What Is the Break-Even Point?

The break-even point is the level of sales at which your total revenue exactly equals your total costs — meaning you make neither a profit nor a loss. Below this point you lose money; above it, every additional sale contributes to profit. Knowing your break-even point is one of the most important steps in pricing a product, planning a budget, or evaluating whether a new venture is viable.

How to Use This Calculator

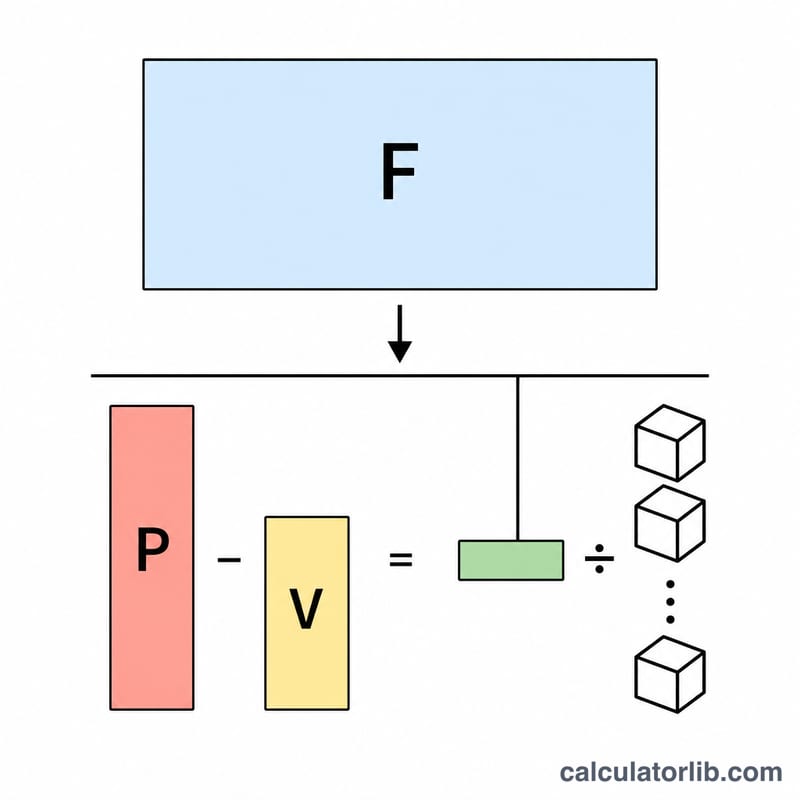

Enter three numbers: your total fixed costs (rent, salaries, insurance and other expenses that do not change with output), the selling price per unit, and the variable cost per unit (materials, packaging, shipping and other costs that rise with each unit sold). The calculator instantly returns the number of units you need to sell, the revenue that represents, your contribution margin per unit, and your contribution margin ratio.

The Formula Explained

First we find the contribution margin — the amount each sale contributes toward covering fixed costs: Contribution Margin = Price − Variable Cost. Then:

Break-Even Units = Fixed Costs ÷ Contribution Margin

Break-Even Revenue = Break-Even Units × Price

If the contribution margin is zero or negative, there is no break-even point because each sale fails to cover its own variable cost.

Worked Example

Suppose your fixed costs are $10,000, you sell each unit for $25, and the variable cost per unit is $15. The contribution margin is $25 − $15 = $10. Break-even units = $10,000 ÷ $10 = 1,000 units. Break-even revenue = 1,000 × $25 = $25,000. The contribution margin ratio is $10 ÷ $25 = 40%.

Interpreting Your Break-Even Result

Your break-even result tells you the minimum activity level your business must reach before it starts generating profit. Reading it correctly means comparing it against what you actually sell.

- Break-even units is the number of units you must sell so that total contribution margin equals fixed costs. Selling exactly this many produces zero profit; every unit beyond it adds its full contribution margin to profit.

- Break-even revenue is the sales-dollar equivalent of that volume. It is useful when you sell a mix of products and think in revenue rather than unit terms.

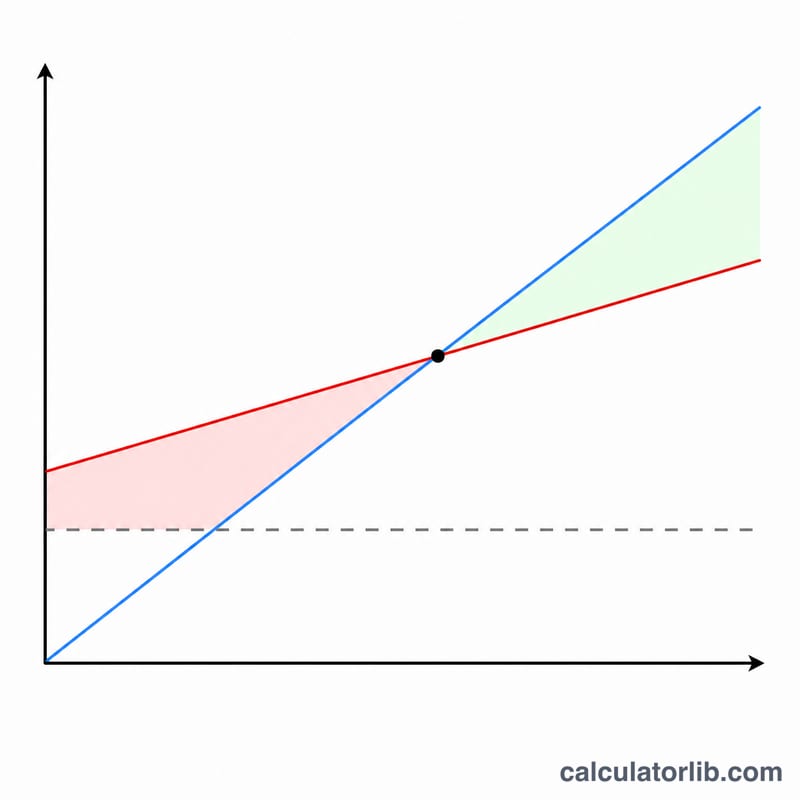

Margin of safety

The margin of safety measures how far current (or projected) sales sit above the break-even point:

$$\text{Margin of Safety}=\text{Actual Sales}-\text{Break-Even Sales}$$For example, if a business breaks even at $214,286 and currently sells $260,000, its margin of safety is $45,714 — about 18% of sales. A larger margin of safety means revenue can fall further before the business begins losing money; a thin margin signals greater vulnerability to downturns.

High vs. low break-even

A high break-even point usually reflects large fixed costs and/or a small contribution margin per unit. Such businesses carry high operating leverage: once they clear break-even, additional sales drop quickly to the bottom line, but losses also mount rapidly if volume falls short. The high-fixed-cost manufacturer above is a typical example.

A low break-even point reflects low fixed costs or a high contribution margin, as with the consulting service. These businesses reach profitability sooner and are more resilient when sales dip, though each additional unit may add less incremental profit relative to total revenue.

You can lower your break-even point three ways: reduce fixed costs, raise the selling price, or cut the variable cost per unit — each of which widens the contribution margin or shrinks the fixed-cost base you need to cover.

This is general educational information about cost-volume-profit analysis, not personalized financial or business advice.

FAQ

What are fixed vs. variable costs? Fixed costs stay the same regardless of how much you produce (rent, salaries). Variable costs change with each unit you make (raw materials, shipping).

Why does my calculator show no result? If the selling price is less than or equal to the variable cost, the contribution margin is zero or negative, so the business can never break even at that price.

How can I lower my break-even point? Reduce fixed costs, lower variable costs per unit, or raise your selling price — each increases the contribution margin and shrinks the number of units needed.