What this calculator does

Applies to the United States. This tool estimates how much of an early 401(k) withdrawal you actually keep after the IRS and your state take their share. If you take money out of a traditional 401(k) before age 59½, the distribution is generally added to your ordinary taxable income and hit with an additional 10% federal early-withdrawal penalty. Assumptions: traditional (pre-tax) 401(k), 2024-era rules, and a flat marginal-rate approximation rather than full bracket math.

How to use it

Enter your gross withdrawal amount, your estimated federal marginal tax rate (the bracket the withdrawal falls into), and your state income tax rate. Leave the penalty box checked if you are under 59½; uncheck it if you qualify for an exception (such as separation from service at age 55+, disability, or certain hardship rules). The calculator returns the net cash, a breakdown of each cost, and the overall effective cost rate.

The formula explained

The net amount is simply the withdrawal reduced by three layers: federal income tax (withdrawal × federal rate), state income tax (withdrawal × state rate), and the 10% penalty (withdrawal × 0.10). Adding those three together gives the total cost, and the effective rate expresses that total as a percentage of the gross withdrawal.

$$\text{Net} = W - (W \cdot r_{fed}) - (W \cdot r_{state}) - (W \cdot 0.10)$$$$\text{Net} = W \times (1 - r_{fed} - 0.10 - r_{state})$$$$r_{eff} = \frac{\text{Total Cost}}{W} \times 100$$

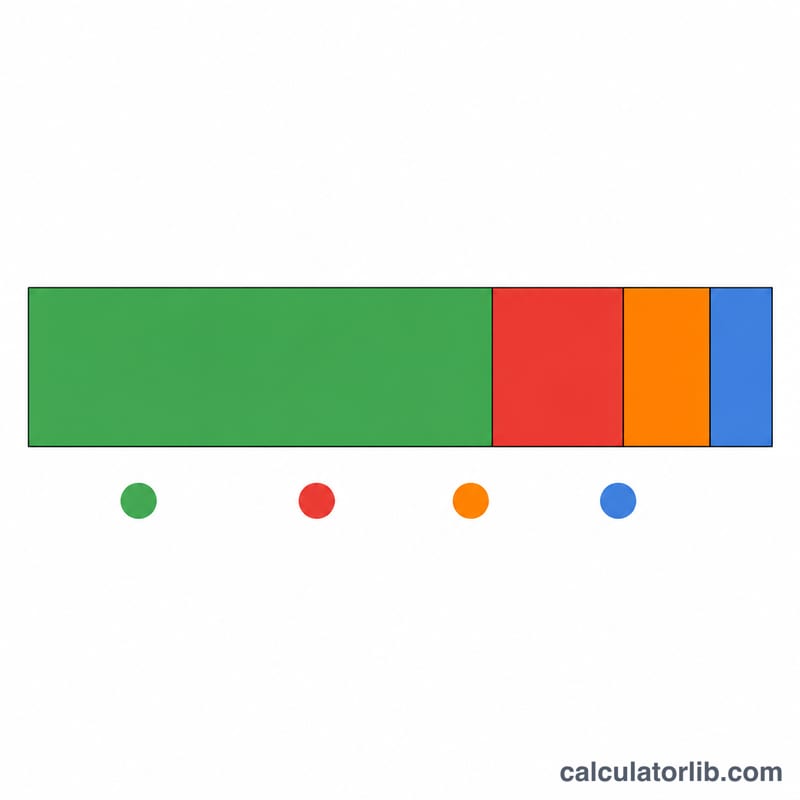

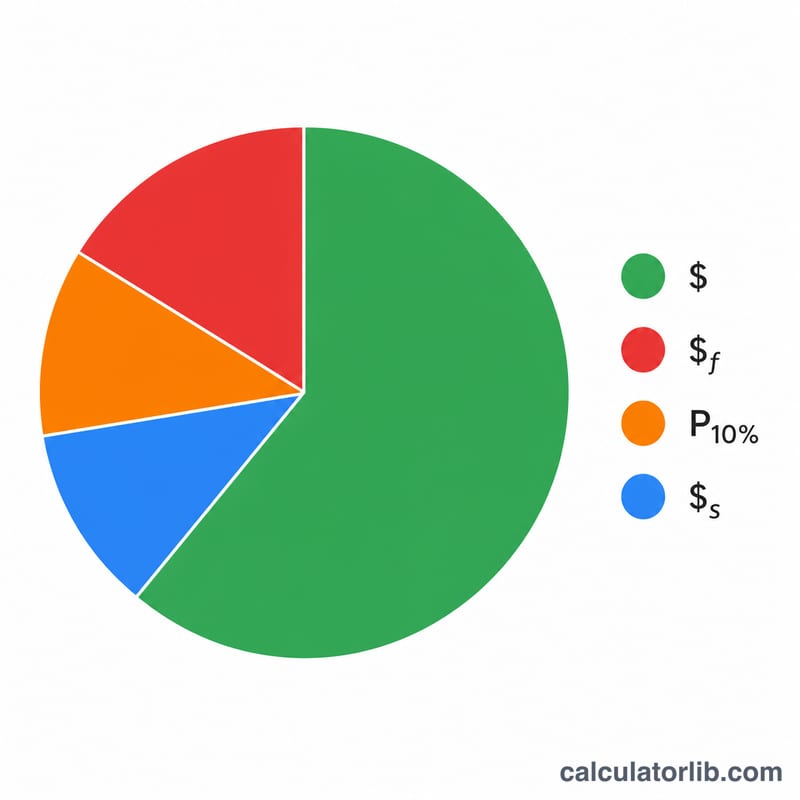

Worked example

Suppose you withdraw $20,000, your federal marginal rate is 22%, your state rate is 5%, and you are under 59½. Federal tax = $4,400, state tax = $1,000, penalty = $2,000. Total cost = $7,400, so you keep $12,600 — an effective cost of 37%.

$$\text{Net} = \$20{,}000 \times (1 - 0.22 - 0.10 - 0.05) = \$12{,}600$$

2024 Federal Income Tax Brackets

A 401(k) early withdrawal is added to your other ordinary income and taxed at your marginal rate — the rate on the last dollars of income. The withdrawal can span more than one bracket, so the table below shows where 2024 thresholds fall for two common filing statuses. These are taxable-income thresholds (after deductions), not gross income.

| Marginal rate | Single (taxable income) | Married filing jointly |

|---|---|---|

| 10% | $0 – $11,600 | $0 – $23,200 |

| 12% | $11,600 – $47,150 | $23,200 – $94,300 |

| 22% | $47,150 – $100,525 | $94,300 – $201,050 |

| 24% | $100,525 – $191,950 | $201,050 – $383,900 |

| 32% | $191,950 – $243,725 | $383,900 – $487,450 |

| 35% | $243,725 – $609,350 | $487,450 – $731,200 |

| 37% | $609,350 and up | $731,200 and up |

To find the marginal rate to enter, add the withdrawal to your existing taxable income and see which bracket the top of that total lands in. Most or all of a large withdrawal may be taxed at a higher rate than your normal wages.

401(k) Early-Withdrawal Penalty Exceptions

Distributions before age 59½ are normally subject to a 10% additional tax on top of ordinary income tax. The IRS allows several exceptions that waive the penalty (income tax may still apply). The table summarizes common exceptions; conditions and documentation requirements apply.

| Exception | Age / condition |

|---|---|

| Rule of 55 (separation from service) | Leave the employer in or after the year you turn 55 (50 for qualified public-safety employees) |

| Total and permanent disability | Any age, if disabled per IRS definition |

| Unreimbursed medical expenses | Amount exceeding 7.5% of AGI, any age |

| Qualified Domestic Relations Order (QDRO) | Paid to ex-spouse/dependent under a court order, any age |

| IRS levy on the plan | Funds taken to satisfy an IRS levy, any age |

| Death of the participant | Paid to a beneficiary or estate, any age |

| Substantially equal periodic payments (72(t)/SEPP) | A series of equal payments; must continue for 5 years or until age 59½, whichever is longer |

| Qualified birth or adoption | Up to $5,000 per child within one year of the event |

| Emergency personal expense (SECURE 2.0) | One distribution up to $1,000 per year |

If an exception applies, uncheck the 10% penalty in the calculator. Note these specific exception rules apply to workplace plans like 401(k)s; IRA exceptions differ slightly (for example, the Rule of 55 does not apply to IRAs).

Interpreting Your Result

The effective cost rate is the total fraction of your gross withdrawal consumed by federal income tax, state income tax, and the 10% early-withdrawal penalty. If the calculator shows a 37% cost rate, it means 37 cents of every dollar withdrawn does not reach you; the remaining 63 cents is your net cash.

Net cash is often far below the gross amount for three stacked reasons: ordinary income tax at your marginal rate, an additional state tax in most states, and the flat 10% federal penalty that applies (unless an exception fits) only because the money came out before age 59½. None of these touch the principal you keep invested — they apply only to the dollars you remove.

It is important to distinguish withholding from final tax owed. Plan administrators are generally required to withhold 20% for federal tax on an eligible distribution, but that 20% is just a prepayment — not your actual liability. If your true marginal rate is higher than 20%, you will owe more when you file; if it is lower, you may get part of it back. The 10% penalty is typically not withheld at all and is settled on your tax return, so the cash you receive at distribution can overstate what you ultimately keep.

Finally, a large withdrawal can push part of your income into a higher bracket than your normal wages occupy. Because the marginal rate applies to the top dollars, the true cost of the last portion of a big withdrawal may exceed the rate you entered. To estimate the bracket the top of your income reaches, you can add the withdrawal to your other income and check it against a marginal tax rate calculator, then enter that rate here.

This is general educational information, not tax or financial advice. Rules, thresholds, and exceptions change and depend on your full situation — consult a qualified tax professional before taking a distribution.

FAQ

Is the 10% penalty always charged? No. Exceptions include disability, qualified medical expenses above a threshold, a qualified domestic relations order, and the "rule of 55." Uncheck the penalty box in those cases.

Why use a flat marginal rate? A withdrawal can push you into higher brackets, so this is an estimate. For precise figures, model the full bracket impact or consult a tax professional.

Does this cover Roth 401(k)s? No — Roth distributions follow different rules; this tool models traditional pre-tax 401(k) withdrawals.