What This Calculator Does

The Savings Needed for Target Passive Income Calculator tells you how large a portfolio you must build to live off its returns. Enter the annual income you want to receive without working, plus the yield or rate of return you realistically expect, and it instantly shows the principal required.

How to Use It

Type your desired annual passive income (for example, $40,000). Enter the expected annual yield as a percentage — dividends, interest, or a safe withdrawal rate such as 4%. The calculator divides your income goal by the decimal yield to reveal the nest egg you need, and also shows the equivalent monthly income.

The Formula Explained

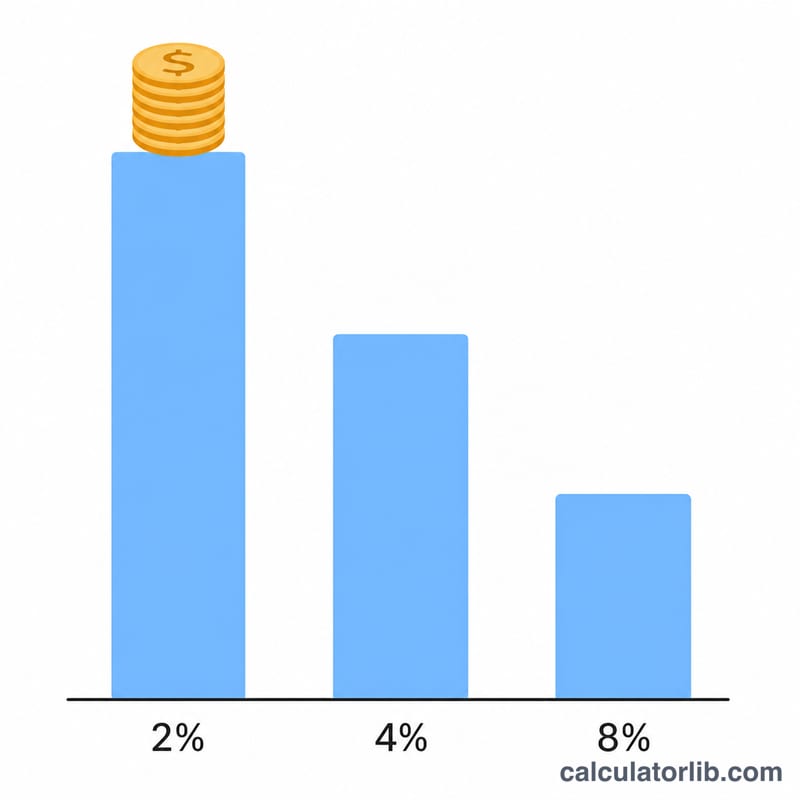

The core relationship is $$\text{Principal} = \frac{\text{Annual Income}}{\text{Annual Yield}}$$ The yield is expressed as a decimal, so 4% becomes \(0.04\). A higher yield means you need less capital; a lower yield means you need more. This is the same logic behind the popular "4% rule" used in retirement planning, where withdrawing 4% per year implies you need 25× your annual spending.

Worked Example

Suppose you want $40,000 per year and expect a 4% yield. $$\text{Principal} = \frac{40{,}000}{0.04} = \mathbf{\$1{,}000{,}000}$$ That equals $3,333.33 of monthly income. If your expected yield were 5% instead, you would need \(40{,}000 \div 0.05 = \$800{,}000\).

FAQ

What yield should I use? A conservative 3–4% is common for diversified portfolios; dividend or bond yields may differ. Use a rate you can sustain.

Does this account for inflation or taxes? No. It is a gross, pre-tax estimate. Reduce your effective yield to allow for taxes and inflation.

Is this the 4% rule? Using a 4% yield gives the same answer as the 4% rule — you need 25 times your target annual income.