What Is a Mortgage Penalty Calculator?

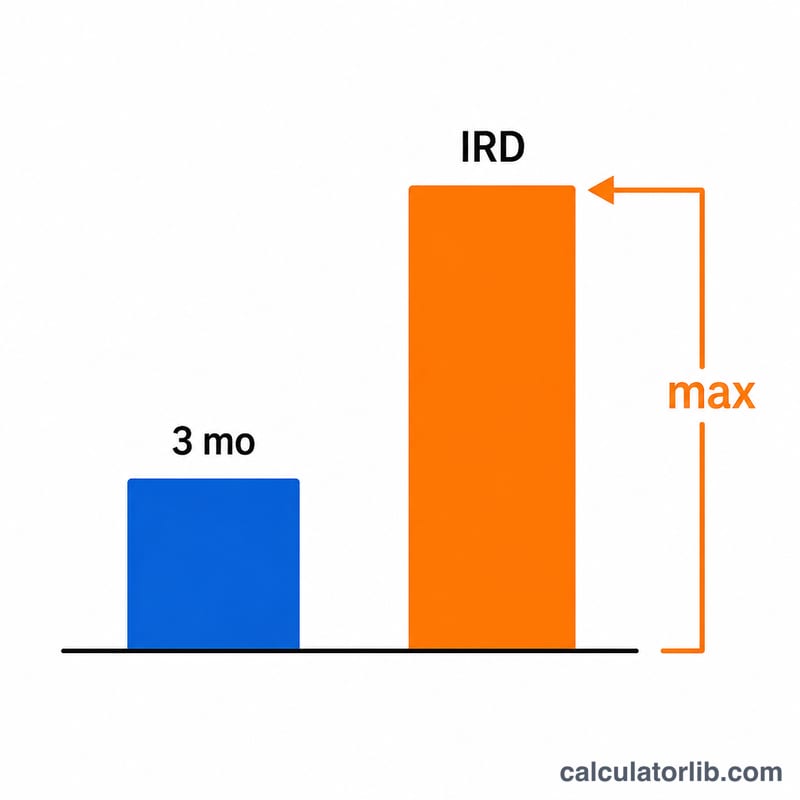

A mortgage prepayment penalty is the fee a lender charges when you pay off, refinance, or break a fixed-rate mortgage before the end of its term. Most lenders calculate this penalty as the greater of two amounts: three months' interest, or the Interest Rate Differential (IRD). This calculator estimates both and shows which one applies. The IRD method described here is common for fixed-rate mortgages in markets such as Canada; always confirm the exact formula your lender uses, as posted-rate and discount adjustments vary.

How to Use It

Enter your outstanding mortgage balance, your current contract interest rate, a comparison (or posted) rate the lender uses for the remaining term, and the number of months left on your term. The calculator computes both penalty methods and reports the larger figure — the amount most lenders would charge.

The Formula Explained

Three months' interest is simply your balance times your monthly rate times three: \(B \cdot \frac{r}{12} \cdot 3\). The IRD is your balance multiplied by the difference between your rate and the comparison rate, scaled by the months remaining: \(B \cdot (r - r_c) \cdot \frac{m}{12}\). The penalty equals the maximum of the two:

$$\text{Penalty} = \max\left(B \cdot \tfrac{r}{12} \cdot 3,\; B \cdot (r - r_c) \cdot \tfrac{m}{12}\right)$$

If the comparison rate exceeds your current rate, the IRD is treated as zero.

Worked Example

Suppose your balance is $300,000, your rate is 5%, the comparison rate is 3%, and 24 months remain. Three months' interest:

$$300{,}000 \times \frac{0.05}{12} \times 3 = \$3{,}750$$

IRD:

$$300{,}000 \times (0.05 - 0.03) \times \frac{24}{12} = 300{,}000 \times 0.02 \times 2 = \$12{,}000$$

The penalty is the greater of the two: $12,000, charged via the IRD method.

FAQ

Why is the IRD often higher? When market rates have fallen below your contract rate, the lender loses future interest, so the IRD grows with both the rate gap and the time left.

Is three months' interest ever the bigger penalty? Yes — typically when your rate is close to or below the comparison rate, or when little time remains on the term.

Is this exact? No. It's an estimate. Lenders may use posted rates, cash-back clawbacks, or other adjustments. Always request an official payout statement before deciding.