What Is an Annuity Due?

An annuity due is a series of equal payments made at the beginning of each period, rather than at the end. Rent, lease payments, and many insurance premiums work this way. Because each payment arrives one period earlier than in an ordinary annuity, every payment earns (or is discounted by) one extra period of interest. This calculator computes both the future value (FV) and present value (PV) of an annuity due. The tool is universal — it works for any currency and any compounding frequency, as long as the rate and the number of periods use the same period length.

How to Use It

Enter the payment made each period (PMT), the interest rate per period as a percentage, and the total number of periods (n). If payments are monthly and your annual rate is 6%, use 0.5% per month and the number of months. The calculator returns the future value, the present value, your total contributions, and the interest earned.

The Formula Explained

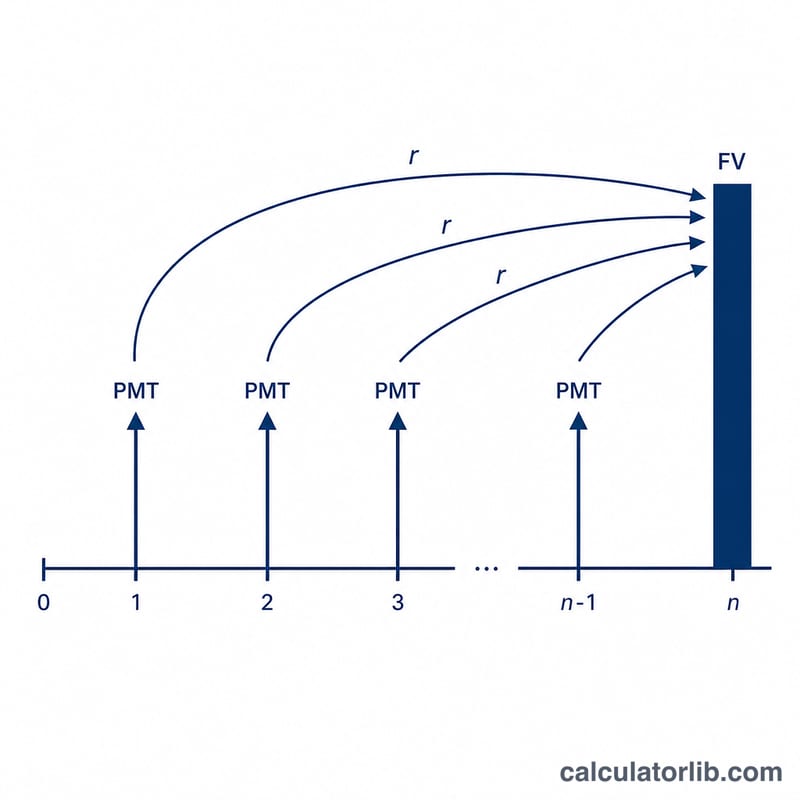

The annuity-due formulas are simply the ordinary-annuity formulas multiplied by an extra (1 + r) factor that accounts for the one-period-earlier timing:

$$FV = \text{PMT} \cdot \frac{(1+r)^{\text{n}}-1}{r} \cdot (1+r)$$

$$PV = \text{PMT} \cdot \frac{1-(1+r)^{-\text{n}}}{r} \cdot (1+r)$$

Here \(r\) is the periodic rate (annual rate ÷ periods per year) and \(n\) is the total number of payments.

Worked Example

Suppose you deposit $1,000 at the start of each year for 10 years, earning 5% annually. With \(r = 0.05\) and \(n = 10\): $$FV = 1000 \times \frac{1.05^{10} - 1}{0.05} \times 1.05 \approx \$13{,}206.79$$ Your total contributions are $10,000, so the interest earned is about $3,206.79. The present value of that same stream is about $8,107.82.

FAQ

How is an annuity due different from an ordinary annuity? Payments come at the start of each period instead of the end, so each one earns an extra period of interest — making the FV and PV higher by a factor of \((1 + r)\).

What rate should I enter? Use the rate for a single period. For monthly payments at a 12% annual rate, enter 1 (i.e. 1% per month) and set periods to the number of months.

What if the interest rate is 0%? Then both FV and PV simply equal \(\text{PMT} \times n\), since there is no growth or discounting.