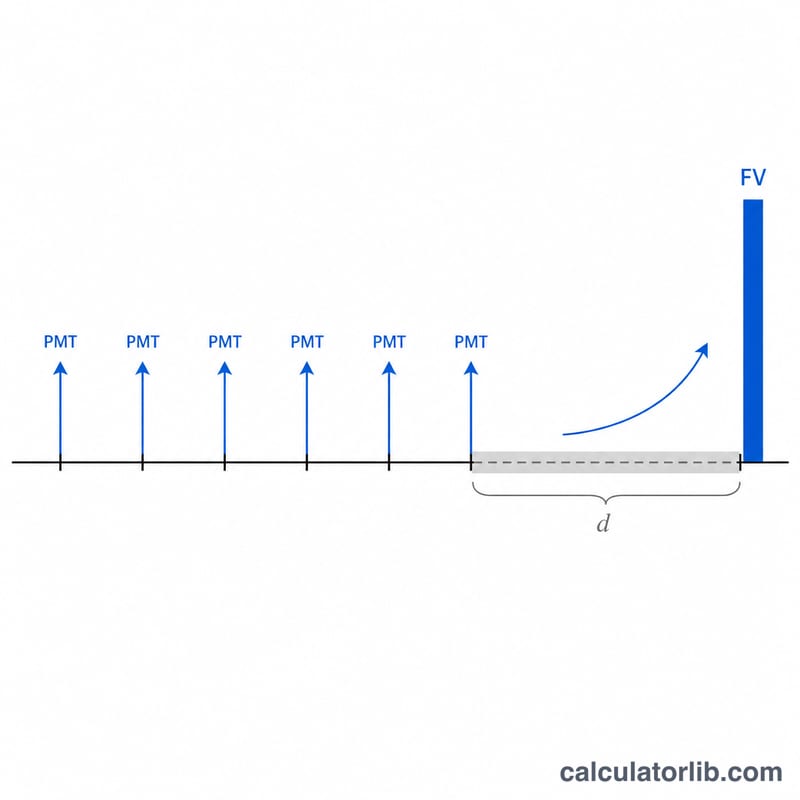

A deferred annuity is a savings vehicle in which you make a series of equal contributions during an accumulation phase, then let the accumulated balance continue to grow (deferred) for an additional number of periods before withdrawals begin. This calculator computes the future value at the end of that combined accumulation-plus-deferral window. It is a universal time-value-of-money tool and does not depend on any specific country or tax regime.

How to Use This Calculator

Enter four values: the payment made each period (PMT), the interest rate earned per period (as a percent), the number of payment periods (n), and the number of deferral periods (d) during which no payments are made but interest keeps compounding. The result shows the final future value, the value at the moment payments stop, the total of all contributions, and the total interest earned.

The Formula Explained

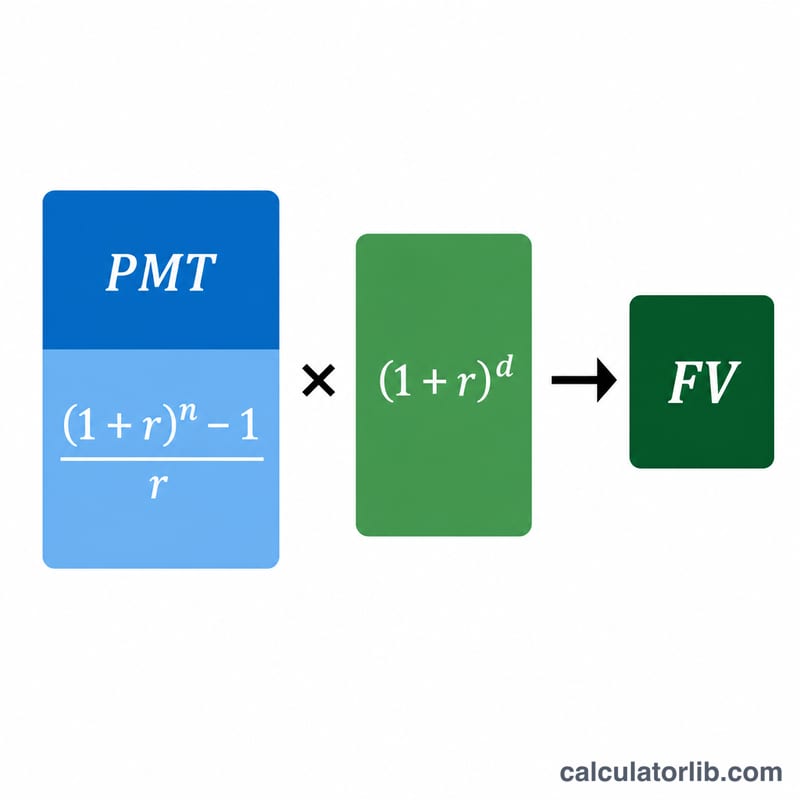

The future value of an ordinary annuity is \( \text{PMT} \cdot \frac{(1+r)^{n}-1}{r} \). Because the balance is then left to grow for \(d\) further periods, it is multiplied by the compound growth factor \( (1+r)^{d} \). Combined, this gives the deferred annuity formula:

$$FV = \text{PMT} \cdot \frac{(1+r)^{n}-1}{r} \cdot (1+r)^{d}$$where

$$\left\{ \begin{aligned} r &= \frac{\text{Rate (\%)}}{100} \\ n &= \text{Periods} \\ d &= \text{Deferral Periods} \end{aligned} \right.$$When the rate is zero, the future value simply equals \( \text{PMT} \times n \).

Worked Example

Suppose you deposit $1,000 per year for 10 years earning 5% annually, then defer for 5 more years. The annuity value after 10 years is

$$1000 \times \frac{1.05^{10} - 1}{0.05} \approx \$12{,}577.89$$Growing that for 5 years:

$$12{,}577.89 \times 1.05^{5} \approx \$16{,}053.27$$You contributed $10,000, so you earned about $6,053.27 in interest.

FAQ

What is the deferral period? It is the time after your last payment during which the balance keeps compounding before payouts begin.

Does this assume payments at the end of each period? Yes, it uses the ordinary annuity (payment-in-arrears) convention.

Can the rate be entered monthly? Yes — just make sure r, n and d all use the same period (e.g., all monthly).