What is an annuity?

An annuity is a series of equal payments made at regular intervals — for example, monthly retirement contributions, loan repayments, or pension income. This calculator computes both the future value (how much the payments grow to) and the present value (what those future payments are worth today) given a payment amount, an interest rate per period, and the number of periods. It works for any currency since the math is unit-agnostic.

How to use it

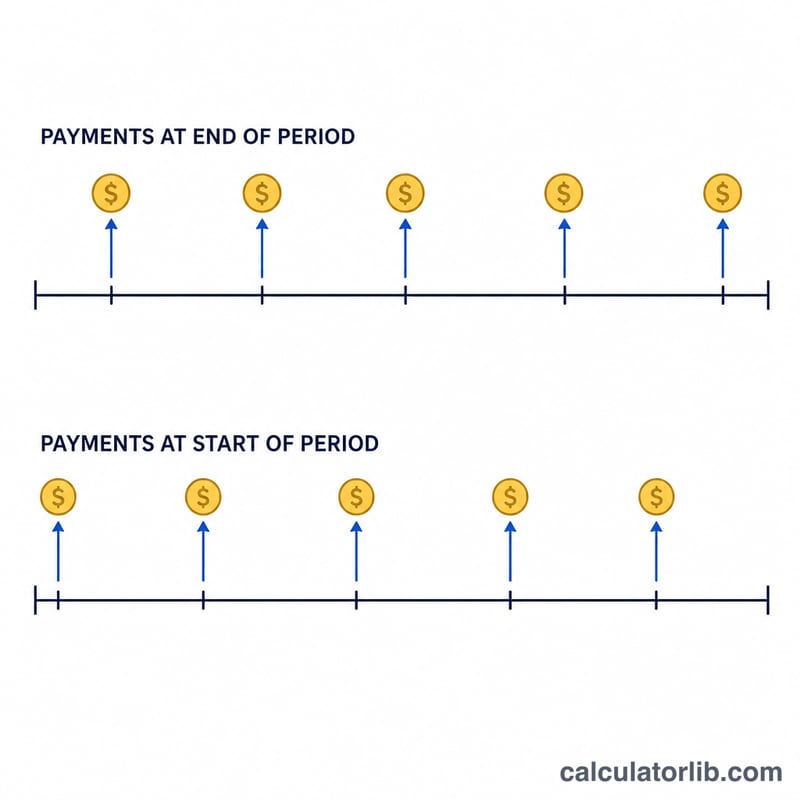

Enter the payment made each period (PMT), the interest rate per period as a percentage, and the total number of periods (n). Make sure the rate and the period count use the same time unit: for monthly payments, use the monthly rate and the number of months. Choose Ordinary if payments occur at the end of each period (the typical case) or Due if they occur at the start.

The formula explained

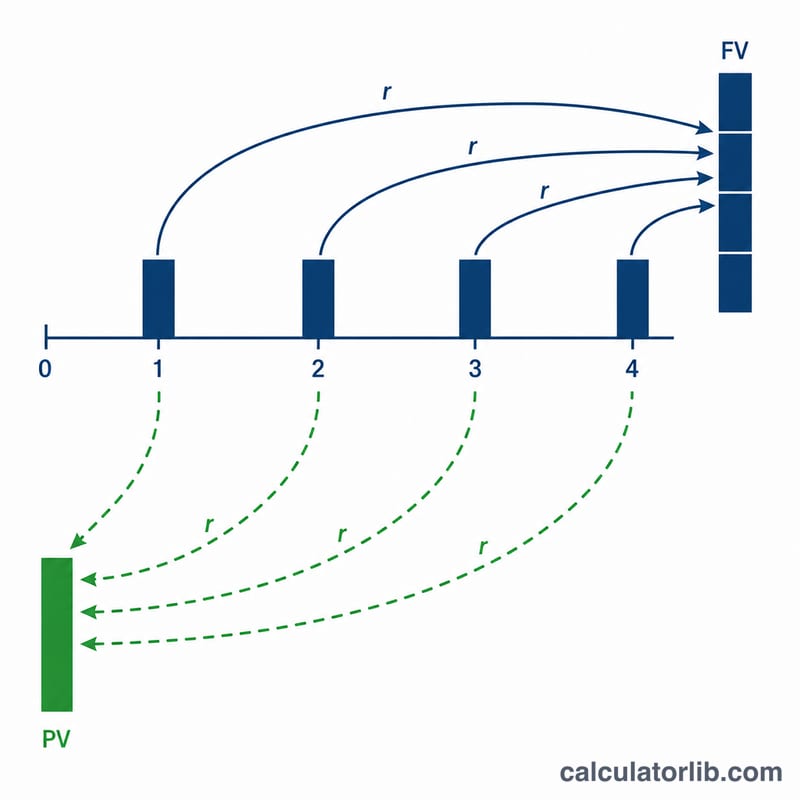

With \(r\) as the periodic rate, the future value is $$FV = \text{PMT} \cdot \frac{(1+r)^{n}-1}{r}$$ and the present value is $$PV = \text{PMT} \cdot \frac{1-(1+r)^{-n}}{r}.$$ For an annuity due, each result is multiplied by \((1 + r)\) because every payment earns one extra period of interest. When the rate is zero, both values simply equal \(\text{PMT} \times n\).

Worked example

Suppose you invest $1,000 at the end of each year for 10 years at 5% annually. $$FV = 1000 \times \frac{(1.05)^{10} - 1}{0.05} = 1000 \times 12.5779 = \$12{,}577.89.$$ You contribute $10,000 total, so you earn about $2,577.89 in interest. The present value is $$1000 \times \frac{1 - 1.05^{-10}}{0.05} = \$7{,}721.73.$$

Annuity Factor Reference Table

The two core annuity factors depend only on the periodic rate \(r\) and the number of periods \(n\). Multiply a factor by your payment (PMT) to get the result:

$$FV = \text{PMT}\cdot\frac{(1+r)^{n}-1}{r}\qquad PV = \text{PMT}\cdot\frac{1-(1+r)^{-n}}{r}$$

The rates below are treated as the rate per period (e.g. an annual rate applied to annual payments). If you pay monthly, divide the annual rate by 12 and count months as periods.

Future Value factor \(\frac{(1+r)^{n}-1}{r}\)

| Rate per period | n = 5 | n = 10 | n = 15 | n = 20 | n = 25 | n = 30 |

|---|---|---|---|---|---|---|

| 2% | 5.204 | 10.950 | 17.293 | 24.297 | 32.030 | 40.568 |

| 4% | 5.416 | 12.006 | 20.024 | 29.778 | 41.646 | 56.085 |

| 5% | 5.526 | 12.578 | 21.579 | 33.066 | 47.727 | 66.439 |

| 6% | 5.637 | 13.181 | 23.276 | 36.786 | 54.865 | 79.058 |

| 8% | 5.867 | 14.487 | 27.152 | 45.762 | 73.106 | 113.283 |

| 10% | 6.105 | 15.937 | 31.772 | 57.275 | 98.347 | 164.494 |

Present Value factor \(\frac{1-(1+r)^{-n}}{r}\)

| Rate per period | n = 5 | n = 10 | n = 15 | n = 20 | n = 25 | n = 30 |

|---|---|---|---|---|---|---|

| 2% | 4.713 | 8.983 | 12.849 | 16.351 | 19.523 | 22.396 |

| 4% | 4.452 | 8.111 | 11.118 | 13.590 | 15.622 | 17.292 |

| 5% | 4.329 | 7.722 | 10.380 | 12.462 | 14.094 | 15.372 |

| 6% | 4.212 | 7.360 | 9.712 | 11.470 | 12.783 | 13.765 |

| 8% | 3.993 | 6.710 | 8.559 | 9.818 | 10.675 | 11.258 |

| 10% | 3.791 | 6.145 | 7.606 | 8.514 | 9.077 | 9.427 |

Example: paying $1,000 per year for 10 years at 5% gives an FV factor of 12.578, so the future value is \(1000\times 12.578 = \$12{,}578\). Verify: $12,577.89.

Annuity Scenarios Compared

Each scenario converts the annual rate to a per-period rate \(r\) and counts periods \(n\) to match the payment frequency. Total contributed is simply \(\text{PMT}\times n\); FV and PV come from the formulas above. Annuity-due values (payments at the start of each period) equal the ordinary values multiplied by \((1+r)\).

| Scenario | PMT | Periodic rate \(r\) | n | Type | Total contributed | Future value | Present value |

|---|---|---|---|---|---|---|---|

| $500/mo, 6%/yr, 20 yr | $500 | 0.5% | 240 | Ordinary | $120,000 | $231,020.45 | $69,790.39 |

| $500/mo, 6%/yr, 20 yr | $500 | 0.5% | 240 | Due | $120,000 | $232,175.55 | $70,139.34 |

| $1,000/yr, 5%/yr, 10 yr | $1,000 | 5% | 10 | Ordinary | $10,000 | $12,577.89 | $7,721.73 |

| $200/mo, 4%/yr, 30 yr | $200 | 0.3333% | 360 | Ordinary | $72,000 | $138,856.65 | $41,894.81 |

| $200/mo, 4%/yr, 30 yr | $200 | 0.3333% | 360 | Due | $72,000 | $139,319.51 | $42,034.46 |

Two patterns stand out: (1) switching from an ordinary annuity to an annuity due lifts both FV and PV by exactly one period's growth, \((1+r)\); and (2) higher payment frequency and longer horizons dramatically widen the gap between what you contribute and the future value, thanks to compounding.

Key Terms & Variables

- PMT — Payment per period

- The fixed cash flow paid or received each period (e.g. $500 every month). All standard annuity formulas assume this amount stays constant.

- \(r\) — Periodic interest rate

- The interest rate applied to a single period, expressed as a decimal. It must match the payment frequency: for monthly payments at a 6% annual rate, \(r = 0.06/12 = 0.005\) (0.5% per month).

- \(n\) — Number of periods

- The total count of payments, not the number of years. Monthly payments for 20 years give \(n = 20\times 12 = 240\).

- FV — Future value

- The accumulated worth of all payments at the end of the annuity, including interest earned. Used to project savings goals.

- PV — Present value

- The worth today of all future payments, discounted at rate \(r\). Used to price loans, leases, and lottery payouts.

- Ordinary annuity

- Payments occur at the end of each period (e.g. most loan and bond payments). This is the default for the formulas shown.

- Annuity due

- Payments occur at the beginning of each period (e.g. rent, insurance premiums). Each cash flow earns one extra period of interest, so \(FV_{due} = FV_{ordinary}\times(1+r)\) and likewise for PV.

- Periodic vs annual rate

- The annual (nominal) rate is the headline figure; the periodic rate is what actually drives each compounding step. Always divide the annual rate by the number of periods per year before using it as \(r\), and never mix an annual rate with a monthly period count.

FAQ

What rate should I enter for monthly payments? Divide the annual rate by 12. For 6% annual, use 0.5 per month and set periods to the number of months.

What's the difference between ordinary and due? Ordinary annuities pay at period end; annuity due pays at period start, giving a slightly higher value because money is invested earlier.

Why is present value lower than future value? Present value discounts future payments back to today, while future value compounds them forward — so PV is always smaller when the rate is positive.