What Is an Immediate Annuity Calculator?

An immediate annuity (also called a single-premium immediate annuity, or SPIA) converts a lump sum of money into a stream of guaranteed periodic income payments that begin right away. This calculator estimates how much income you would receive each period based on your premium, an assumed interest rate, the length of the payout, and how often payments are made.

How to Use It

Enter the principal (the lump sum or premium you pay), the assumed annual interest rate the insurer credits, the payout period in years, and the payment frequency (monthly, quarterly, semi-annual, or annual). The calculator returns the income per payment, the number of payments, the total payout, and the total interest earned over the contract.

The Formula Explained

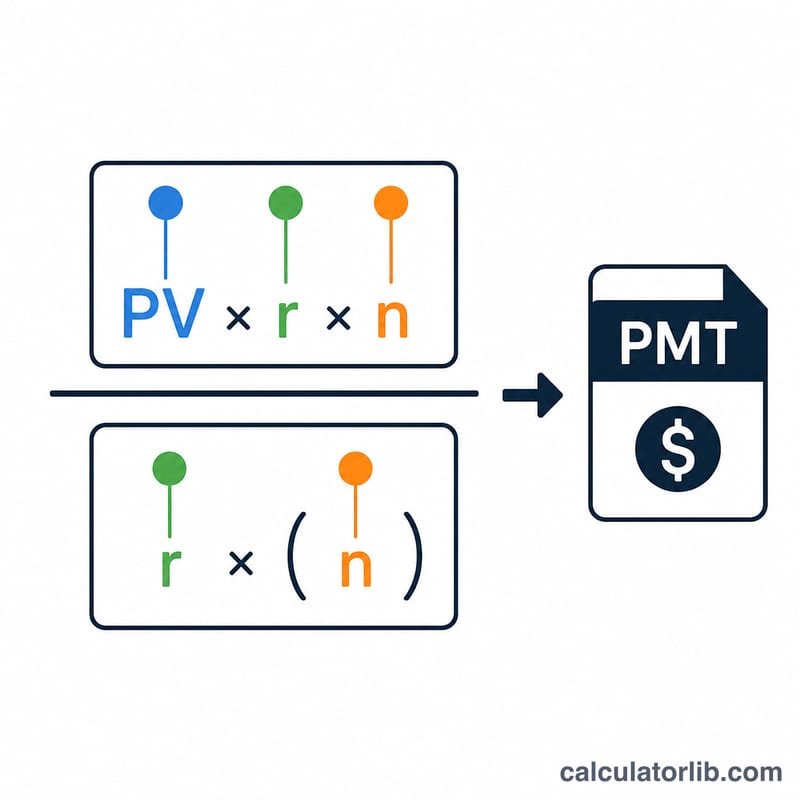

The payment is the standard annuity (amortization) formula: $$\text{PMT} = \frac{PV \cdot r}{1 - (1 + r)^{-n}}$$ Here PV is the present value (your premium), r is the periodic interest rate (annual rate \(\div\) payments per year), and n is the total number of payments (years \(\times\) payments per year). When the rate is zero, the payment simply equals \(PV \div n\).

Worked Example

Suppose you pay a $100,000 premium for an annuity earning 5% annually, paid monthly over 20 years. The periodic rate is \(0.05 \div 12 = 0.0041667\) and there are 240 payments. $$\text{PMT} = \frac{100{,}000 \times 0.0041667}{1 - 1.0041667^{-240}} \approx \$659.96 \text{ per month}$$ for a total payout of about $158,389 — roughly $58,389 in interest.

FAQ

Is this guaranteed income? The calculator shows a math estimate. Actual insurer quotes depend on age, gender, mortality assumptions, fees, and current rates.

Does it account for inflation? No — it models a fixed (non-indexed) annuity. Inflation-adjusted annuities pay less initially.

What rate should I use? Use a rate near what insurers are currently crediting (often 3%–6%) for a realistic estimate.