What is the Add-on Rate vs APR Conversion Table?

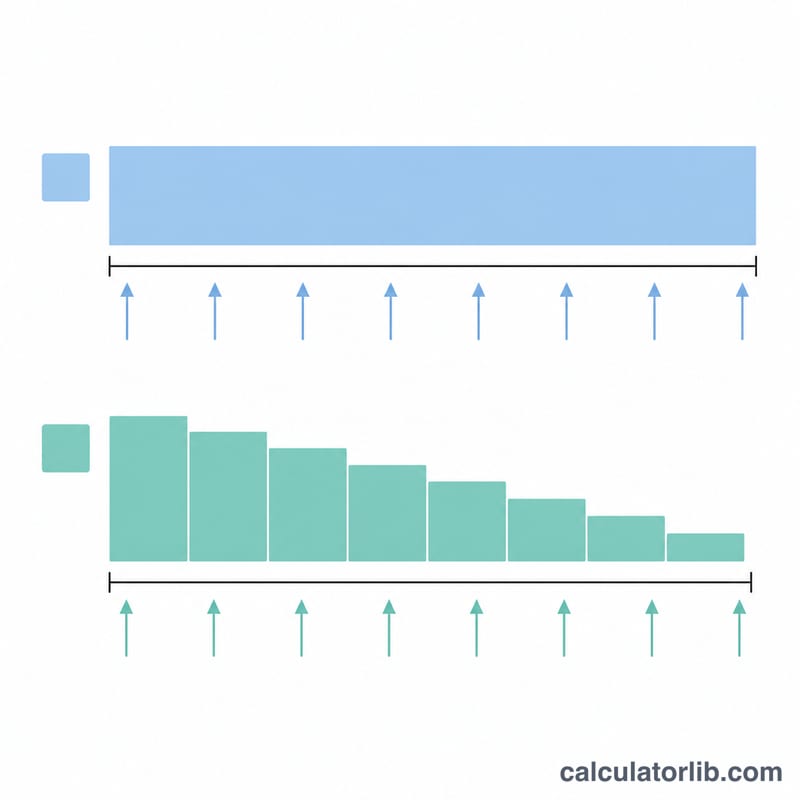

This calculator converts between an add-on rate (a flat interest rate charged on the original principal for the whole loan term) and the effective annual rate (APR) of an equal-payment amortizing loan. The add-on method is a common consumer-loan convention for auto loans, motorcycle loans and installment sales. Because the borrower repays principal gradually but is charged interest on the full original principal the entire time, the true APR is roughly double the add-on rate. This is universal financial math and applies in any country.

How to use it

Enter a Rate in percent, pick which direction to convert (APR to add-on, or add-on to APR), choose the payment frequency (payments per year), then set the maximum number of payments and the step. The tool prints one row per loan term so you can compare how the conversion changes with length.

The formula

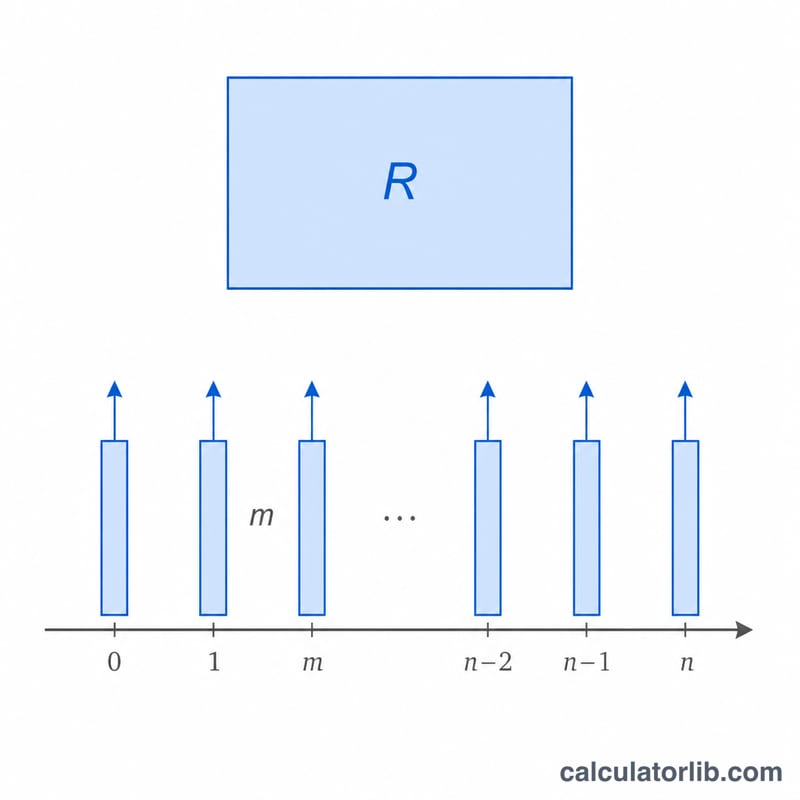

Let \(m\) be payments per year, \(n\) the number of payments, and \(i = R/m\) the per-period rate where \(R\) is the effective annual rate (decimal). The total repayment factor (total paid divided by principal) is \(n \cdot i / (1 - (1+i)^{-n})\). The add-on (total flat interest ratio) is $$A = \frac{n \cdot i}{1 - (1+i)^{-n}} - 1$$ To go from add-on back to APR we solve the same equation numerically for \(R\).

Worked example

Take \(R = 5\%\) effective annual, monthly payments (\(m = 12\)), \(n = 60\). Per-period \(i = 0.05/12 = 0.00416667\). \((1+i)^{-60} = 0.779205\), so \(1 - 0.779205 = 0.220795\). Factor = $$\frac{60 \times 0.00416667}{0.220795} = \frac{0.25}{0.220795} = 1.13227$$ Add-on \(A = 0.13227 = 13.23\%\). Reversing \(13.227\%\) add-on at \(n = 60\) returns \(R \approx 5\%\) APR.

FAQ

Why is the APR about double the add-on rate? The add-on charges interest on the full original principal even though the balance falls over time, so the effective annualized cost is higher.

Is the add-on column annual or total? It is the total flat interest ratio over the whole term. Divide by the number of years (\(n/m\)) for an annualized add-on figure.

What does the step do? It sets the spacing between table rows, e.g. a step of 6 with a max of 60 shows \(n = 6, 12, 18, \ldots 60\).