What this calculator does

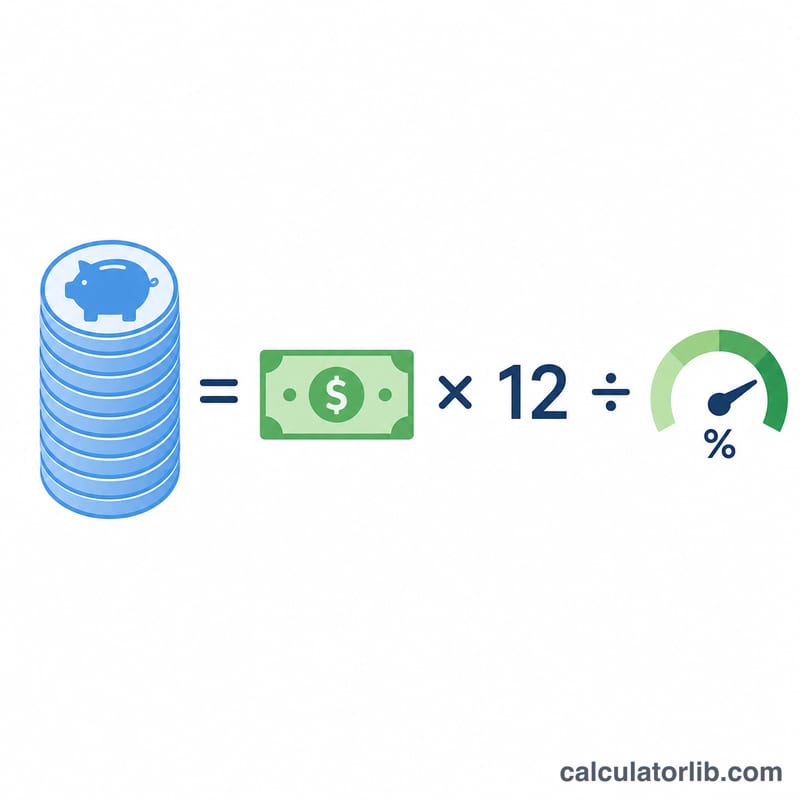

This tool estimates the lump sum of savings — your "nest egg" — needed to generate a chosen monthly income in retirement. It works by annualizing your desired monthly income and dividing by a safe annual withdrawal rate, the percentage of your portfolio you plan to draw each year.

How to use it

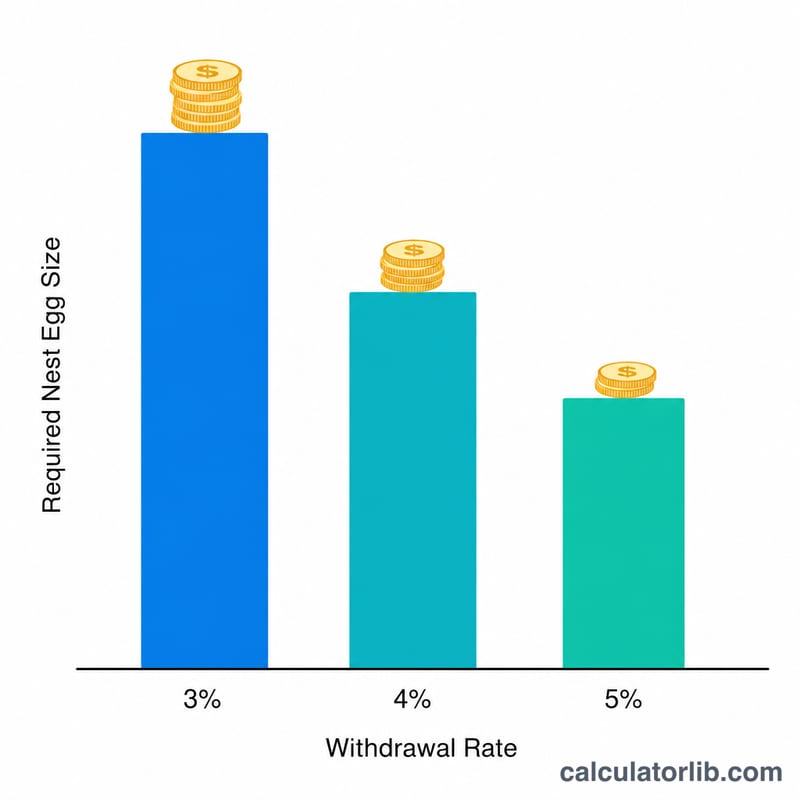

Enter the monthly income you want your savings to provide, then enter the annual withdrawal rate you consider sustainable. Many planners use the "4% rule" as a starting point, though more conservative savers prefer 3% to 3.5%. The result is the total savings needed at retirement.

The formula explained

The calculation is $$\text{Nest Egg} = \frac{\text{Monthly Income} \times 12}{\text{Withdrawal Rate}}$$ Multiplying monthly income by 12 gives the annual income target. Dividing by the withdrawal rate (as a decimal) scales that up to the portfolio size required. A lower withdrawal rate demands a larger nest egg because you are drawing a smaller slice each year.

Worked example

Suppose you want $4,000 per month and assume a 4% withdrawal rate. Annual income is \(4{,}000 \times 12 = \$48{,}000\). Dividing by 0.04 gives $1,200,000. So you would need roughly $1.2 million saved to support that income under the 4% rule.

FAQ

What withdrawal rate should I use? The classic 4% rule is common, but lower rates (3–3.5%) give a bigger safety margin for long retirements.

Does this account for inflation? The withdrawal rate concept assumes inflation-adjusted withdrawals, but this calculator gives a present-day target and does not project future inflation.

Is this guaranteed? No. Withdrawal-rate rules are guidelines based on historical returns and do not guarantee your money will last; consult a financial professional.