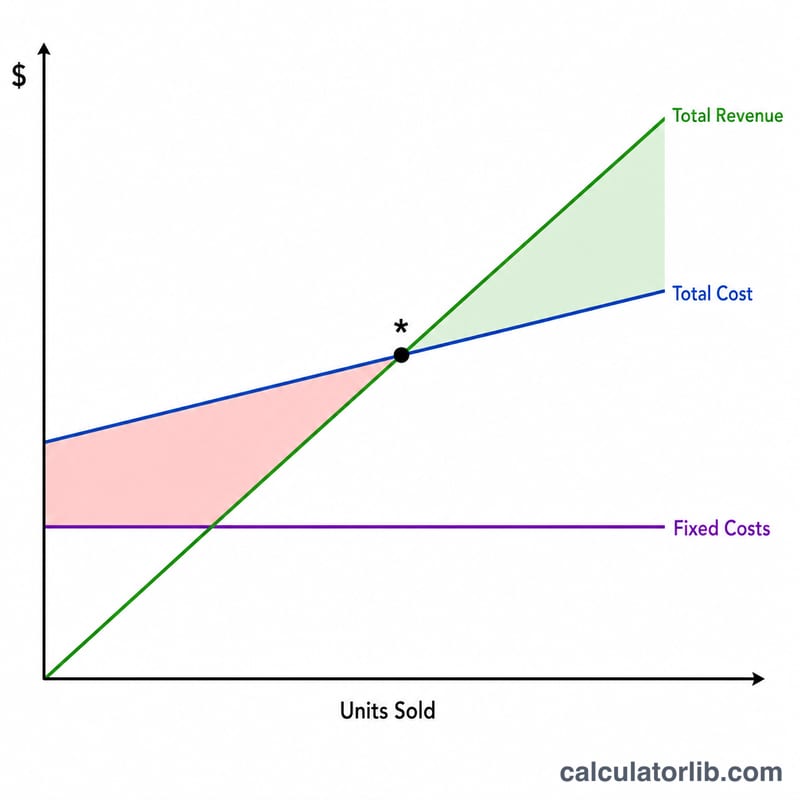

What Is the Break-Even Point?

The break-even point is the level of sales at which total revenue exactly equals total costs — you make neither a profit nor a loss. Knowing this number is essential for pricing decisions, sales targets, and assessing whether a product or business idea is viable. This calculator works in any currency; just keep your inputs consistent.

How to Use This Calculator

Enter three values: your total fixed costs (rent, salaries, insurance — costs that don't change with sales volume), the selling price per unit, and the variable cost per unit (materials, packaging, per-sale fees). The calculator returns the number of units you must sell to break even, the contribution margin per unit, the contribution margin ratio, and the revenue that target represents.

The Formula Explained

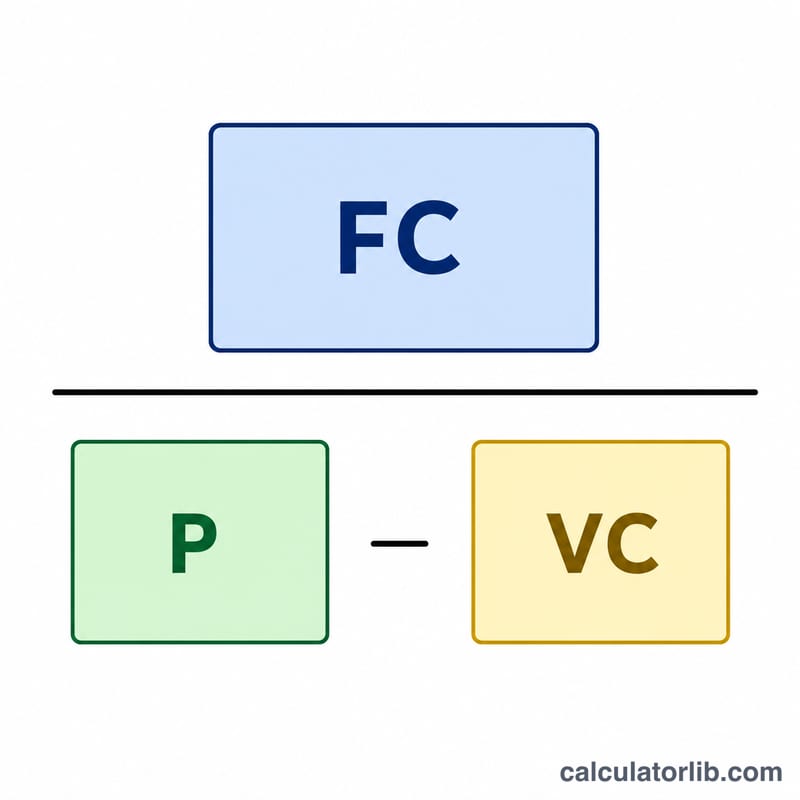

The formula is $$\text{Break-Even Units} = \frac{\text{Fixed Costs}}{\text{Price/Unit} - \text{Variable Cost/Unit}}$$ The denominator, price minus variable cost, is the contribution margin — the amount each sale contributes toward covering fixed costs. Once enough units are sold to cover all fixed costs, every additional unit's contribution margin becomes profit.

Worked Example

Suppose fixed costs are $10,000, each unit sells for $25, and the variable cost per unit is $15. The contribution margin is \(\$25 - \$15 = \$10\). $$\text{Break-Even Units} = \frac{\$10{,}000}{\$10} = 1{,}000 \text{ units}$$ At $25 each, that's $25,000 in break-even revenue. Selling more than 1,000 units produces profit; fewer means a loss.

Key Terms Defined

- Fixed costs — Costs that do not change with the number of units produced or sold within the relevant range, such as rent, salaried staff, insurance, and equipment leases.

- Variable cost per unit — The cost incurred for each additional unit produced or sold, including direct materials, per-unit labor, packaging, and shipping.

- Price per unit — The selling price charged to the customer for one unit of the product or service.

- Contribution margin (per unit) — Price per unit minus variable cost per unit. It is the amount each sale "contributes" toward covering fixed costs and, beyond break-even, toward profit. \(\text{CM} = \text{Price} - \text{Variable Cost}\).

- Contribution margin ratio — Contribution margin expressed as a fraction of price: \(\text{CM ratio} = \frac{\text{Price} - \text{Variable Cost}}{\text{Price}}\). It shows the share of each sales dollar available to cover fixed costs.

- Break-even point — The sales volume at which total revenue equals total costs, so profit is zero. In units: \(\frac{\text{Fixed Costs}}{\text{Contribution Margin per Unit}}\).

- Break-even revenue — The sales dollars needed to break even, equal to break-even units multiplied by price, or \(\frac{\text{Fixed Costs}}{\text{CM ratio}}\).

Interpreting Your Break-Even Result

High vs. low break-even units. A high break-even number means you must sell a large volume before earning any profit, which signals greater risk — especially if your realistic sales forecast is close to or below that figure. A low break-even number gives you a wider safety margin, because you reach profitability sooner and can absorb slow periods more easily.

What the contribution margin ratio signals. A high contribution margin ratio means most of each sales dollar is available to cover fixed costs and then flow to profit, so revenue above break-even grows profit quickly. A low ratio means costs eat up most of each sale, so you depend heavily on volume and have little cushion against price cuts or cost increases.

Selling above or below break-even. Every unit sold above the break-even point adds its full contribution margin to profit. Every unit short of break-even leaves part of your fixed costs uncovered, producing a loss for the period. The gap between your expected sales and break-even is your margin of safety.

Limitations. This model assumes a constant price, a constant variable cost per unit, and fixed costs that stay flat across the range — and it treats the business as selling a single product or a stable product mix. In reality, volume discounts, bulk purchasing, capacity steps (such as hiring or new equipment), and changing product mix can all shift the numbers. Treat the result as a planning benchmark and revisit it whenever your prices or cost structure change.

FAQ

What if price equals variable cost? Then the contribution margin is zero (or negative) and you can never break even — each sale fails to cover its own cost. Raise the price or cut variable costs.

What is the contribution margin ratio? It's the contribution margin divided by the selling price, shown as a percentage. A higher ratio means each sales dollar contributes more to covering fixed costs.

Should units be rounded up? Yes — in practice you can't sell a fraction of a unit, so round up to be safe. This tool shows the exact value so you can decide.