What Is the Break-Even Point?

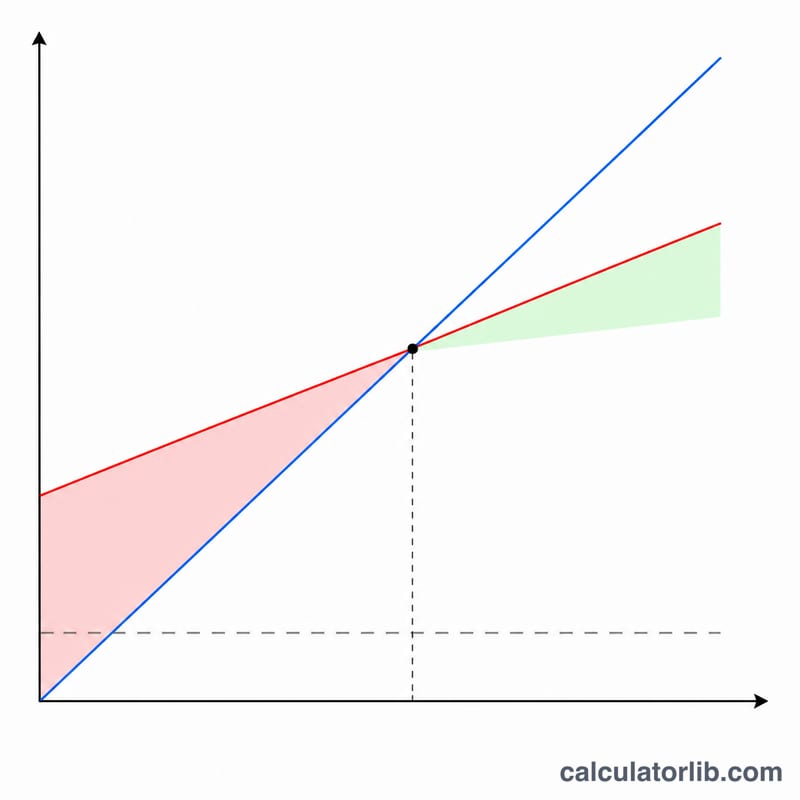

The break-even point is the sales volume at which your total revenue exactly equals your total costs — you make neither a profit nor a loss. Below this point you operate at a loss; above it, every additional unit generates profit. It is one of the most important numbers in pricing, budgeting, and startup planning.

How to Use This Calculator

Enter three values: your fixed costs (rent, salaries, insurance — costs that do not change with volume), the price you charge per unit, and the variable cost per unit (materials, packaging, per-unit labor). The calculator returns how many units you must sell to break even, the contribution margin per unit, and the revenue at that point.

The Formula Explained

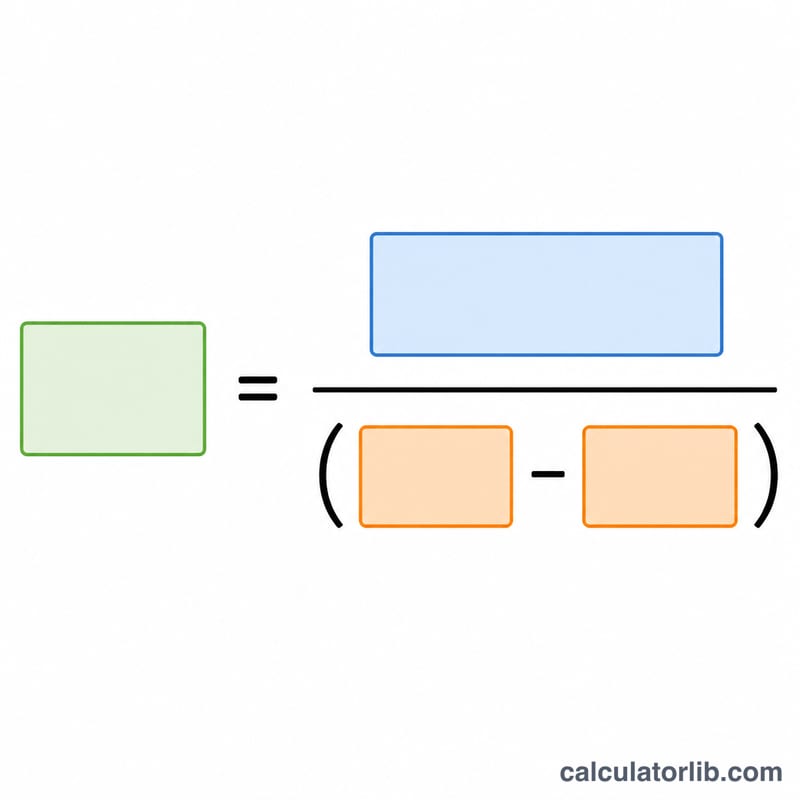

Break-even is solved algebraically by setting cost equal to revenue. Total cost is Fixed + (Variable × Q); total revenue is Price × Q. Setting them equal and solving for Q gives:

$$\text{Break-Even Units} = \frac{\text{Fixed Costs}}{\text{Price per Unit} - \text{Variable Cost per Unit}}$$

The denominator, \(\text{Price} - \text{Variable Cost}\), is the contribution margin — the amount each sale contributes toward covering fixed costs.

Worked Example

Suppose fixed costs are $10,000, you sell each unit for $50, and the variable cost is $30. Contribution margin = \(50 - 30 = \$20\). Break-even units = $$\frac{10{,}000}{20} = \textbf{500 units}.$$ At 500 units, revenue = \(500 \times \$50 = \$25{,}000\), which exactly covers the $10,000 fixed plus $15,000 variable costs.

Key Terms Defined

- Fixed Costs

- Expenses that do not change with the number of units produced or sold over the relevant period — for example rent, salaries, insurance, and equipment leases. They must be paid regardless of sales volume.

- Variable Cost per Unit

- The cost that is incurred for each additional unit produced or sold, such as raw materials, direct labor per unit, packaging, and per-transaction fees. Total variable cost rises in proportion to volume.

- Contribution Margin (per unit)

- The amount each unit contributes toward covering fixed costs after variable costs are paid: \(\text{Price} - \text{Variable Cost}\). Once fixed costs are fully covered, each additional unit's contribution margin becomes profit.

- Contribution Margin Ratio

- The contribution margin expressed as a fraction of price: \(\frac{\text{Price} - \text{Variable Cost}}{\text{Price}}\). It tells you what portion of each sales dollar is available to cover fixed costs and profit.

- Break-Even Units

- The number of units that must be sold so that total revenue exactly equals total cost — the point of zero profit and zero loss. It equals fixed costs divided by contribution margin per unit.

- Break-Even Revenue

- The sales dollars at the break-even point, equal to break-even units multiplied by price, or fixed costs divided by the contribution margin ratio.

- Margin of Safety

- How far actual or projected sales exceed the break-even point, often expressed as a percentage: \(\frac{\text{Actual Sales} - \text{Break-Even Sales}}{\text{Actual Sales}}\). It measures the cushion before the business begins to lose money.

Interpreting Your Break-Even Result

The break-even units figure is the sales volume at which your business neither earns a profit nor incurs a loss — total revenue exactly equals total cost. The break-even revenue is the corresponding sales-dollar threshold. Together they answer the practical question: how much do I need to sell just to keep the lights on?

Operating above vs. below break-even

When sales exceed the break-even point, every additional unit adds its full contribution margin to profit, because fixed costs are already covered. When sales fall below break-even, the business operates at a loss: revenue is not enough to cover both variable and fixed costs. The break-even point therefore acts as a target floor for sales planning, pricing decisions, and cost control.

Margin of safety

The gap between expected sales and the break-even point is your margin of safety. For example, if you expect to sell 1,000 units and break even at 750, your margin of safety is 250 units, or 25% of expected sales. A larger margin of safety means more room to absorb a downturn in demand, a price cut, or rising costs before profitability is threatened.

Assumptions and limits

This calculation is a simplified linear model and carries several important assumptions:

- Pre-tax: Break-even is computed before income taxes; it reflects operating profit, not after-tax profit.

- Single product (or fixed mix): The formula assumes one product or a constant sales mix. With multiple products at different margins, you must use a weighted-average contribution margin.

- Linear costs and price: It assumes price per unit, variable cost per unit, and total fixed costs stay constant across the relevant range. In reality, volume discounts, capacity step-costs, and price changes can shift the break-even point.

- Costs cleanly split: Some costs are semi-variable and must be separated into fixed and variable components before use.

Use break-even analysis as a planning and decision-support tool alongside cash-flow and margin analysis rather than as a precise forecast. This is general educational information, not professional financial advice; consult a qualified advisor for decisions specific to your business.

FAQ

What if price is less than variable cost? Then the contribution margin is negative or zero and you can never break even — each sale loses money. Raise your price or cut variable costs.

Should I round up the units? Yes. Since you cannot sell a fraction of a unit, round up to the next whole unit to be safely at or above break-even.

Does this include taxes? No. This is a pre-tax operating break-even. For after-tax targets, increase the required profit before dividing by contribution margin.