What This Calculator Does

This tool tells you how large a deposit or lump sum you need to set aside so that the interest alone produces a desired monthly income — without touching the principal. It's useful for planning passive income, retirement drawdown, or savings goals where you want your capital to stay intact.

How to Use It

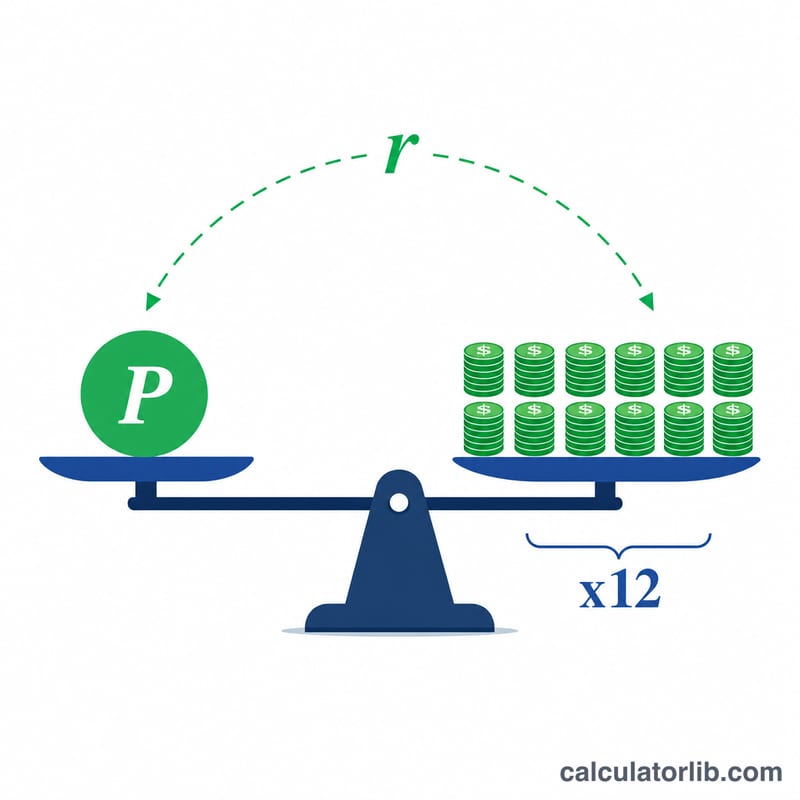

Enter the monthly income you want to receive and the annual interest rate (APR) you expect to earn on the deposit. The calculator multiplies your monthly income by 12 to get the annual income needed, then divides by the decimal interest rate to reveal the principal required.

The Formula Explained

The core equation is

$$\text{Deposit} = \frac{\text{Monthly Income} \times 12}{\dfrac{\text{Annual Rate (\%)}}{100}}$$The numerator is the yearly income you want. The denominator is the rate expressed as a decimal. Dividing the two gives the principal whose yearly interest exactly equals your target income.

Worked Example

Suppose you want $1,000 per month and your bank pays 5% annually. Annual income needed = \(\$1{,}000 \times 12 = \$12{,}000\). Deposit:

$$\text{Deposit} = \frac{\$12{,}000}{0.05} = \$240{,}000$$With $240,000 earning 5%, you receive $12,000 a year, or $1,000 a month, while keeping the principal.

FAQ

Does this account for taxes or inflation? No. It gives a gross, pre-tax figure assuming a constant rate. Real income may be reduced by taxes and eroded by inflation over time.

Why does a lower rate require a bigger deposit? Because less interest is earned per dollar, you need more dollars to reach the same income.

Is the principal touched? No — this assumes you live only on the interest, leaving the deposit intact.