What Is the FD Premature Withdrawal Penalty Calculator?

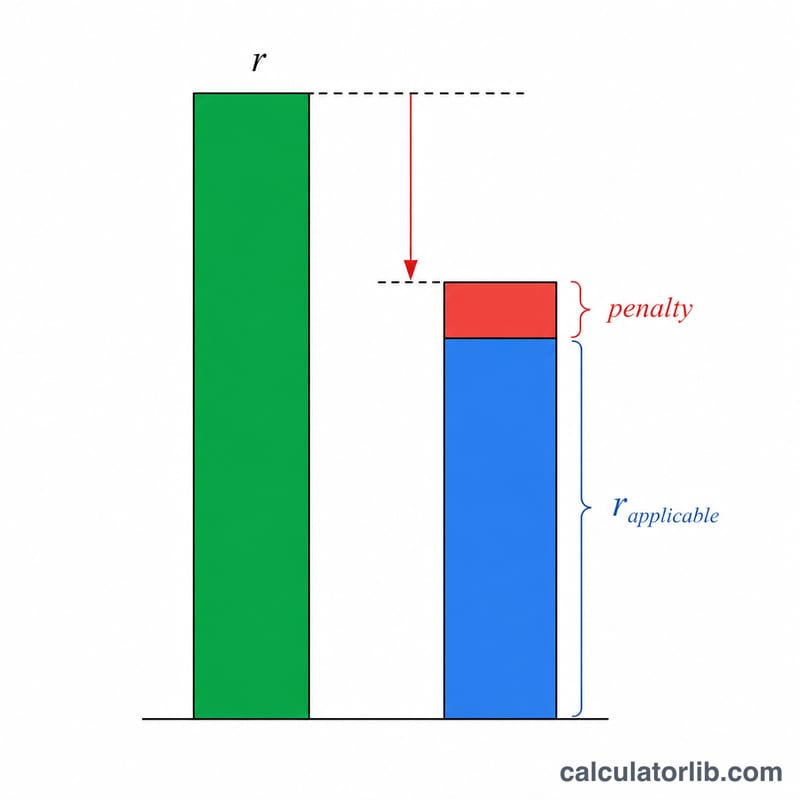

When you break a fixed deposit (FD) before its maturity date, banks usually pay interest at a reduced "applicable" rate — the rate that was in effect for the actual period your money stayed deposited — and then subtract a premature withdrawal penalty (commonly 0.5%–1% per annum). This calculator shows exactly how much interest you will receive, the final withdrawal value, and how much interest you lose because of the penalty.

How to Use It

Enter your deposit amount (principal), the original card rate quoted when you opened the FD, the applicable rate for the period actually held, the penalty rate, and the number of months you held the deposit before withdrawing. The tool computes interest using the reduced effective rate.

The Formula Explained

The effective rate is the applicable rate minus the penalty. Interest is calculated as simple interest prorated over the months held:

$$I = P \times \frac{r_{e}}{100} \times \frac{n}{12} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} P &= \text{Principal} \\ r_{e} &= \max\!\left(\text{Applicable Rate} - \text{Penalty},\ 0\right) \\ n &= \text{Months Held} \end{aligned} \right.$$

The maturity (withdrawal) value adds this interest back to your principal.

Worked Example

Suppose you deposit 100,000 at a card rate of 7%, but for the 12 months you actually held it, the applicable rate is 6% with a 1% penalty. The effective rate is \(6\% - 1\% = 5\%\). $$I = 100{,}000 \times \frac{5}{100} \times \frac{12}{12} = \mathbf{5{,}000}$$ Without the penalty you would have earned 6,000, so you lose 1,000 to the penalty, and your withdrawal value is 105,000.

FAQ

Why is the rate lower than my booked rate? Banks pay the rate applicable to the period the deposit actually ran, not the original tenure rate, which is often lower for shorter periods.

Is interest simple or compound here? This calculator uses simple-interest proration for the held period, which closely matches how banks compute penalty payouts for short tenures.

Can the penalty be waived? Some banks waive penalties for senior citizens, sweep-in accounts, or in genuine emergencies — set the penalty to 0 to model that.