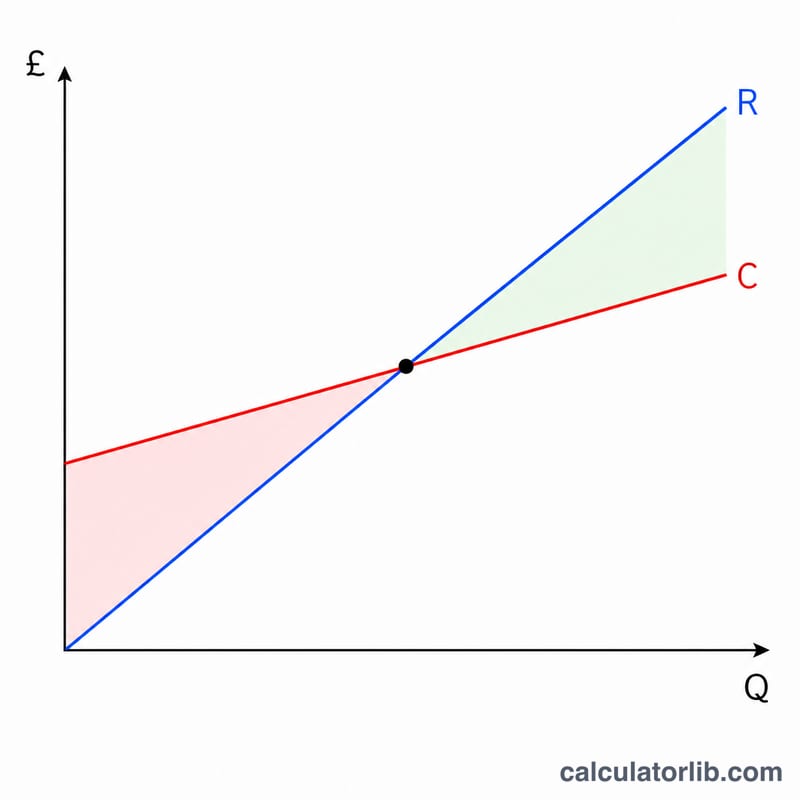

What Is the Break-Even Point?

The break-even point is the level of sales at which total revenue exactly equals total cost, so profit is zero. Below this point a business loses money; above it, each additional unit generates profit. This calculator uses the standard linear cost-volume-profit model where total cost rises in a straight line with units sold.

How to Use This Calculator

Enter your total fixed cost (rent, salaries, insurance and other costs that do not change with volume), the selling price per unit, and the variable cost per unit (materials, packaging, per-unit labour). The tool returns the break-even quantity in units, the matching break-even revenue, the contribution margin per unit, and the contribution margin ratio.

The Formula Explained

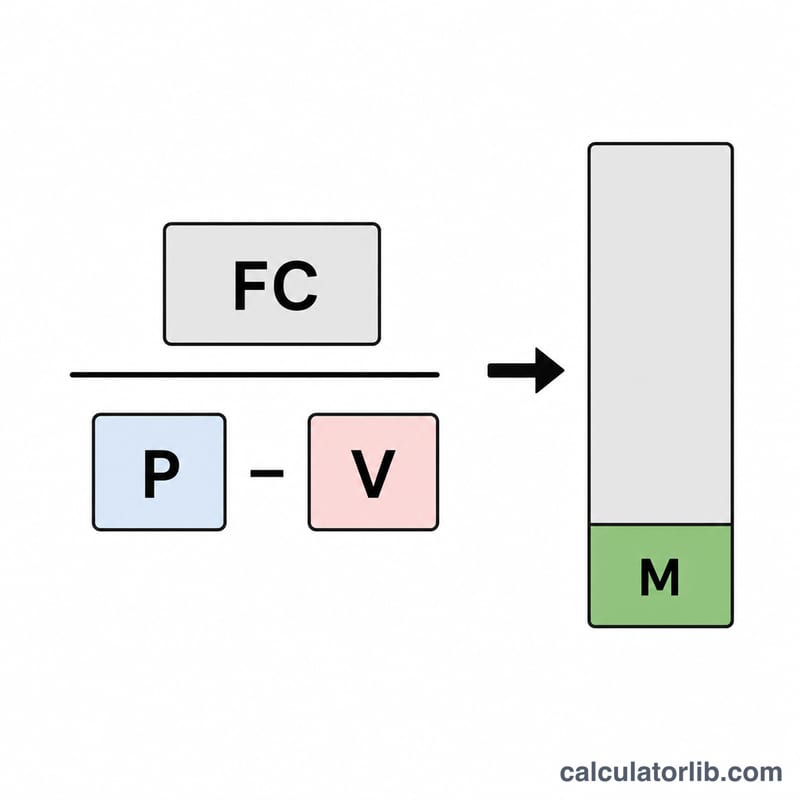

Break-even units equal fixed cost divided by the contribution margin per unit, where the contribution margin is the selling price minus the variable cost:

$$\text{Q} = \frac{\text{Fixed Cost}}{\text{Price} - \text{Variable Cost}}$$

Each unit sold contributes its margin toward covering fixed costs. Once enough units are sold to cover all fixed costs, the company breaks even. If price equals variable cost the margin is zero and there is no break-even point.

Worked Example

Suppose fixed cost is $10,000, the selling price is $25 per unit, and the variable cost is $15 per unit. The contribution margin is \(\$25 - \$15 = \$10\). Break-even units = $$\frac{\$10{,}000}{\$10} = 1{,}000 \text{ units}$$ Break-even revenue = \(1{,}000 \times \$25 = \$25{,}000\). The contribution margin ratio is \(\frac{\$10}{\$25} = 40\%\).

FAQ

What is contribution margin? It is the amount each unit contributes to fixed costs and profit after covering its own variable cost (price minus variable cost).

What if price is below variable cost? The margin is negative and the business loses money on every sale, so there is no positive break-even point.

Does this include taxes? No. This is a pre-tax operating break-even based on a simple linear model. Add desired profit to fixed cost to find a target-profit sales level.