What Is the Annual Withdrawal Amount Calculator?

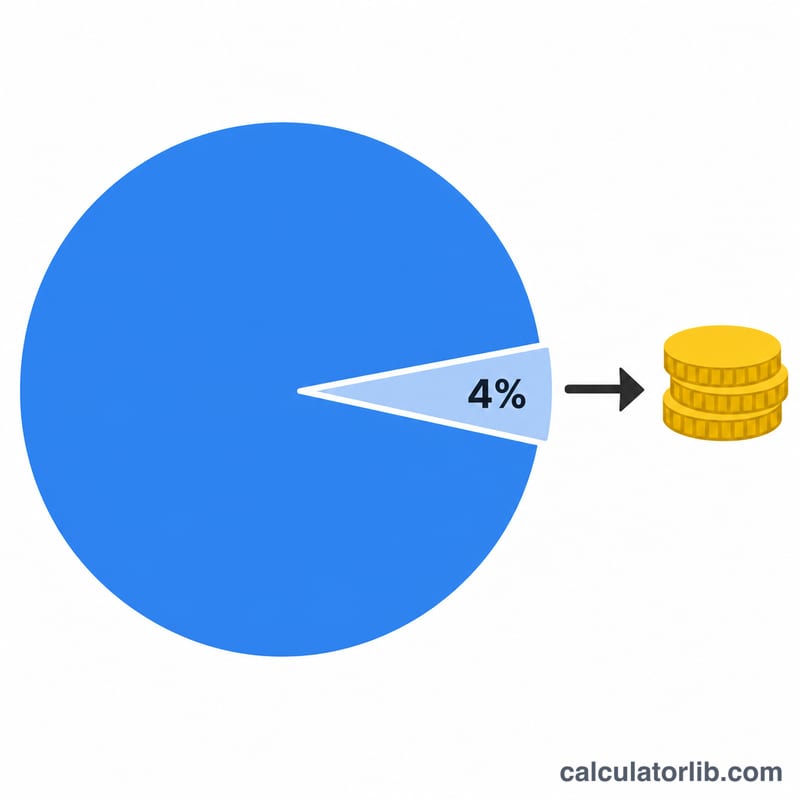

This tool estimates how much money you can take out of an investment or retirement portfolio each year based on a withdrawal rate you choose. It is built around the popular "4% rule" idea, a guideline often used to gauge a sustainable spending level in retirement, but you can enter any rate. The calculator is jurisdiction-neutral — it is pure arithmetic and works with any currency, though the dollar sign is shown for illustration.

How to Use It

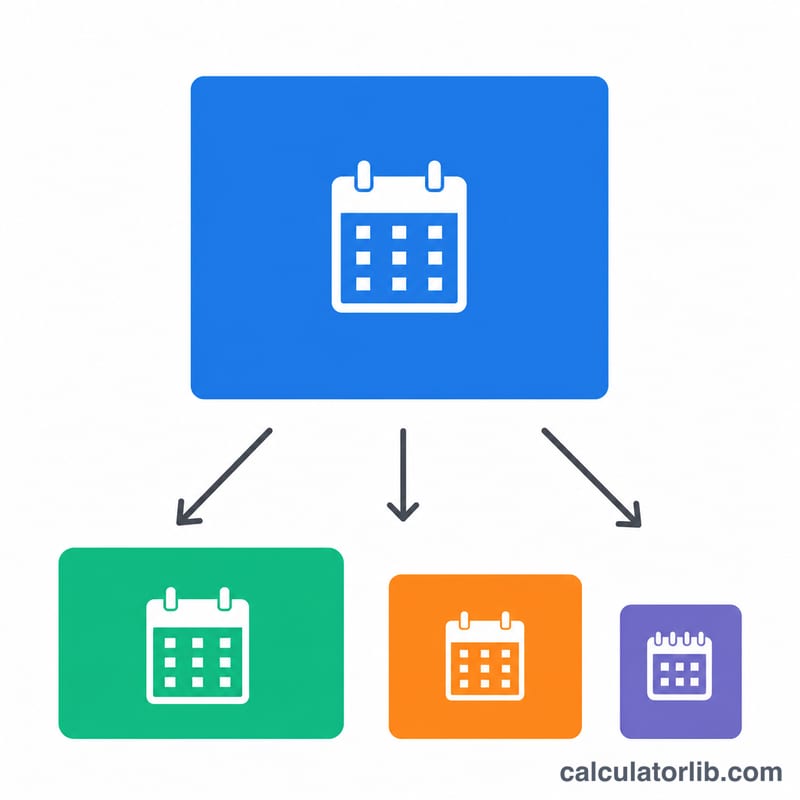

Enter your total portfolio value and the annual withdrawal rate you want to apply. The calculator instantly shows the resulting annual withdrawal, then breaks it down into monthly and weekly equivalents so you can plan a steady income.

The Formula Explained

The core formula is simple:

$$\text{Annual Withdrawal} = \text{Portfolio Value} \times \frac{\text{Withdrawal Rate (\%)}}{100}$$The monthly figure divides the annual amount by 12, and the weekly figure divides it by 52. The withdrawal rate is the percentage of your portfolio you plan to spend in the first year; many planners use 3%–5%.

Worked Example

Suppose you have a portfolio of $1,000,000 and choose a 4% withdrawal rate. Your annual withdrawal is \(1{,}000{,}000 \times 0.04 = \$40{,}000\). That is about $3,333.33 per month or roughly $769.23 per week.

FAQ

Is the 4% rule guaranteed? No. It is a historical guideline, not a promise. Market returns, inflation, and how long you live all affect whether a withdrawal rate is sustainable.

Does this account for inflation or investment growth? No. This calculator gives a snapshot based on your current portfolio value and rate. It does not project balances forward or adjust for inflation.

What withdrawal rate should I choose? A lower rate (e.g. 3%) is more conservative and likely to last longer, while a higher rate provides more income but increases the risk of depleting the portfolio. Consult a financial advisor for personalized guidance.