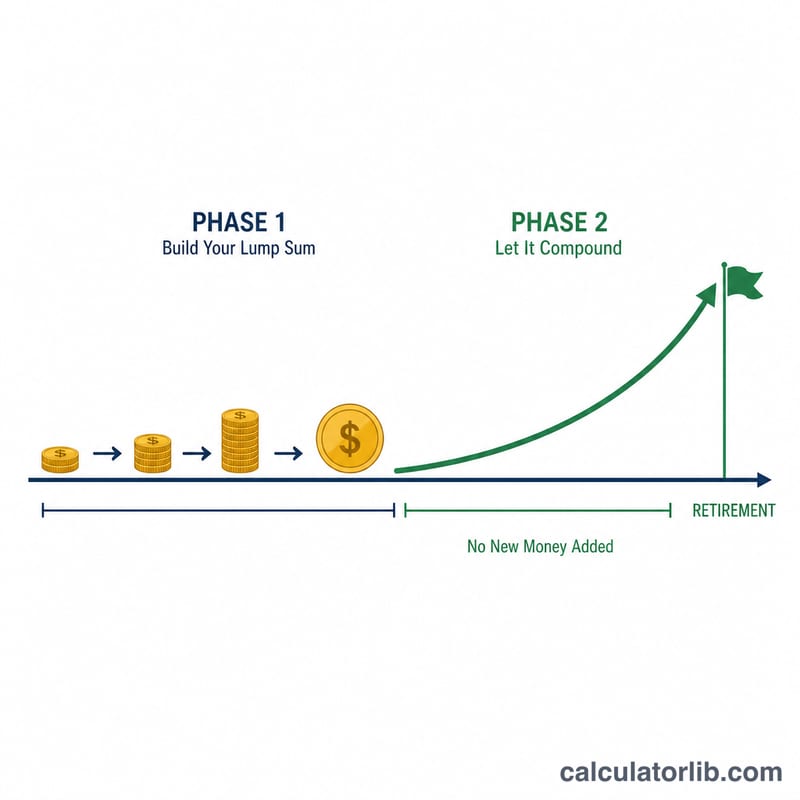

What Is Coast FIRE?

Coast FIRE is the point at which you have enough invested that, without adding another dollar, compound growth alone will carry your portfolio to your full retirement target by the time you stop working. Once you hit your Coast FIRE number you can "coast" — covering only current living costs while your existing investments grow untouched. It's a popular milestone within the broader FIRE (Financial Independence, Retire Early) movement.

How to Use This Calculator

Enter your current age, your planned retirement age, your expected annual expenses in retirement, a safe withdrawal rate (4% is the common rule of thumb), and a real (inflation-adjusted) annual return. Optionally add your current invested savings to see your progress. The calculator returns the lump sum you'd need invested today to coast to your goal.

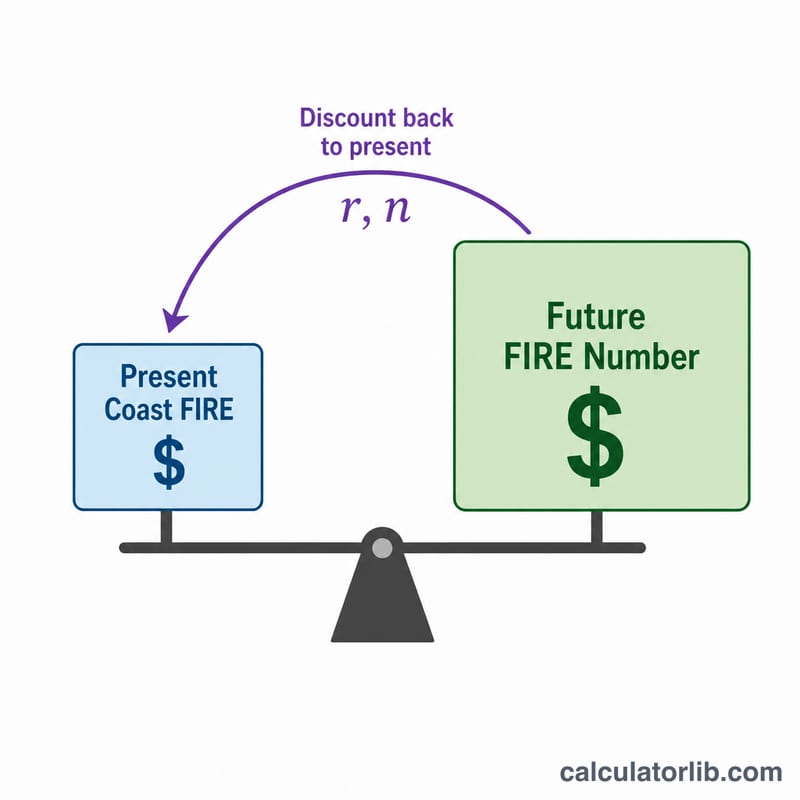

The Formula Explained

First we find your full FIRE Number = Annual Expenses ÷ Safe Withdrawal Rate. Then we discount it back to today using the real return:

$$\text{Coast FIRE} = \frac{F}{(1+r)^{n}}$$where \(r\) is the real annual return as a decimal and \(n\) is the number of years until retirement. Using a real return means your expenses and target are expressed in today's dollars.

Worked Example

Suppose you're 30, retiring at 65 (\(n = 35\) years), need $40,000/year, use a 4% withdrawal rate, and expect a 5% real return.

$$\text{FIRE Number} = \frac{40{,}000}{0.04} = \$1{,}000{,}000$$$$\text{Coast FIRE} = \frac{1{,}000{,}000}{(1.05)^{35}} = \frac{1{,}000{,}000}{5.516} \approx \$181{,}290$$Invest that once and never save again, and you'd still hit $1M by 65.

FAQ

Should I use a real or nominal return? Use a real (inflation-adjusted) return, typically 4–7%, so your expenses stay in today's dollars.

What withdrawal rate should I pick? 4% is the classic Trinity-study rule; conservative planners use 3.5% or 3%.

Does this include Social Security or pensions? No — it assumes your portfolio funds your full expenses. Subtract guaranteed income from expenses first if you want to account for it.