What This Calculator Does

When you take money out of a tax-deferred retirement account—such as a traditional IRA or 401(k)—the distribution is generally treated as ordinary income and taxed accordingly. The Retirement Withdrawal After-Tax Calculator estimates how much of a gross withdrawal you actually keep once income taxes are applied, so you can plan distributions that meet your spending needs without surprises.

How to Use It

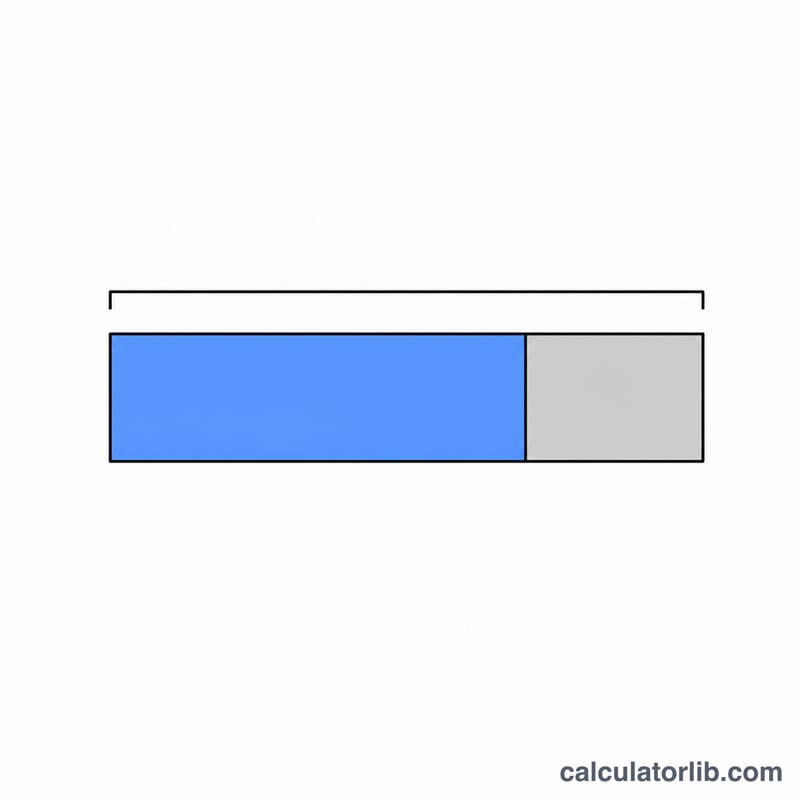

Enter the gross (pre-tax) amount you plan to withdraw, then enter your effective tax rate as a percentage. Your effective rate is the blended share of the withdrawal that goes to taxes—often lower than your top marginal bracket. The calculator returns your net after-tax amount, the estimated tax owed, and your inputs for reference.

The Formula Explained

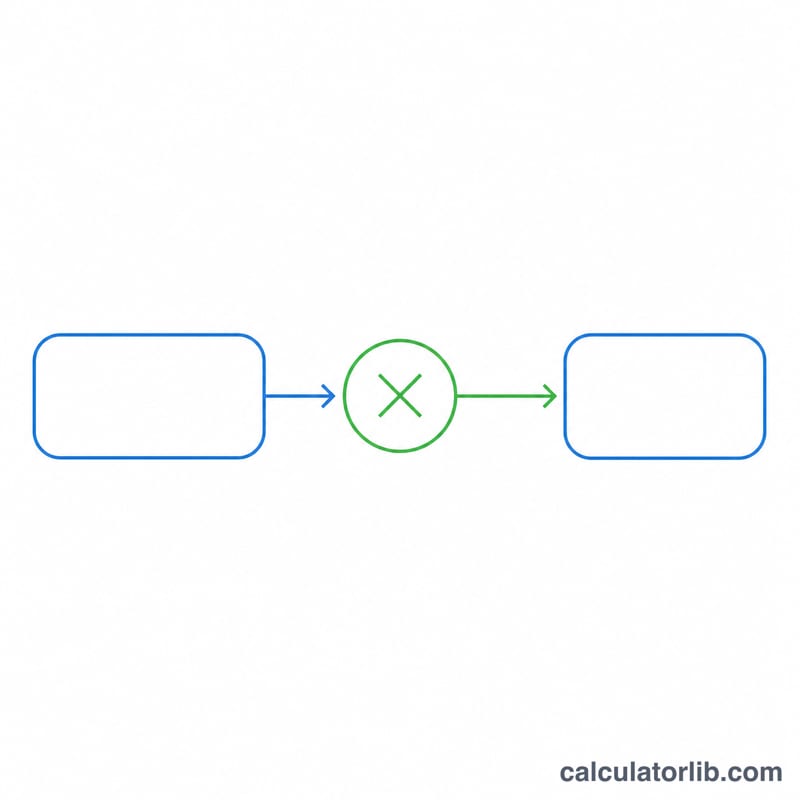

The math is simple: $$\text{Net} = \text{Gross} \times (1 - r)$$ where \(r\) is the tax rate expressed as a decimal. The tax owed is \(\text{Gross} \times r\). For example, a 22% rate becomes \(r = 0.22\), so you keep 78% of the withdrawal.

Worked Example

Suppose you withdraw $50,000 at an effective tax rate of 22%. Tax owed = $$50{,}000 \times 0.22 = \$11{,}000.$$ Net withdrawal = $$50{,}000 \times (1 - 0.22) = 50{,}000 \times 0.78 = \$39{,}000.$$ You would need to withdraw more than $50,000 if you require $50,000 of spendable cash.

FAQ

Is this US-specific? The tool is a general before-and-after-tax estimator. It does not model brackets, early-withdrawal penalties, Roth tax-free distributions, or state taxes—use a single effective rate that reflects your situation.

What rate should I enter? Use your expected effective (average) income-tax rate on the distribution, including any applicable state tax, rather than your top marginal rate.

Does it include the 10% early-withdrawal penalty? No. If a penalty applies, add it to your effective rate to approximate the combined hit.